11th Sep 2025. 9.05am

Regency View:

BUY MHA (MHA)

Regency View:

BUY MHA (MHA)

MHA’s Successful AIM IPO

AIM IPOs are often overhyped and underdeliver, spiking on day one then fading when reality catches up. MHA has taken a different path…

Since listing in April the shares have built steadily on strong numbers, sticky revenues and a clear plan to scale as a genuine challenger to the Big Four.

From Victorian roots to modern challenger

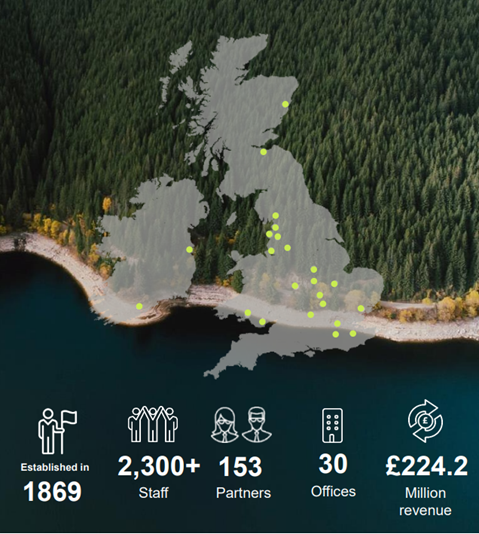

MHA may trace its history to the 1860s, but the listed story is very much about the next chapter. The firm operates across four divisions that cover Audit and Assurance, Tax, Accounting and Business Advisory, and Wealth Management. That breadth gives MHA multiple entry points to win and deepen client relationships across a wide set of industries.

Recurring revenue is the foundation. About 87% of fees are recurring, tied to activities that clients need in all parts of the cycle. That provides visibility and cushions the business when conditions get choppy. It also sets up natural cross sell across divisions as relationships widen over time.

Scale matters in this market and MHA now employs more than 2,300 people across 30 offices with 153 partners. As the UK member of Baker Tilly International, the firm can pitch for larger mandates with global reach while keeping the agility of a mid tier operator. It is a useful middle ground that lets MHA win work from companies that might default to the Big Four but want responsiveness and value.

Buying growth the smart way

Management is leaning into a fragmented market with selective acquisitions. The standout move so far is Baker Tilly South East Europe, completed in August for about €24m in cash and shares. This adds Cyprus and Greece and broadens the regional footprint, creating more scope for cross border referrals and sector depth.

The IPO provided meaningful firepower. With £98m raised, MHA can fund disciplined deals that fit culturally and add earnings, rather than chase size for headlines. The playbook is to integrate quickly, align controls and unlock scale benefits. The group has a long record of doing exactly that.

Investing in tomorrow’s tools

The second engine is technology. Around half of staff now use AI or automation tools in some form, with tax the most advanced area. Automation is streamlining document processing and report generation, which frees capacity for higher value work and helps margins.

The firm is also building a unified data architecture that brings finance, HR and client systems onto one backbone. Better forecasting, clearer performance tracking and faster decision making should follow. That is how you scale professional services without letting overheads swell, and it supports the goal of being a £500m revenue business in the medium term.

Broad based growth at a bargain basement price

The latest full year numbers tell the story. For the year to March 2025 revenue rose 45% to £224m. Adjusted earnings increased 33% to £41.1m and adjusted profit before tax rose 31% to £36.3m. Operating margins held firm at about 36% and cash conversion was 91%. In a sector where utilisation and lock up can bite, that is a strong combination of growth and discipline.

Growth was broad based. Audit and Assurance remains the engine, while advisory work accelerated as clients sought restructuring and corporate finance support. Sector diversity helps smooth the bumps, with contributions from real estate and construction, retail and consumer, financial services, technology, healthcare and more. Client retention remains high, which keeps the growth flywheel spinning.

Valuation is part of the appeal. On trailing numbers the shares sit on a price to earnings ratio of 4.6. Return on capital is about 73% and return on equity is about 200%. Those figures are unusual for a newly listed AIM company of this size. Net cash of £17.7m supports the balance sheet and the first dividend is expected with the interim results. Current market expectations look sensible with revenue guided to about £240m in the new year and adjusted EBITDA around £42.2m.

The IPO was also a statement of intent. It was the largest AIM float of 2025 and the biggest in professional services for five years. Beyond the capital, the listing has lifted profile with clients and acquisition targets and has aligned partners and investors under one structure. That alignment matters when the strategy relies on consistent delivery over multiple years.

Momenutm builds on IPO success

The technical picture matches the fundamentals. Rather than a pop and fade, the chart shows a staircase higher since April. Pullbacks have been orderly and buyers have stepped in ahead of the 50 day moving average through the summer. That behaviour looks like accumulation rather than hot money trading the headline.

The latest consolidation in August has resolved higher with the shares pressing fresh highs in September. Momentum remains supportive while the trend structure holds. As long as the market respects support zones that have formed during prior pauses, the path of least resistance stays up while the operational story converts into earnings and cash.

MHA looks like an AIM floatation done right. You get defensive recurring revenues, broad based growth, robust cash generation and a balance sheet that can fund disciplined M&A and technology investment. Add the Baker Tilly network for reach and credibility and you have a challenger that can keep taking market share from bigger rivals. We’re more than happy to add MHA to our list of AIM Investor open positions.

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.