5th Dec 2025. 10.34am

Weekly Briefing – Friday 5th December

| Market | Movement this week (%)* |

|---|---|

| FTSE 100 | +0.04% |

| FTSE 250 | -0.04% |

| FTSE All-Share | +0.05% |

| AIM 100 | -0.38% |

| AIM All-Share | -0.12% |

* Price movement from Monday's open at 8am

Regency View:

Weekly Briefing – Friday 5th December

Market Overview

Dear Investor,

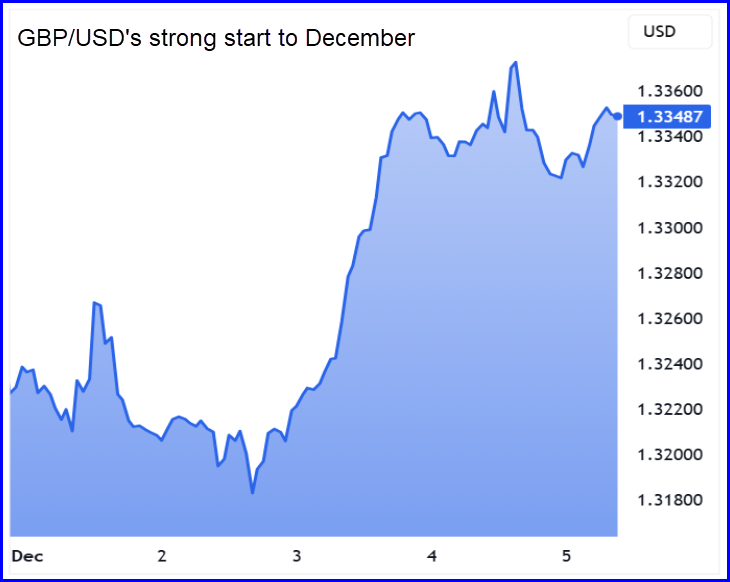

With global stocks treading water this week, most of the movement has been in currencies. Equity markets have been flat and hesitant, but FX has been lively, with sterling delivering its biggest daily rise since April and the yen prompting a reassessment of global funding conditions. In a week where equities drifted sideways, currencies have provided all the direction.

Sterling’s jump was driven by stronger UK economic data and a rapid unwinding of negative bets placed ahead of the Budget. The UK Composite PMI for November came in at 51.2 compared with expectations of 50.5, signalling a return to expansion. That single upside surprise gave investors more confidence in the domestic picture and helped stabilise sentiment that had looked fragile only a fortnight ago.

Positioning amplified the move. Many traders had built short positions on the pound before the Budget only to be caught by a combination of improving data and a softer US dollar. US private payrolls fell by 32,000 in November and President Trump’s hint that Kevin Hassett could become the next chair of the Federal Reserve pushed markets to price in faster rate cuts. The dollar weakened 0.5% against a basket of major currencies, helping sterling hold on to its gains.

The other notable shift this week came from Japan, where the Bank of Japan signalled that another rate rise may be on the way before year end. Japanese government bond yields moved higher and the yen briefly strengthened, prompting investors to revisit the risks tied to the long running yen carry trade. The reaction across global markets was modest, yet the message was enough to remind investors that changes in Japanese policy can influence global funding conditions.

For UK investors this matters because Japan is the largest holder of US Treasuries and rising local yields can reduce demand for overseas debt at a time when issuance is already elevated. Sterling may be finding its footing again, yet global currency dynamics remain fluid and the next decisive move could come from Tokyo rather than Washington.

Wishing you a fantastic weekend,

Tom

Thomas Light – Chartered FCSI

Director of Research

Market Movers

On the rise: BHP Group (LSE:BHP) +7.5% on the week

BHP pushed higher this week as copper prices reached fresh record levels. Benchmark copper on the London Metal Exchange rose 0.4% to $11,235 per tonne after touching an all time high of $11,294.5. The move was driven by expectations that major Chinese smelters will cut output in 2026 and by continued dollar softness following weak US economic data.

The strength in copper was part of a broader rally in mining names. Global peers including Rio Tinto and Southern Copper also traded firmer, while Australia’s mining sub index reached its highest level since October. Iron ore prices added further support, rising for a fourth consecutive session on strong buying interest for medium grade cargoes. The combination of higher copper and firmer iron ore pushed sentiment across the diversified mining sector into positive territory.

BHP’s trading metrics remain solid. The shares continue to sit above both their 50 day and 200 day moving averages and have shown steady momentum across 1 month, 3 month and 6 month periods. Forecast valuation multiples remain reasonable for a large cap miner, with a forward price to earnings ratio of 13.5 and a dividend yield close to 4%. Operationally the group remains highly geared to movements in copper, iron ore and metallurgical coal.

REGENCY VIEW: Higher copper prices always give BHP an extra gear and this week’s record highs strengthen that link. With the dollar softening and supply signals tightening, BHP remains well positioned for any continuation in the commodity cycle.

Trustpilot shares fell sharply this week after short seller Grizzly Research disclosed a short position in the online review platform. The accompanying report accused the company of operating what it described as an “extortion model”, claiming Trustpilot creates unsolicited profiles for businesses that attract negative reviews and then encourages those businesses to buy subscription packages to manage the feedback. The allegations also pointed to differences in review scores between paying and non paying companies.

The report highlighted concerns around the quality and authenticity of reviews on the platform. Grizzly Research said it had found examples of negative reviews being challenged or removed for paying clients, while non paying businesses were more likely to accumulate critical feedback. It also claimed that some high scoring companies on the platform included businesses that had already ceased trading or had faced regulatory issues. Trustpilot has not yet issued a detailed response to address the specific claims.

The market reaction was immediate. The shares dropped more than 18% and trading volumes moved well above recent averages. Trustpilot already faced valuation headwinds, with a forward price to earnings ratio of 47.4 and a price to sales multiple of 4.34. Momentum has been weak for some time, with the stock down 44.8% over 1 year and sitting more than 47% below its 52 week high.

REGENCY VIEW: Allegations from short sellers tend to be emotive, so investors will be looking closely at Trustpilot’s response. Until the company provides clarity and hard data to counter the claims, the market will likely remain cautious.

Sector Snapshot

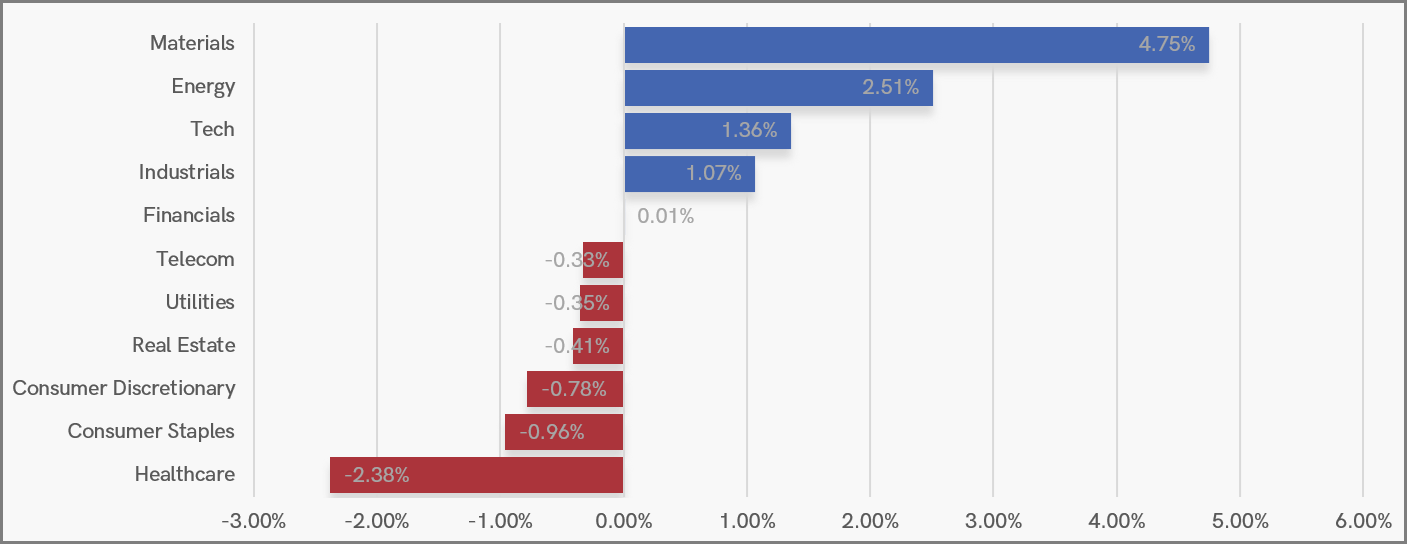

Materials led the market this week, supported by stronger commodity prices and improving sentiment across resource-linked names. Energy and Tech also performed well, with Industrials adding modest gains, hinting at a mild rotation back toward cyclical and growth-oriented sectors.

At the lower end, Healthcare extended its recent weakness, joined by Consumer Staples and Consumer Discretionary in negative territory. Real Estate, Utilities and Telecom also edged lower, suggesting investors were more comfortable leaning into cyclical momentum than seeking defensive cover.

UK Sector Performance (7-Days)

UK Price Action

It has been a quieter week for the FTSE as prices have settled into a tight consolidation just above the 50 day moving average. This pause comes after the sharp rebound from the late November lows and shows the market catching its breath rather than rushing into a fresh leg higher.

The longer term trend structure remains bullish, but the recent recovery has lacked the same punch seen during previous upside breaks. Until price can break convincingly out of this short term range, traders should be prepared for either scenario, with the 9,578 area acting as key near term support and last week’s highs marking the immediate barrier to further progress.

FTSE 100 Rolling Futures (Daily Candle Chart)

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.