6th Mar 2026. 10.33am

Weekly Briefing – Friday 6th March

| Market | Movement this week (%)* |

|---|---|

| FTSE 100 | -4.49% |

| FTSE 250 | -4.46% |

| FTSE All-Share | -4.44% |

| AIM 100 | -4.30% |

| AIM All-Share | -3.82% |

* Price movement from Monday's open at 8am

Regency View:

Weekly Briefing – Friday 6th March

Market Overview

Dear Investor,

A week like this can test the resilience and mindset of even the most seasoned long term investor. The 24 hour news cycle has a way of pulling market participants into the emotion of events as they unfold in real time. During weeks like the one just gone, perspective, context and patience are often your greatest allies. It is very easy to get caught up in the blow by blow commentary, but the market rarely rewards decisions made in the heat of the moment.

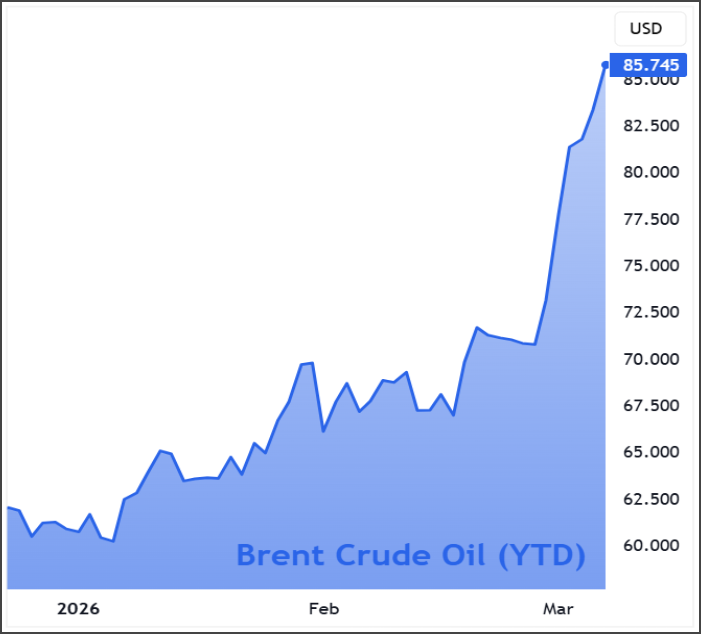

The moves across markets over the past few sessions reflect that tension. Oil has pushed higher as traders price in the risk of disruption across the Gulf, the US dollar has firmed as global capital drifts toward safety, and European equities have taken a breather after a strong run. The DAX has felt the pressure more than most, while the FTSE has held up relatively well thanks to its heavy weighting in energy, mining and defensive sectors.

Across the Atlantic the picture looks a little calmer. The S&P 500 continues to chop sideways near its highs rather than breaking down in panic. That sort of price action often tells you that investors are still assessing the situation rather than rushing to reprice the entire economic outlook. Markets tend to move fastest when uncertainty suddenly disappears. Right now we are still firmly in the uncertainty phase.

From a macro perspective the real question is what happens to energy prices if tensions persist. Sustained strength in oil rarely stays confined to the commodity markets for long. It gradually feeds into inflation expectations, complicates the outlook for central banks and eventually works its way into consumer spending and business confidence.

For long term investors the challenge is always the same during moments like this. The headlines become louder, the price swings become sharper and the temptation to react becomes stronger. Yet history shows that the bigger drivers of returns tend to remain earnings growth, liquidity and the broader economic cycle. In other words, the things that rarely change overnight, no matter how dramatic the newsflow may feel at the time.

Wishing you a calm and considered weekend,

Tom

Thomas Light – Chartered FCSI

Director of Research

Market Movers

On the rise: Thungela Resources (LSE:TGA) +31.5% on the week

Shares in coal producer Thungela Resources moved higher this week despite the company issuing a trading statement pointing to a headline loss for the year ended December 2025. The expected loss was driven primarily by a large non-cash impairment of around R8.8 billion across its South African and Australian operations, reflecting weaker forward coal price assumptions and a stronger outlook for local operating currencies against the US dollar.

The impairment follows a softer year for seaborne thermal coal prices, with benchmark prices at Richards Bay and Newcastle falling as demand from key import markets eased and global supply remained robust. Importantly, the company stressed that these accounting adjustments do not impact cash generation or operational continuity, and the write-downs largely relate to historical capital invested in assets approaching the end of their economic lives.

Beyond the headline figures, the underlying business continues to generate strong cash flow and maintain a robust balance sheet. Thungela also remains attractively valued relative to peers, with the shares trading on low earnings multiples and continuing to rank highly across quality, value and momentum factors, reflecting ongoing investor appetite for cash-generative commodity producers.

Regency View: Sometimes the most bullish news is the market’s reaction to what initially looks like bad news. The impairment may dominate the headlines, but the strong share price response suggests investors are looking straight through the accounting noise and focusing on Thungela’s underlying cash generation and valuation

Reckitt’s latest results were solid on the surface, but the shares slipped as investors looked a little deeper into the detail. The consumer goods group reported like-for-like revenue growth of 5.4% in the fourth quarter, ahead of expectations, capping a year in which underlying sales grew around 5% and operating profit edged higher.

The real momentum continues to come from emerging markets, where revenues surged more than 14% during the year. Those regions are now responsible for a significant portion of the group’s growth, helping to offset a far more subdued performance across developed markets. Europe in particular remains a difficult trading environment, with revenues falling as consumers remain cautious and competition across household and healthcare products intensifies.

Management is guiding for core revenue growth of around 4% to 5% in 2026, although the near-term outlook is slightly clouded by a softer cold and flu season which could weigh on demand for its seasonal healthcare products. At the same time, the company is continuing to reshape its portfolio after completing the sale of its Essential Home division, a move designed to focus the business on higher growth brands and categories.

Regency View: Reckitt remains a high-quality global consumer business, but the market is clearly wrestling with the balance between dependable brands and modest growth. When expectations are set high, even a decent set of results can struggle to excite investors.

Sector Snapshot

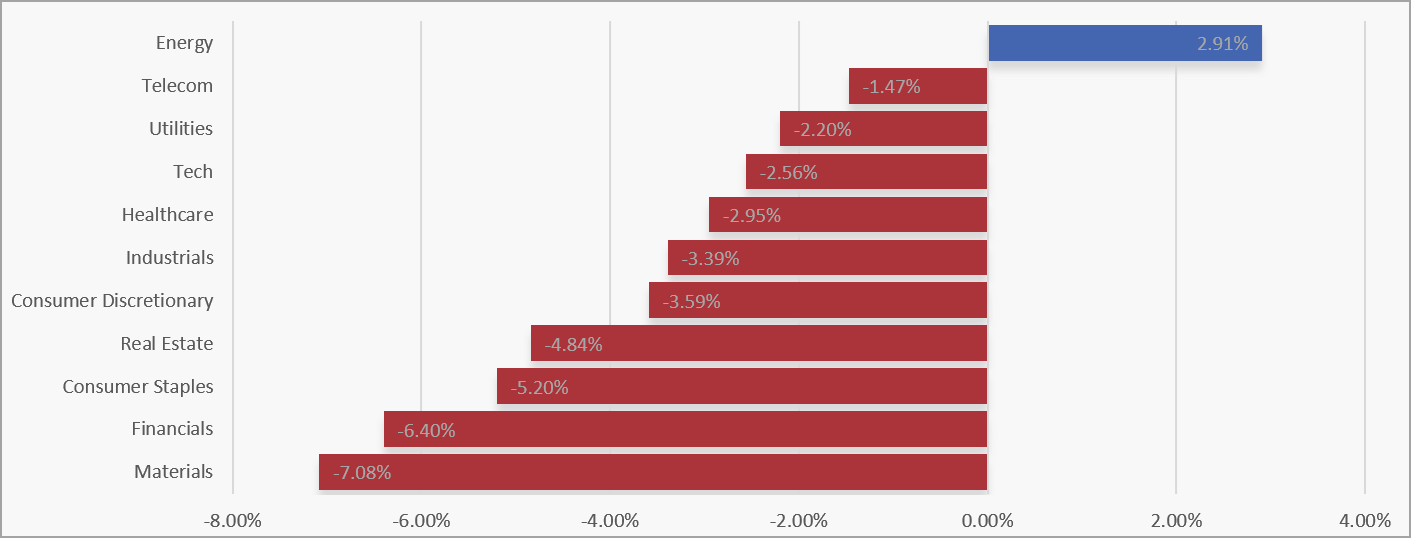

Energy was the only sector to post gains this week, standing out clearly as strength in oil prices supported the space while the rest of the market struggled. The divergence was stark, with most other sectors slipping lower as investors pulled back from risk and rotated away from cyclical exposure.

Financials and Materials were among the weakest performers, with Real Estate, Industrials and Consumer Discretionary also under heavy pressure. Even the traditional defensive areas such as Consumer Staples, Healthcare and Utilities failed to provide shelter, highlighting just how broad the risk-off move has been.

UK Sector Performance (7-Days)

UK Price Action

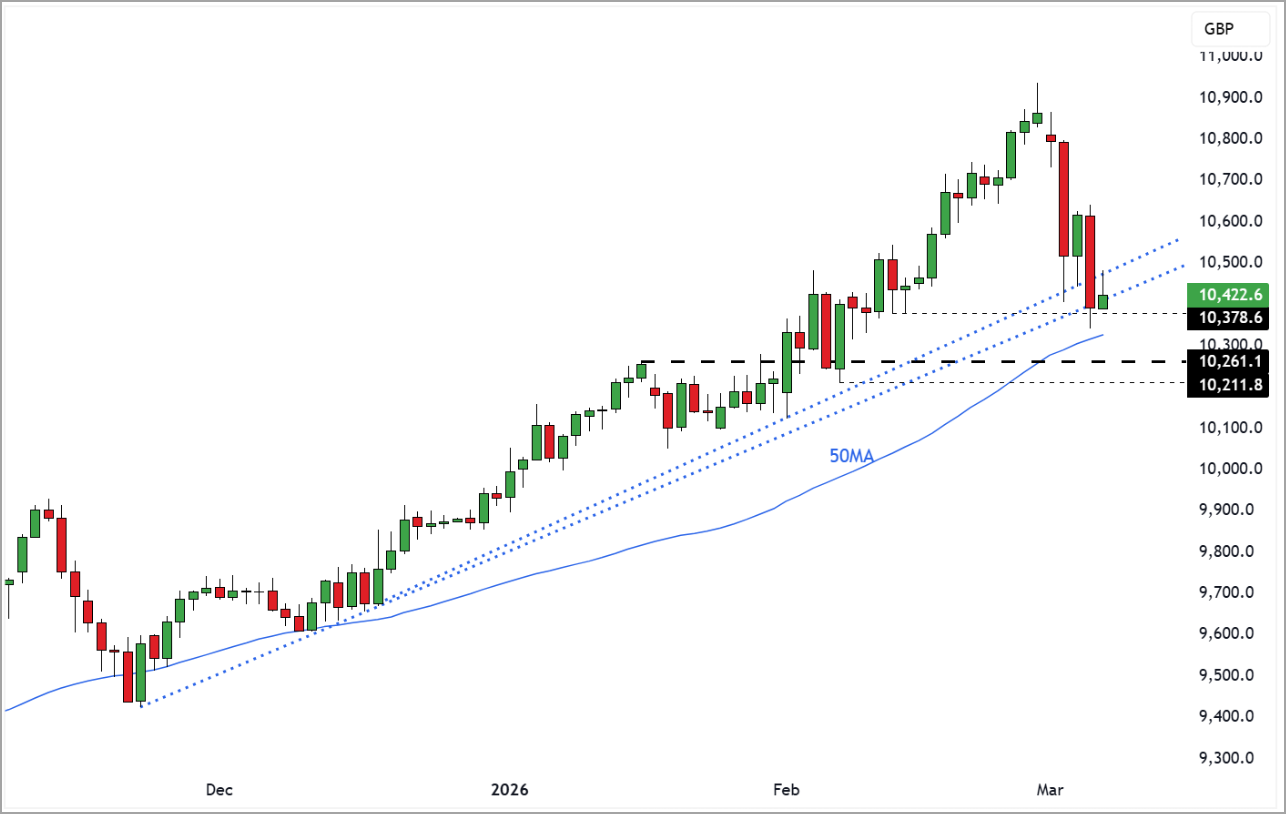

The FTSE has experienced its first proper trend test of the year this week as global risk appetite spiked in the wake of the Iran conflict. The sell off knocked prices away from their highs and briefly broke the steepest of the rising trendlines that had been guiding the advance, but from a technical standpoint there is no need to get overly dramatic just yet. Price has so far stabilised around the prior breakout zone and nearby support cluster, and as long as buyers continue to defend this region the broader uptrend remains firmly intact with the latest volatility looking more like a routine shakeout than the start of something more serious.

FTSE 100 Rolling Futures (Daily Candle Chart)

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.