21st Nov 2025. 10.35am

Weekly Briefing – Friday 21st November

| Market | Movement this week (%)* |

|---|---|

| FTSE 100 | -2.35% |

| FTSE 250 | -2.73% |

| FTSE All-Share | -2.36% |

| AIM 100 | -1.90% |

| AIM All-Share | -1.83% |

* Price movement from Monday's open at 8am

Regency View:

Weekly Briefing – Friday 21st November

Market Overview

Dear Investor,

This week saw the main event of the autumn earnings season, Nvidia’s numbers, and they certainly lived up to the anticipation. The chipmaker reported a 62% year-on-year jump in revenue to 57 billion dollars and pushed back confidently against any suggestion that AI demand is cooling. For a market that has spent the past month debating whether the AI boom is losing momentum, the scale of Nvidia’s performance went a long way toward resetting the conversation.

What surprised investors was not the strength of the results but the way the share price behaved afterwards. Nvidia opened sharply higher before fading through the session and closing around 3% lower on the day. It was a reminder that expectations have climbed to extraordinary heights and that even exceptional execution can struggle to satisfy a market positioned for perfection. The reaction said little about fundamentals and much more about how crowded the trade has become.

The detail inside the update reinforced the sense of deep and sustained demand. Photonics and data-centre products once again led the way, fuelled by hyperscale cloud providers racing to build out AI infrastructure. Nvidia made it clear that this investment cycle is not easing. If anything, appetite for compute capacity continues to grow, pushing bubble fears to the sidelines and bringing focus back to the real drivers behind the theme.

There were macro threads in the backdrop, including stronger US jobs data and a still-divided Federal Reserve, but none of them changed the core takeaway. Nvidia’s update underscored that AI remains the dominant structural force shaping global market psychology, even if day-to-day price action is becoming more volatile.

For UK investors, the message is straightforward. Short-term swings are inevitable, but the long-term AI story remains firmly intact. Nvidia’s numbers showed that momentum in the build-out of AI infrastructure is alive and well, and that remains the more important signal amid the noise.

Wishing you a fantastic weekend,

Tom

Thomas Light – Chartered FCSI

Director of Research

Market Movers

On the rise: Halma (LSE:HLMA) +6.2% on the week

Halma was one of the standout risers this week after the group lifted its full-year revenue guidance on the back of a strong first half. Adjusted pretax profit jumped 29.3% to 270.5 million pounds, driven by exceptional demand for its photonics products in the United States. These are the high precision components at the heart of data centre construction, and with AI infrastructure expanding at pace, the company’s exposure to this theme is turning into a powerful tailwind.

Management now expects organic revenue growth in the mid-teens percentage range for the full year, up from an earlier forecast of low double digits. A major cloud service provider accounted for almost a fifth of group revenue in the period, highlighting just how central Halma’s technology has become to the new wave of data centre investment. The group also guided to an adjusted EBIT margin of around 22% for the full year and proposed a 7% increase in the interim dividend to 9.63 pence.

The market responded warmly to the update. Halma’s ability to capture premium growth in high demand niches, while maintaining its disciplined margin profile, has reinforced confidence in its long-term strategy. With AI infrastructure still in full build-out mode, the company enters the second half in a position of real strength.

REGENCY VIEW: Halma has been a long-running favourite of ours, with first and second tranche recommendations to FTSE Investor clients in 2023 and 2024 respectively. The position has grown into a very healthy profit, and this latest upgrade only reinforces why we backed the business in the first place.

Crest Nicholson was one of the weakest performers this week after the housebuilder warned that full-year profit would land at the low end of, or slightly below, its guidance range. The update confirms what many in the sector have been feeling through the summer. The housing market has stayed soft, buyers remain cautious, and the uncertainty around government tax policy has done little to improve sentiment. Against that backdrop, FY25 volumes came in at the lower end of expectations and the open market sales rate eased through the final quarter.

Management did its best to focus attention on the positives. The group has made progress on its transformation plan, Project Elevate, with early improvements in build quality, customer satisfaction and sales strategy. The balance sheet is in better shape too, helped by tighter inventory management and a series of land parcel disposals that delivered good economic terms. Net debt finished the year at the stronger end of guidance and around 50 million pounds of land receipts have already been secured for FY26. These are encouraging steps for a business that has been working hard to regain financial flexibility.

Even so, the market took a cautious view. A reserves adjustment linked to historical profit recognition and signs of build cost inflation added to the sense that the turnaround will take time. Crest Nicholson has a clearer strategy, a more disciplined operating approach and a better aligned land bank, but the near-term environment is still challenging. Investors want to see that the transformation can translate into steadier sales rates and firmer margins, and for now, that remains the missing piece.

REGENCY VIEW: Crest Nicholson is clearly doing the heavy lifting behind the scenes, and the early signs of a more disciplined, sharper business are beginning to show. The challenge now is turning that operational graft into the kind of consistency that convinces investors the turnaround has real staying power.

Sector Snapshot

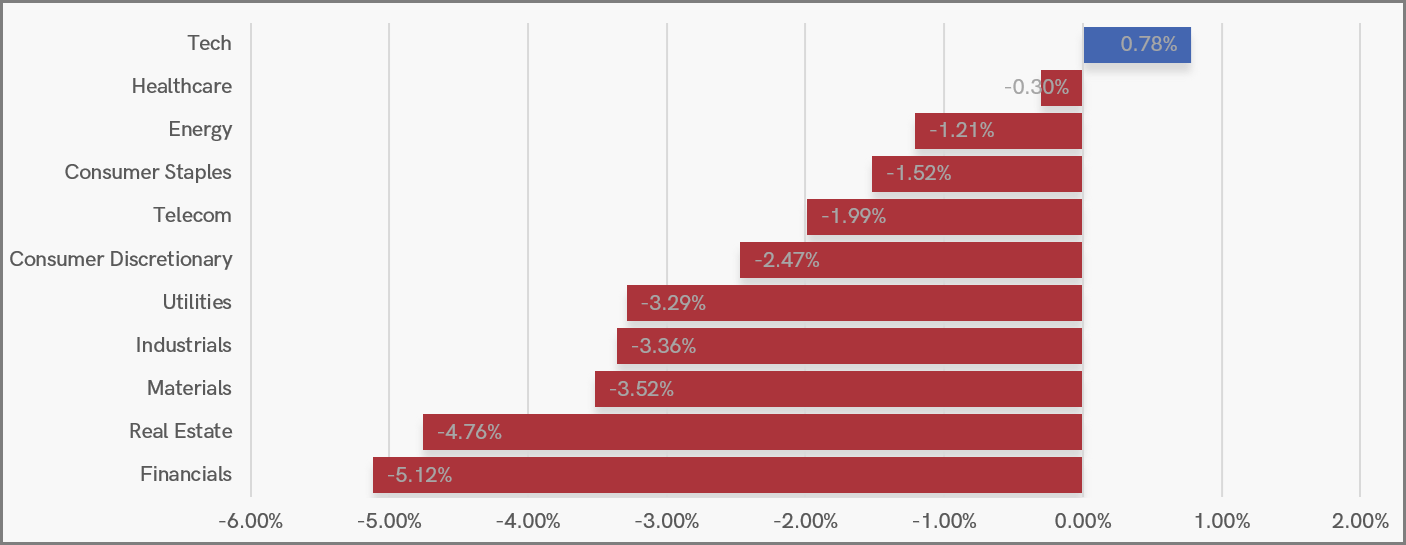

It was a tough week across most sectors, with Tech standing out as the only area to post gains, helped by renewed interest in quality growth and resilient earnings. Healthcare also held relatively firm, while the rest of the market saw broad-based declines.

Financials and Real Estate were hit hardest, reflecting investor caution around interest rates and credit conditions. Materials, Industrials and Utilities also saw sharp losses, underscoring a clear risk-off tone as defensives and cyclicals alike came under pressure.

UK Sector Performance (7-Days)

UK Price Action

It has been a continuation of the weakness seen at the end of last week. Prices have slipped back below the 50-day moving average, with the FTSE now retracing roughly five percent from its recent highs.

Short-term momentum remains firmly bearish, but the longer-term trend structure is still clearly bullish. For now, the focus is on whether buyers will step in around the 9,350 support zone to defend the broader uptrend.

FTSE 100 Rolling Futures (Daily Candle Chart)

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.