9th May 2025. 10.55am

Weekly Briefing – Friday 9th May

| Market | Movement this week (%)* |

|---|---|

| FTSE 100 | +0.89% |

| FTSE 250 | +1.82% |

| FTSE All-Share | +1.02% |

| AIM 100 | +3.45% |

| AIM All-Share | +3.10% |

* Price movement from Monday's open at 8am

Regency View:

Weekly Briefing – Friday 9th May

Market Overview

Dear Investor,

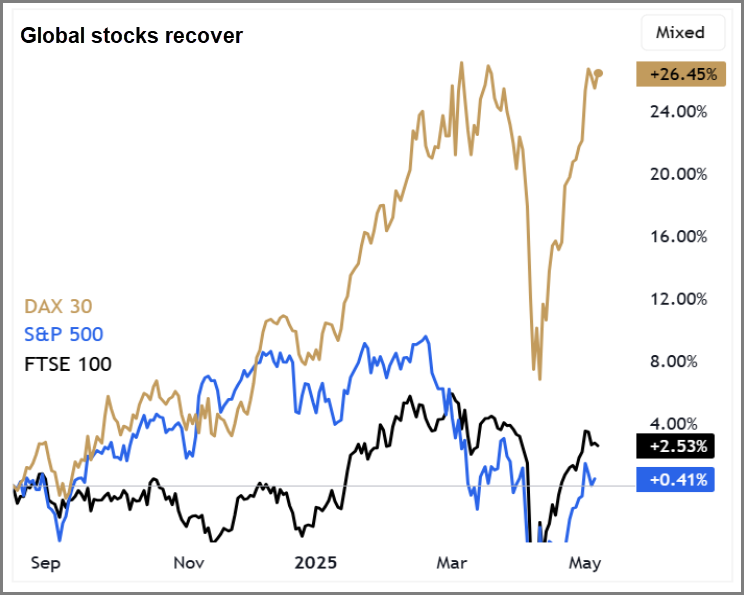

With the FTSE having erased its ‘liberation day’ losses and earnings season getting off to a strong start, investors would be forgiven for thinking “what trade war?” The reality, however, is that the full impact of Trump’s tariffs hasn’t disappeared — it’s just taking a little longer to show up in the places that matter.

Let’s start with the Bank of England. The rate cut to 4.25% wasn’t just about inflation trends. Governor Andrew Bailey has been increasingly vocal about the risks to growth posed by global trade uncertainty. This latest move marks the fourth cut since August, and it’s clear the Bank is acting early to soften the blow from the policy shifts coming out of Washington. When central banks start cutting ahead of confirmed damage, it tells you the risk environment has changed.

That message is echoed by the companies who’ve just reported. From Nestlé and Mercedes-Benz to Unilever and Primark, we’re seeing a consistent theme in earnings calls: uncertainty is doing the real damage. The tariffs themselves are only part of the story. The bigger issue is that CEOs don’t know what comes next. Forecasts are being pulled, investment plans delayed, and long-term strategies put on ice. If you run a global supply chain, you can’t just pivot overnight because a policy was announced on a Tuesday.

There’s also the matter of currency volatility, which is already biting. Unilever flagged the sharp moves in dollar-euro exchange rates as a source of real financial stress. It’s not just the tariffs — it’s the knock-on effects across FX markets, consumer sentiment, and the broader demand outlook. Meanwhile, EU-US trade talks remain stuck in the mud, and retaliatory tariffs from Brussels are now on the calendar for early July.

So while the FTSE may have bounced and early earnings have soothed nerves, this isn’t a story with a neat ending. Under the surface, companies are telling us they’re flying blind. There’s a big difference between a share price recovery and business-as-usual. As always, we need to read beyond the headlines — and listen closely to what’s not being said.

Wishing you a fantastic weekend,

Tom

Thomas Light – Chartered FCSI

Director of Research

Market Movers

On the rise: InterContinental Hotels Group (LSE:IHG) +4.5% on the week

InterContinental Hotels Group has seen its share price surge over 18% since mid-April, driven by expectations of a strong first-quarter trading update for 2025. The company didn’t disappoint, delivering solid results with a 3.3% global increase in revenue per available room (RevPAR). Strong performances in the Americas and EMEAA regions offset some challenges in Greater China, demonstrating IHG’s ability to capture demand across multiple markets.

The update highlighted robust growth across all key segments. Business travel revenue grew by 3%, leisure by 2%, and group bookings surged by 5%, signalling broad-based demand recovery. IHG’s diversified portfolio and global reach helped drive these results, showcasing the strength of its brands. The company also reported significant development activity, opening 14.6k rooms in Q1—double last year’s total—reinforcing its aggressive expansion strategy.

IHG’s development pipeline continues to thrive, with 25.8k rooms signed across 158 properties in Q1, marking a 9.4% year-on-year increase. The acquisition of the Ruby brand added 5.7k rooms, further bolstering its portfolio. With such a strong pipeline, IHG is well-positioned to benefit from the global travel recovery.

Looking ahead, IHG remains confident in meeting profit expectations for 2025, despite some economic uncertainty. Its asset-light, fee-based model, coupled with strong cash generation, ensures resilience. The company’s solid market position and ongoing growth prospects, backed by a share buyback program, provide a strong foundation for the rally to continue.

REGENCY VIEW:

InterContinental Hotels solid fundamentals, with a PE ratio of 22.3 and an impressive operating margin of 21.15%, indicate a company capable of strong profitability. Despite the shares weak start to the year, the 19.2% forecasted EPS growth suggests there’s still potential for growth, making it one to watch.

Shares in ZOO Digital dropped this week following the release of a trading update that highlighted a weaker-than-expected financial performance and a cautious outlook for the year ahead.

While the company reported a 22% rise in revenue to $49.4 million for FY25, this came in below market expectations of $50.7 million, and adjusted EBITDA only just turned positive at $0.1 million—well short of the anticipated $1.5 million. The update also confirmed that several high-value projects were not delivered in the fourth quarter, pushing revenues into the next financial year and complicating near-term forecasting.

Despite stronger-than-expected net cash of $2.6 million, investor sentiment was dented by the warning that FY26 revenues are likely to fall short of previous expectations. ZOO is continuing to restructure its operations to remain profitable on a lower revenue base, including over $6.8 million in cost savings implemented in FY25 and a further $1.7 million planned for FY26. Management flagged persistent headwinds in the media and entertainment sector, ranging from disrupted production cycles to emerging geopolitical risks—including potential new US tariffs on foreign-made films.

This combination of softer guidance, operational restructuring, and revenue deferrals appears to have triggered renewed market concerns about visibility and earnings momentum in the year ahead.

REGENCY VIEW:

Zoo Digital’s stock has tumbled more than 80% over the past year, reflecting ongoing struggles with profitability and weak returns. While its low price-to-sales ratio may appeal to value seekers, the company’s speculative nature and challenging market conditions make it a risky play.

Sector Snapshot

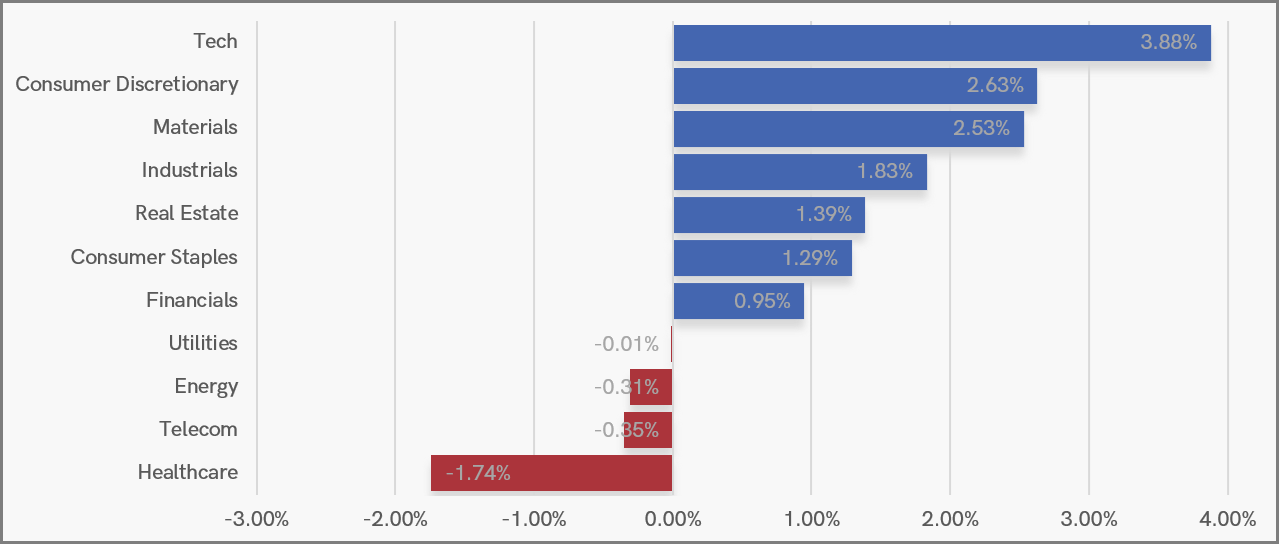

Technology remained in pole position this week, but the real shift came in the form of a quiet comeback from Materials and Consumer Discretionary — a sign that investors are broadening their exposure to include more cyclical and commodity-linked names. Industrials also found support, helped by stable macro signals and renewed interest in infrastructure-led plays.

At the back of the pack, Healthcare drifted lower as investors stepped away from defensive growth, while Telecoms and Energy slipped slightly in quiet trade. The tone of the market suggests rotation rather than retreat, with appetite building beyond mega-cap tech and into the next layer of opportunity.

UK Sector Performance (7-Days)

UK Price Action

The FTSE held its ground this week, but there are hints the recovery might be starting to lose momentum. Tuesday saw a brief push higher, only for the market to fade and close lower—forming a small bearish engulfing candle. It’s not a game-changer on its own, but it does suggest a touch of fatigue creeping in.

FTSE 100 Rolling Futures (Daily Candle Chart)

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.