4th Jul 2025. 10.51am

Weekly Briefing – Friday 4th July

| Market | Movement this week (%)* |

|---|---|

| FTSE 100 | -0.04% |

| FTSE 250 | -0.77% |

| FTSE All-Share | -0.12% |

| AIM 100 | +1.07% |

| AIM All-Share | +0.92% |

* Price movement from Monday's open at 8am

Regency View:

Weekly Briefing – Friday 4th July

Market Overview

Dear Investor,

The AI revolution has come back into focus this week with Nvidia’s share price breaking out and holding at highs recently. After a few months of uncertainty, the company has reasserted itself at the heart of the AI trade, proving once again why it’s seen as the engine behind this global megatrend.

Earlier in the year, there was a clear wobble. Geopolitical tensions, concerns around export restrictions, and fears of competition from China’s DeepSeek all conspired to knock Nvidia’s share price lower. But the market has a short memory when the growth story is this strong. Investors were given a fresh dose of optimism as Nvidia delivered another earnings beat, while CEO Jensen Huang laid out a vision that extends well beyond the next quarter. The AI infrastructure build-out is not slowing down. If anything, it is accelerating.

From a UK perspective, it’s a timely reminder of how global market leadership can influence sentiment everywhere. While we might not have a domestic giant at Nvidia’s scale, the enthusiasm for AI is spilling across borders, shaping investor attitudes and capital flows alike. UK investors are right to look outward. Opportunities in this space are not constrained by geography, and the trends driving demand for AI compute are as relevant in London as they are in Silicon Valley.

As always, the path forward won’t be without dips. But when the fundamentals are firing, sentiment is recovering, and technicals are pointing higher, it creates a powerful mix. Nvidia’s breakout is more than just a chart pattern. It is a signal that the AI narrative still has legs, and for investors watching from the UK, it’s a cue to stay engaged with the bigger picture.

Wishing you a fantastic weekend,

Tom

Thomas Light – Chartered FCSI

Director of Research

Market Movers

On the rise: Carnival (LSE:CCL) +8.9% on the week

Cruise ship operator Carnival have continued their strong recent run following an impressive Q2 trading update published at the end of June, with investors responding positively to record revenues, rising profitability and another upgrade to full-year guidance.

Net income reached 565 million dollars, up nearly 475 million year-on-year, while adjusted net income more than tripled and beat expectations by 185 million. Carnival also posted record operating income and the highest adjusted EBITDA margins in years, helped by strong close-in demand and exceptional onboard spending.

The company’s performance was so strong it hit its 2026 SEA Change financial targets 18 months ahead of schedule, including a more than doubling of adjusted return on invested capital to over 12.5 percent. Customer deposits hit an all-time high of 8.5 billion dollars and the forward booking curve remains the longest on record, with 2026 bookings already in line with 2025’s record levels. Pricing power remains robust too, with net yields up 6.4 percent compared to last year and gross margin yields more than 25 percent higher.

The full-year outlook has been raised again, with adjusted net income now expected to grow over 40 percent compared to 2024 and adjusted EBITDA forecast to reach nearly 6.9 billion dollars. Carnival has also increased its revolving credit capacity by 50%, giving it more financial flexibility heading into the back half of the year. With record-breaking numbers across the board and strong momentum heading into 2026, the business is sailing on calm waters despite wider macroeconomic chop.

REGENCY VIEW:

Carnival’s financials are cruising in the right direction, with strong momentum, improving profitability, and a forward PE of just 12.6 supporting the rally. It’s not cheap on a book value basis, but with earnings growth forecast above 20% and multiple momentum and quality screens lighting up, the stock still looks well positioned for smooth sailing into 2026.

Mpac’s share price gapped significantly lower on Tuesday following a trading update that revealed a sharp slowdown in order intake during the second quarter, driven by tariff uncertainty and falling consumer confidence in the US.

The slowdown, particularly acute in the Group’s core Original Equipment business, means full-year revenue is now expected to fall well short of previous expectations, with the closing order book down to around £90 million from £118.5 million at the end of last year. Mpac, which designs and builds high-speed packaging and automation solutions for global consumer goods manufacturers, had enjoyed a resilient start to the year, supported by strong service revenues and solid performances from its 2024 acquisitions.

Meanwhile, cash has come under pressure due to the slowdown in customer deposits, with net debt creeping slightly higher versus December. Management has responded with tighter financial controls, a clampdown on discretionary spending, and renegotiation of supplier terms. A buy-in transaction for the UK defined benefit pension scheme, announced alongside the update, is expected to simplify the balance sheet and eliminate a key source of future volatility. Despite near-term headwinds, Mpac remains confident that the actions being taken now will position it well when customer confidence returns.

REGENCY VIEW:

Mpac’s latest numbers show a company under pressure but not out for the count. Revenue ticked up yet slim operating margins and rising net debt are weighing on profitability. The share price momentum is weak, mirroring investor nerves. That said, the valuation looks reasonable and cash reserves offer some breathing room.

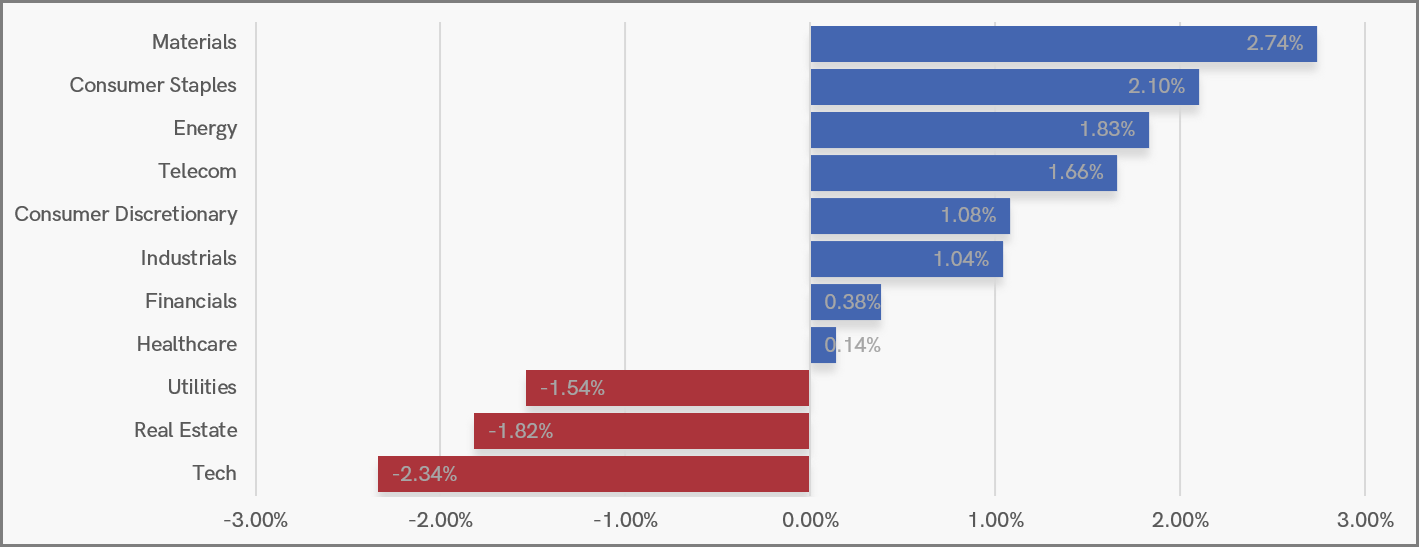

Sector Snapshot

This is a seven day snapshot during which the UK market edged higher, with gains led by Materials, Consumer Staples, and Energy. Strength in commodity names and stable demand for essentials helped drive the rally, while Telecoms and Consumer Discretionary also chipped in with modest gains.

In contrast, Tech took a breather after recent outperformance, slipping to the bottom of the leaderboard alongside Real Estate and Utilities. The rotation suggests investors are leaning back into value and defensives with earnings visibility, while trimming exposure to interest rate-sensitive growth names.

UK Sector Performance (7 Days)

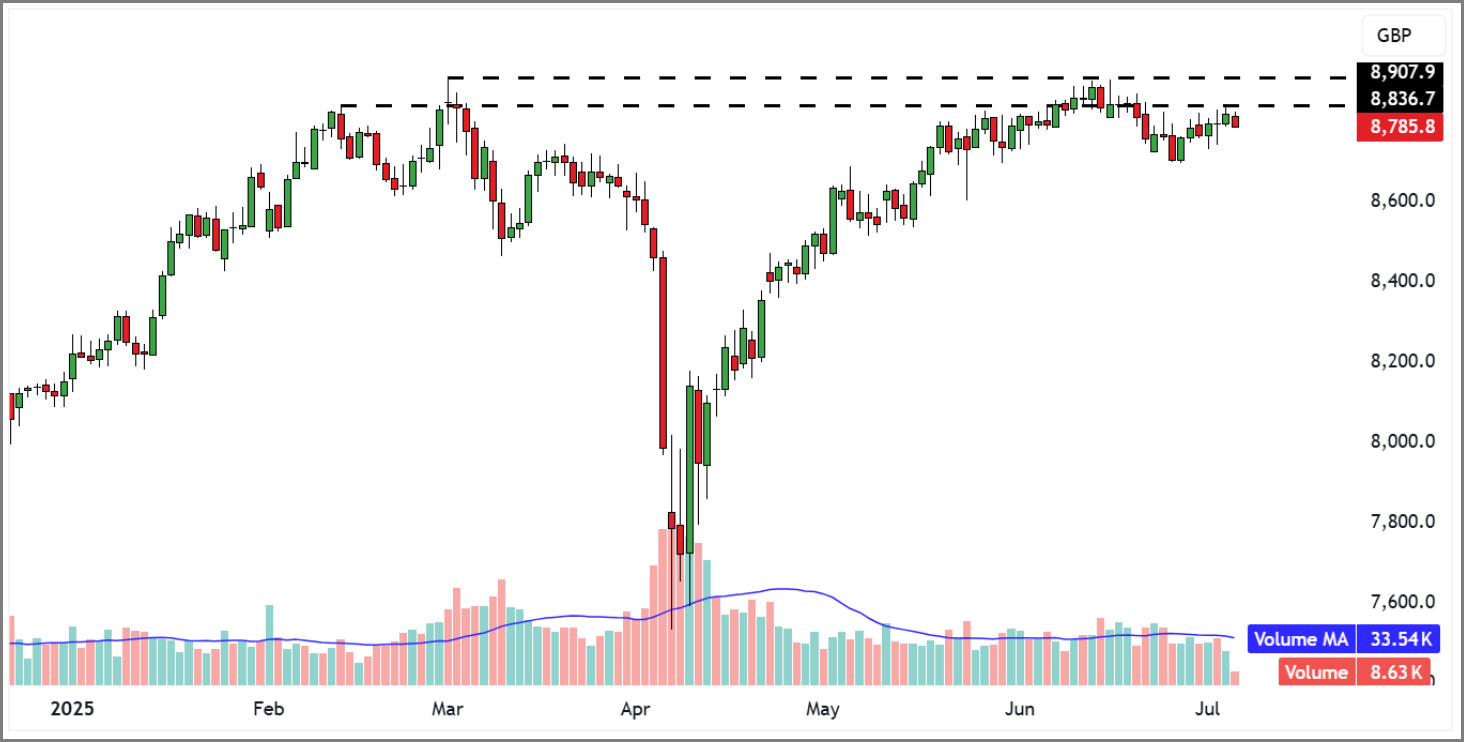

UK Price Action

With Wimbledon in full swing and the F1 Grand Prix on the horizon, it’s no surprise to see the FTSE drifting sideways on light summer volumes. The index continues to coil just below key resistance, consolidating its recent gains while traders wait for a catalyst. Whether it can follow the lead of US markets and punch through to new highs remains the big question.

FTSE 100 Rolling Futures (Daily Candle Chart)

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.