9th Apr 2026. 9.01am

Regency View:

BUY MHA (MHA) Second Tranche

Regency View:

BUY MHA (MHA) Second Tranche

A valuation reset creates a second opportunity

We first highlighted MHA back in September following a highly successful IPO, with the shares continuing to make impressive gains in the months that followed. More recently, that momentum has faded, with the stock pulling back sharply from its highs.

However, trends rarely move in a straight line. What we are seeing now looks more like a valuation reset than a change in the underlying story, and in our view, that is starting to create a more attractive entry point.

Continued execution with little fanfare

The underlying business has continued to perform as expected. The most recent update showed revenue up 13.2% to £121.3m, with adjusted EBITDA rising 10.7% to £21.8m. Margins remained stable at 18%, while net cash increased to £25.7m, supporting guidance for full year results in line with expectations.

There were no standout surprises in those numbers, but that is part of the appeal. MHA is delivering steady, predictable growth across its core service lines, supported by a high level of recurring income and strong client retention.

What stands out is the quality of those earnings. With around 87% of revenue recurring, the group benefits from a high level of visibility across its client base. This is not growth that needs to be constantly rebuilt, but revenue that builds through long term relationships and repeat work.

The model continues to translate efficiently into returns. Return on capital remains around 85%, supported by a structure that does not require significant reinvestment to sustain growth. Cash conversion is also strong, reflecting tight control over working capital and a business that turns earnings into cash efficiently.

There is also an element of operating leverage starting to come through. As the business scales, incremental revenue does not require the same level of cost growth, allowing margins to remain stable while earnings expand.

Expanding the platform

The more relevant development is what has happened since those results.

The completion of the UAE acquisition this week adds another step in the group’s international expansion. For around £7.4m, MHA has acquired an established audit, tax and advisory business in a region that continues to attract global capital and cross border activity.

This follows the South East Europe deal completed last year and reinforces a clear strategy. MHA is building an increasingly international platform in a fragmented market where scale, sector expertise and reach are becoming more important.

The key point is that these are not transformational deals, but incremental ones. That is often where value is created. Smaller, well integrated acquisitions can be absorbed quickly and contribute to earnings without introducing unnecessary risk.

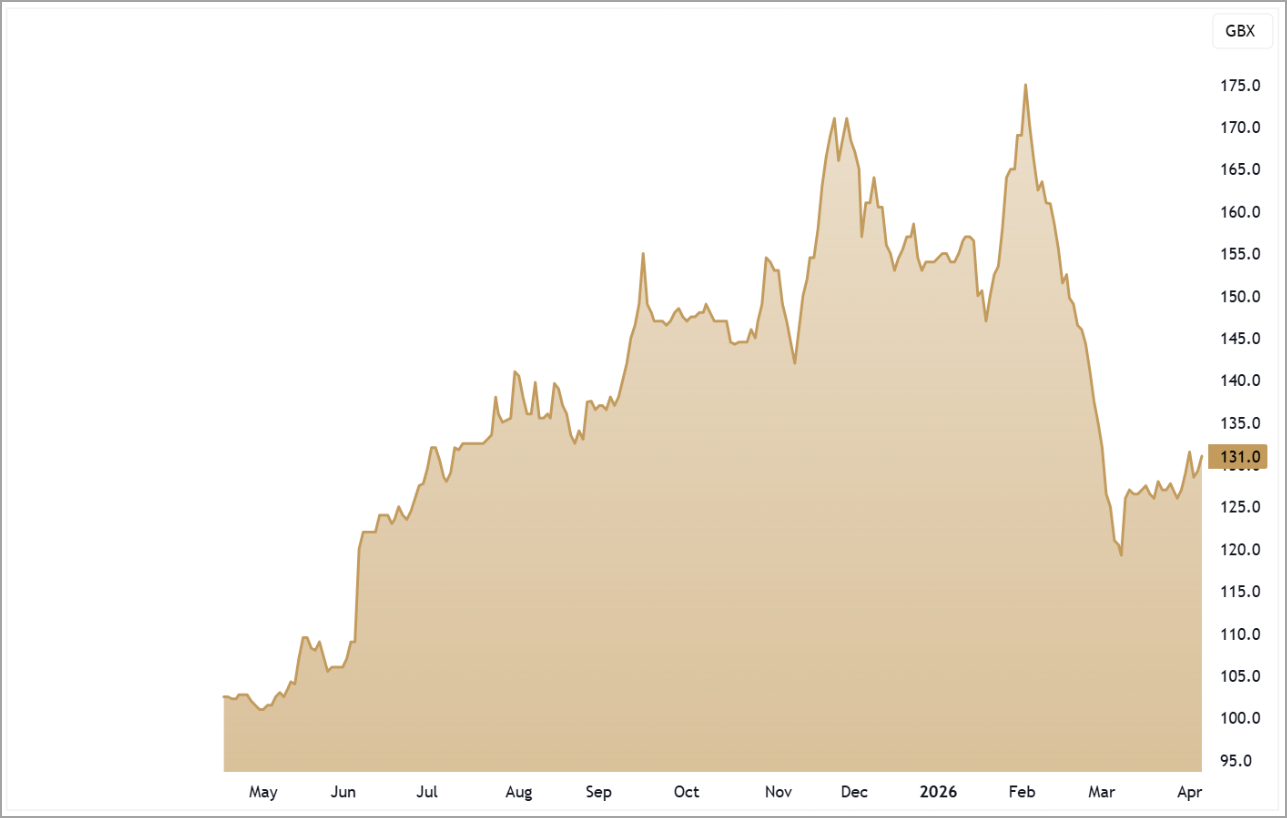

Price action following a post IPO peak

The chart has undergone a clear shift in structure over recent months. After trending higher from the IPO, the shares formed a double top in February before entering a deep pullback.

Since then, price has moved lower in a series of lower highs, with momentum clearly fading. However, this type of move is not unusual following a strong initial run, particularly as early positioning begins to unwind.

A useful way to frame the move is through Fibonacci retracement levels, which measure how much of a prior advance has been given back. In this case, the shares have retraced more than 70% of their post IPO rally and are now stabilising around key support levels. This is often where selling pressure begins to ease and the balance between buyers and sellers starts to shift.

At this stage, the chart suggests a transition rather than a breakdown. The earlier momentum phase has clearly ended, but the current price action points more towards consolidation than continued weakness.

Valuation now doing more of the work

The change in sentiment has brought valuation back into focus.

MHA now trades on around 5.2x EV to EBITDA and roughly 5x free cash flow, alongside a prospective dividend yield of about 4.3%. For a business delivering double digit growth, high returns and strong cash generation, that represents a more balanced entry point than was available during the initial post IPO rally.

The market appears to have reset expectations, even as the business continues to execute. That creates a different dynamic, where future returns are more likely to be driven by operational delivery rather than multiple expansion.

At current levels, the investment case is becoming simpler. The business continues to perform, the strategy is progressing, and the valuation is no longer demanding. The story here has not changed, only the price.

Five Key Takeaways

1. Valuation reset: The shares have retraced more than 70% of their post IPO rally despite continued execution

2. Consistent delivery: Revenue growth, margins and cash generation remain firmly on track

3. Strategy progressing: The UAE acquisition reinforces a clear and repeatable international expansion plan

4. Strong fundamentals: High recurring revenue and returns support a resilient and cash generative model

5. Improved entry point: Around 5.2x EV to EBITDA and a 4.3% yield offer a more attractive valuation

MHA 1yr Chart

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.