9th Jan 2026. 10.24am

Weekly Briefing – Friday 9th January

| Market | Movement this week (%)* |

|---|---|

| FTSE 100 | +1.34% |

| FTSE 250 | +2.24% |

| FTSE All-Share | +1.44% |

| AIM 100 | +2.92% |

| AIM All-Share | +2.58% |

* Price movement from Monday's open at 8am

Regency View:

Weekly Briefing – Friday 9th January

Market Overview

Dear Investor,

Happy New Year!

Our first full week back in the markets has seen Donald Trump’s oil grab in Venezuela dominate headlines, yet for all the noise, financial markets have barely flinched. Crude prices have been surprisingly well behaved and broader risk appetite has held up, a reminder that not every geopolitical flashpoint translates into immediate market stress. With that in mind, this felt like a good moment to step back from the headlines and focus on what could really shape returns for UK investors in 2026.

The most obvious and ever present theme remains AI. The debate around bubble or not will no doubt intensify, particularly as valuations in parts of the market look demanding. But one development that feels far more durable is the broadening of AI away from a handful of headline grabbing builders towards the businesses actually using it to improve productivity, protect margins and sharpen their competitive edge. For UK investors, this is where the opportunity set widens meaningfully, as many of these beneficiaries sit outside the US mega cap space and closer to home in software, industrials, defence and services.

Alongside this, value and income are quietly regaining their appeal. Interest rates have been coming down for over a year and while the Bank of England remains cautious, the direction of travel is clear. At the same time, the FTSE sits at all time highs and is trading on a multiple well above its recent average. In that environment, dependable cash generation, resilient dividends and sensible balance sheets start to matter more again. For a market like the UK, which is rich in these characteristics, that creates a supportive backdrop for patient investors.

That leads neatly to the third and perhaps most important theme. With valuations elevated and returns likely to be harder earned, stock selection is set to matter far more than simply chasing the index. Some businesses will justify higher multiples through earnings delivery and strategic positioning. Others will struggle. The gap between winners and losers is likely to widen, and this is where a disciplined, selective approach can really add value.

Taken together, these themes point to a market that rewards focus rather than frenzy. AI is evolving, income is relevant again, and careful stock picking looks set to trump blind exposure. Taken together, it points to a year where selectivity and discipline matter far more than simply being invested.

Wishing you a very happy and successful year ahead,

Tom

Thomas Light – Chartered FCSI

Director of Research

Market Movers

On the rise: BAE Systems (LSE:BA.) +16.6% on the week

Shares in BAE Systems rose this week as defence spending moved back to the centre of political focus. President Donald Trump called for US defence spending of $1.5trn next year and said US contractors should pause dividends and buybacks until weapons production accelerates. That stance weighed on US defence stocks but lifted sentiment towards European names, where investors see fewer constraints and greater flexibility.

European aerospace and defence stocks pushed to fresh highs, extending a rally that has been building for several years. The sector continues to benefit from the reality that defence budgets are rising structurally, not cyclically, as governments respond to persistent geopolitical risk. BAE led gains among UK-listed peers, reflecting its scale, breadth of capabilities and deep links with the US defence market.

BAE’s exposure to the US looks particularly relevant in this context. If restrictions on capital returns persist for US contractors, it may encourage a shift in contracts, partnerships and investor capital towards non-US suppliers that can deliver at scale. That dynamic adds another tailwind to a sector that is already operating with strong demand visibility.

Regency View: BAE remains a key name for our FTSE Investor product. The valuation reflects its strategic importance, but strong cash generation, resilient margins and long-term visibility continue to justify its place in a portfolio built for an uncertain world.

Shell slipped this week as the group flagged a loss in its chemicals and products division for the fourth quarter, a reminder that downstream earnings remain under pressure. While upstream oil, gas and LNG production guidance was left unchanged, the market focused on softer refining margins and the drag from chemicals.

The weakness was compounded by a broader pullback across European energy stocks after oil prices dipped. Crude moved lower following President Trump’s announcement of an agreement with Venezuela that could bring additional supply back to the market, nudging Brent down around 1% and taking much of the sector with it.

In isolation, the update was not dramatic, but in a market that has become increasingly sensitive to marginal changes in oil prices, Shell’s shares reacted accordingly. With energy stocks having enjoyed a strong run at points over the past year, any hint of softer earnings momentum is being met with a quick reassessment.

Regency View: Shell remains a high-quality, cash-generative major, but this week’s move underlines how exposed the shares are to short-term swings in oil prices and downstream margins. For now, we prefer exposure elsewhere in the UK energy space, where the risk-reward looks more compelling.

Sector Snapshot

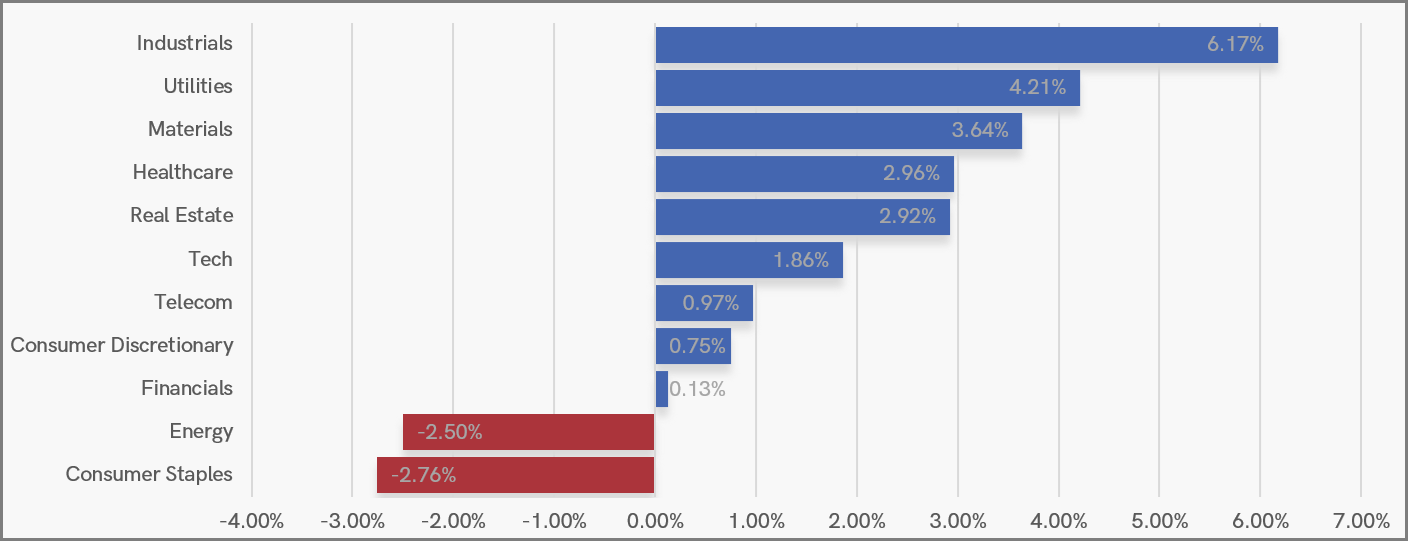

Industrials topped the table this week, boosted by strong moves in defence stocks following Donald Trump’s military action in Venezuela. Utilities also performed well, potentially helped by Storm Goretti in the UK, which has brought renewed focus on domestic infrastructure and grid resilience. Materials, Healthcare and Real Estate added to the upside, giving the rally some breadth.

Energy was the clear laggard, likely weighed down by political uncertainty around Venezuela and concerns over supply dynamics. Consumer Staples also slipped, suggesting investors favoured event-driven and cyclical themes over traditional defensives as the week unfolded.

UK Sector Performance (7-Days)

UK Price Action

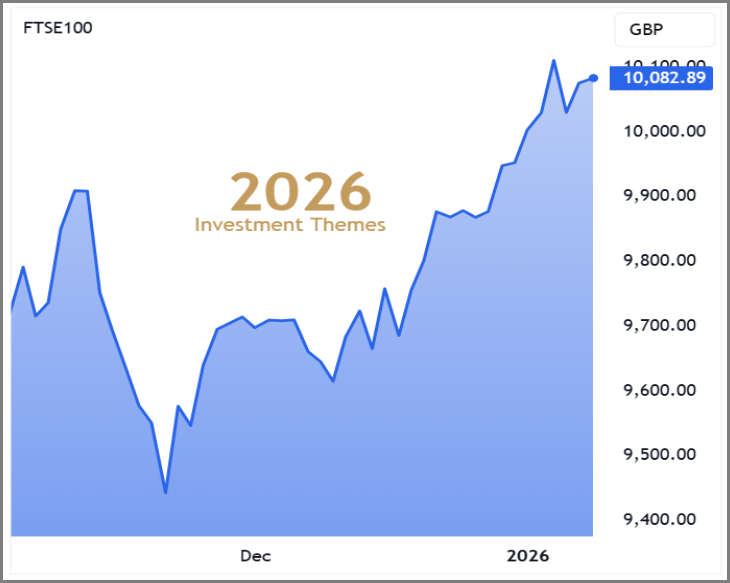

The FTSE has started the new year by breaking to fresh trend highs, and importantly this move has held through the week as volume returned to the market. That combination of price expansion and renewed participation is a constructive signal and suggests the breakout is being accepted rather than faded.

Our baseline assumption remains that broken resistance should now transition into support as the trend progresses. As long as the index continues to hold above the prior highs, the path of least resistance remains higher, with any near term pullbacks likely to be viewed as opportunities rather than threats to the broader uptrend.

FTSE 100 Rolling Futures (Daily Candle Chart)

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.