5th Sep 2025. 10.51am

Weekly Briefing – Friday 5th September

| Market | Movement this week (%)* |

|---|---|

| FTSE 100 | +0.57% |

| FTSE 250 | -0.13% |

| FTSE All-Share | +0.45% |

| AIM 100 | +0.15% |

| AIM All-Share | +0.36% |

* Price movement from Monday's open at 8am

Regency View:

Weekly Briefing – Friday 5th September

Market Overview

Dear Investor,

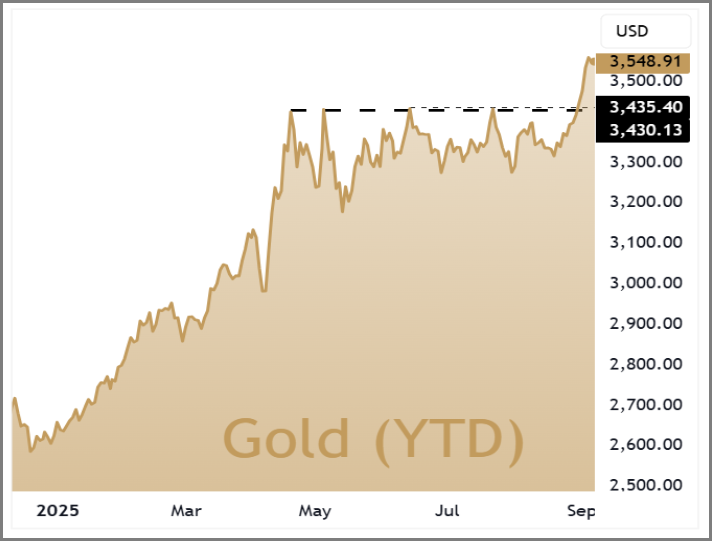

After a sleepy summer gold has sprung back to life this week, breaking above $3,500 an ounce and shaking off the sideways grind that dominated the past few months…

The move has caught our attention not just because the chart looks brighter, but because of what it says about the mood across global markets. When gold wakes up, it usually means investors are starting to take risk more seriously.

The spark came from Washington. Donald Trump’s decision to sack Fed governor Lisa Cook and ramp up his public feud with chair Jay Powell has put the independence of the world’s most important central bank in doubt. While the dollar has actually tracked sideways this week, it remains soft in the bigger picture, and the uncertainty swirling around US policy has been enough to help gold break higher.

This rally is not just about the dollar. Gold has always had a knack for sniffing out stress, and this time is no different. It has been moving in line with equity volatility, which is starting to perk up again after months of calm. More tellingly, the buying is being driven by central banks, ETFs and macro funds that allocate on a macro view rather than on price. That is a very different dynamic from the days when retail households in Asia were the swing factor, buying dips and selling strength. Today’s flows are stickier and less price sensitive, which explains why gold has marched from $2,000 to $3,500 in just 18 months.

You can see that shift in the mining sector too. Gold miners were left behind early in the move, but their share prices are now starting to catch up. That suggests investors are beginning to believe higher prices are here to stay, since miners only really work as a trade if you think the gold price will be sustained. Meanwhile, it makes sense that emerging market central banks are stepping up diversification away from the dollar. If you are running reserves, who better to recognise the risks of a captive Fed than another central banker.

For UK investors, the takeaway is simple. Gold’s breakout is a reminder that it remains a vital hedge when political risk, fiscal concerns and global rate uncertainty collide. Whether tomorrow’s payrolls print extends the rally or sparks a short pause, the bigger message is that gold is flagging risks about US debt and the dollar that equities and bonds are still choosing to ignore.

Wishing you a fantastic weekend,

Tom

Thomas Light – Chartered FCSI

Director of Research

Market Movers

On the rise: Shield Therapeutics (AIM:STX) +24.9% on the week

Shares in AIM-listed biotech Shield Therapeutics have been on the rise recently, following the release of a second-quarter trading update that reported a doubling of revenues. The company’s lead product, Accrufer, an oral iron replacement therapy, has seen increased adoption in the United States, where iron deficiency remains a common and often under-treated condition. This growth in sales reflects Shield’s expanding commercial presence and the effectiveness of its strategy to penetrate the U.S. market.

The company also announced its aim to achieve positive cash flow by the end of the year. This target marks a significant milestone in Shield’s financial development and has attracted attention from investors. Shield has implemented cost-control measures and formed strategic partnerships to support its commercial operations, which have contributed to its improved financial outlook. These developments have coincided with a more than 17 percent increase in the company’s share price this week.

Shield’s product Accrufer addresses a large patient population that requires iron supplementation but may not tolerate or prefer intravenous treatments. The convenience and tolerability of oral iron therapy have made Accrufer an appealing option for both patients and healthcare providers. Since the summer, Shield’s shares have risen more than three-fold, reflecting the market’s response to its commercial progress and revenue growth. The company’s position in the iron deficiency treatment market continues to strengthen as awareness and demand for Accrufer increase.

REGENCY VIEW:

Shield Therapeutics remains a high-risk, high-reward play in the biotech space, with strong revenue growth but deeply negative margins and no clear path to profitability yet. The company’s valuation metrics suggest investors are pricing in future success, but with a return on capital of -120% and no earnings forecasts available, caution is warranted until operational efficiency improves.

Shares in Jet2 dropped sharply this week following its AGM statement, where management flagged that earnings are likely to come in towards the lower end of consensus forecasts. The company reported strong summer capacity of 18.5m seats, up 8% on last year, with package holiday passengers rising 2% and flight-only travellers up 17%. However, the shift towards later bookings and tighter consumer spending left investors cautious, with markets quick to price in softer near-term profitability.

Jet2 has responded by exercising capacity discipline for the coming winter season, trimming its schedule from 5.8m seats to 5.6m while still maintaining year-on-year growth of 9%. This approach is designed to protect pricing and ensure sustainable load factors, but it also signals that management is prioritising margin stability over chasing volume in an uncertain environment. While average package holiday pricing remains firm, yields on flight-only tickets have needed additional marketing support to drive conversions.

Despite the near-term pressure, Jet2 continues to invest for the long haul, underpinned by a 146-strong Airbus A321neo order book stretching to 2035. The group also announced further board evolution with the appointment of Rachel Kentleton as Senior Independent Director. For investors, the message is clear: the model remains resilient and customer loyalty is strong, but the later booking trend and a cautious outlook for winter have raised questions about the pace of earnings growth in the year ahead.

REGENCY VIEW:

Jet2 might have hit some short-term turbulence, but on a forward PE of just 7.3 and an EV/EBITDA below 2, the valuation still looks grounded in value. Strong returns on equity and disciplined capacity management suggest the long-haul case remains intact for patient investors despite the recent sell-off.

Sector Snapshot

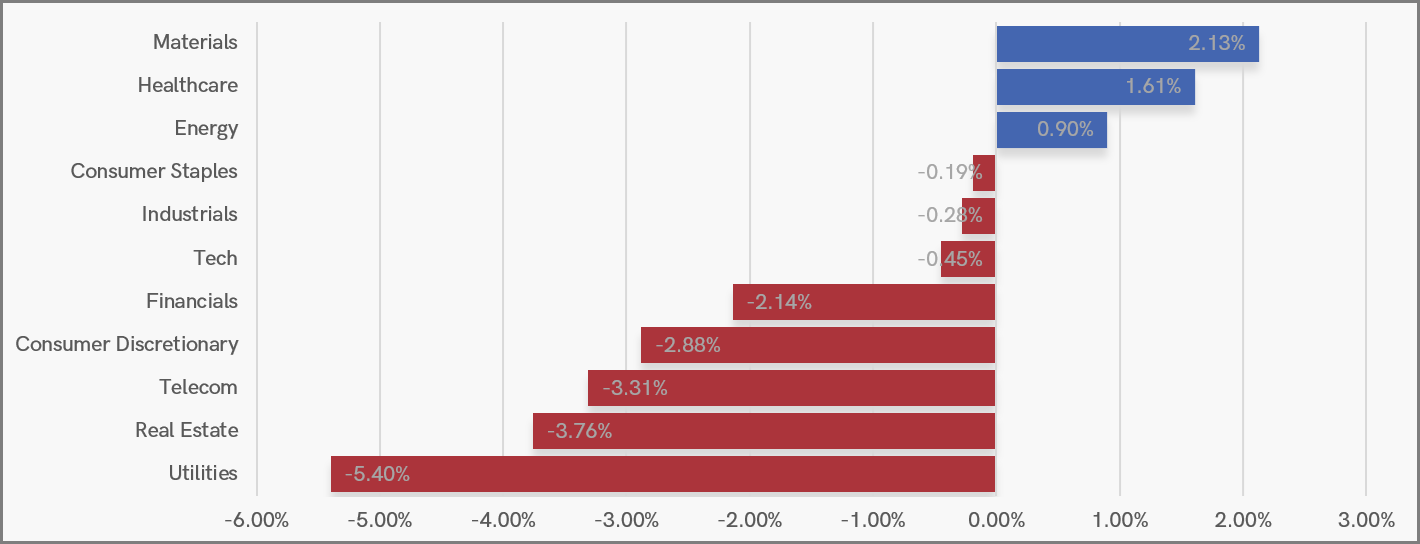

Materials led the market this week, with Healthcare and Energy also in positive territory, showing that investors were still willing to back sectors tied to earnings resilience and commodity exposure. Gains here contrasted with softer performances across most other areas, where momentum was harder to come by.

At the bottom of the table, Utilities, Real Estate and Telecom posted the steepest losses, highlighting weakness in traditionally defensive and rate-sensitive names. Financials and Consumer Discretionary also dragged lower, pointing to a cautious tone despite the support from a handful of outperforming sectors.

UK Sector Performance (7-Days)

UK Price Action

Last week we noted that the FTSE had pulled back to the top of its old range, with former resistance set to be tested as support. Recent sessions have shown signs of that support holding, and a close near or above Thursday’s high would create a fresh inflection point that bulls could interpret as a dip-buying setup.

FTSE 100 Rolling Futures (Daily Candle Chart)

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.