6th Feb 2026. 11.10am

Weekly Briefing – Friday 6th February

| Market | Movement this week (%)* |

|---|---|

| FTSE 100 | +0.93% |

| FTSE 250 | -0.62% |

| FTSE All-Share | +0.75% |

| AIM 100 | -2.78% |

| AIM All-Share | -2.27% |

* Price movement from Monday's open at 8am

Regency View:

Weekly Briefing – Friday 6th February

Market Overview

Dear Investor,

This week the political discourse and currency volatility have been much closer to home. With Sir Keir struggling to maintain control in Westminster, sterling wobbled as investors briefly re-priced political risk that had been sitting quietly in the background.

That move filtered through to gilts too, but the broader equity market response was notably calm. UK stocks have continued to grind higher, and that resilience says more about what is happening within the market than any single headline. Rather than chasing momentum, investors have been rotating capital between sectors, keeping the overall trend intact.

We have seen that clearly in recent weeks. Early leadership from materials has faded, with leadership rotating towards more defensive areas such as healthcare, consumer staples and utilities. Cyclical sectors have cooled rather than broken, allowing the FTSE to continue pushing higher without the sort of frothy price action that often precedes sharper pullbacks.

Earnings season has added another layer to that story. Trading updates from major names on both sides of the Atlantic have kept attention firmly on company delivery rather than macro noise. Results from groups such as Shell and Anglo American at home, alongside updates from US heavyweights including Amazon and Alphabet, have reinforced the idea that fundamentals still matter in a market driven by selective leadership.

Taken together, it feels less like a market running hot and more like one quietly reallocating capital. Currency moves and politics will continue to create short-term volatility, but as long as sector leadership keeps rotating rather than breaking down, the underlying tone for UK equities remains steady rather than stretched.

Wishing you a fantastic weekend,

Tom

Thomas Light – Chartered FCSI

Director of Research

Market Movers

On the rise: Anglo American (LSE:AAL) +4.2% on the week

Anglo American hit new trend highs this week as its latest production report reminded the market why the miners have been doing the heavy lifting for the FTSE. Copper and premium iron ore both delivered a strong finish to 2025, with management pointing to higher grades and solid plant performance in Chile, while Collahuasi hit record throughput, helping keep full year output within guidance.

The real story sits in the forward view. Anglo has temporarily restarted a second plant at Los Bronces on the back of a firmer copper price environment, aiming to offset a softer patch expected at Collahuasi in 2026. Guidance then steps up from 2027, with maiden 2028 targets pointing to materially higher Chilean copper volumes versus 2025, while Quellaveco continues to do what investors want from a tier one asset: churn out cash, with capital payback targeted in 2026.

Alongside the operational update, the portfolio reshape keeps rolling. The sale process for steelmaking coal is moving along, De Beers is heading towards separation, and management flagged that De Beers is likely to be loss making in 2025 with an impairment review under way. It is not all sunshine, but the market tends to forgive the messy exit lanes when copper and iron ore are behaving and the medium term production path is improving.

Regency view: Anglo’s momentum has been driven by the right commodity at the right time, with copper pricing doing the talking and operational execution keeping the narrative tidy. Valuation is no longer cheap on headline multiples, so the shares will likely stay sensitive to any wobble in copper or further guidance trims, but the direction of travel on production beyond 2026 is the key support for the current trend.

Sage shares came under pressure this week as a broader sell-off swept through European software and data analytics names. The trigger was not company-specific news, but a renewed bout of AI anxiety after the launch of new generative tools raised questions about how defensible incumbent business models really are.

The spark came from Anthropic’s latest upgrade to its Claude platform, particularly its legal plug-in, which prompted sharp falls across the sector. Investors began reassessing whether established software providers can earn an adequate return on heavy AI investment, or whether faster-moving challengers risk commoditising parts of their offering. That shift in sentiment dragged down a wide range of names, including Sage, as multiples compressed across the space.

Importantly, this has been a thematic move rather than a fundamental one. Sage has not issued a negative update, but in a market that is increasingly focused on clear and visible AI monetisation, even high-quality operators have found themselves caught in the downdraft as investors rotate away from perceived “AI incumbents” toward areas with more obvious near-term beneficiaries.

Regency view: Sage remains a high-quality business with strong cash generation and a deeply embedded customer base, but the market is clearly demanding clearer evidence of how AI translates into incremental revenues rather than just defensive positioning. For now, sentiment is doing the driving, not the numbers.

Sector Snapshot

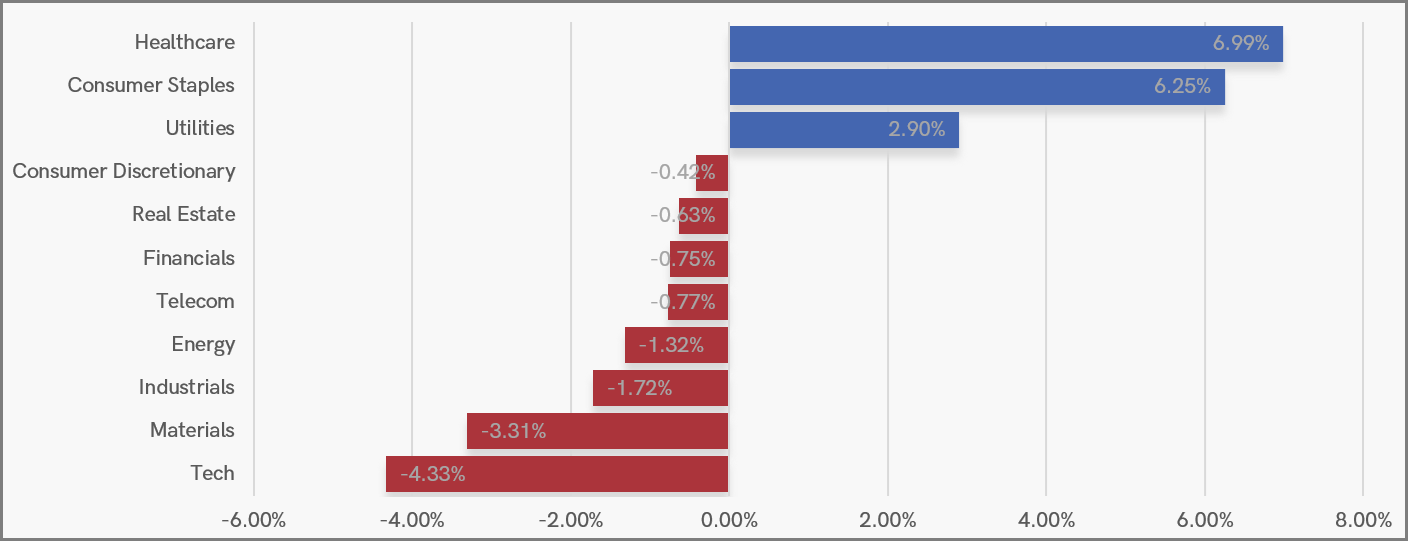

Healthcare and Consumer Staples dominated this week’s leaderboard, with Utilities also delivering a solid performance. The common thread across the leaders was a clear preference for sectors offering stable earnings and predictable demand, suggesting investors were once again leaning into defensives.

At the other end, Tech and Materials were the weakest performers, with Industrials and Energy also under pressure. Financials, Telecom and Real Estate slipped modestly, reinforcing the sense that appetite for growth and cyclical exposure has taken a back seat to stability.

UK Sector Performance (7-Days)

UK Price Action

The FTSE spent the latter part of January consolidating in a bullish ascending formation, compressing beneath resistance before finally breaking higher earlier this week. That breakout extended the broader uptrend and initially confirmed that buyers remained firmly in control.

Since then, Thursday’s pullback has brought prices back into the former breakout zone, an area that now sits firmly in focus as potential support. If this level holds, it would reinforce the idea of a healthy retest within an ongoing trend. If it fails, however, it would start to look more like a false break from the pattern and could signal that the market is due a deeper pullback before the uptrend can reassert itself.

FTSE 100 Rolling Futures (Daily Candle Chart)

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.