4th Apr 2025. 10.08am

Weekly Briefing – Friday 4th April

| Market | Movement this week (%)* |

|---|---|

| FTSE 100 | -3.46% |

| FTSE 250 | -4.26% |

| FTSE All-Share | -3.60% |

| AIM 100 | -5.29% |

| AIM All-Share | -4.94% |

* Price movement from Monday's open at 8am

Regency View:

Weekly Briefing – Friday 4th April

Market Overview

Dear Investor,

This week saw the culmination of weeks of Trump’s tariff news. Donald dubbed it “liberation day”—a bold claim considering the sweeping nature of the new tariffs. In his words, it’s all about “taking care of our people first” and fighting back against what he sees as decades of economic surrender. From where we’re sitting in the UK, though, it feels less like a bold step forward and more like a leap into uncertainty.

It remains to be seen whether these tariffs will drive inflation, choke growth, or even tip the US into recession. But one thing is clear: this lack of stability is bad news for investment. Setting up factories, altering component lists, and finding new suppliers—these things take time, money, and a stable trade environment. When tariffs seem to be switched on and off at a whim, how can businesses plan ahead? In the UK, where many manufacturers rely on complex global supply chains, that’s a serious concern.

The most glaring example is the UK’s own position in this tariff landscape. Despite being a close ally of the US, we’re still facing a 10% tariff on our exports. That stings, particularly when you consider the effort put into maintaining strong transatlantic ties post-Brexit. With Europe facing tariffs as high as 20% and Japan 24%, it’s clear the US isn’t playing favourites. For UK exporters, this could mean higher costs that are tough to pass on to customers already squeezed by rising inflation.

The harshest hit by Trump’s tariffs is China, which now faces a staggering 54% on its exports to the US. Beijing has promised to retaliate, as have the EU and other affected countries. The problem is that these tit-for-tat moves rarely end well. As one strategist put it, “Retaliation day will follow liberation day.”

Closer to home, the impact on UK markets could be indirect but significant. If global trade volumes dip, the UK’s export-reliant sectors—like manufacturing and automotive—could feel the pinch. Companies that rely on smooth transatlantic trade may find themselves squeezed between higher costs and reluctant customers.

Ironically, amid the tension, some countries are finding a silver lining. Mexico and Canada, for example, have been spared the worst of the tariffs, thanks to their trade deal with the US. Mexico, in particular, could benefit as companies look to shift production to dodge US tariffs on other regions.

As the dust settles, one thing is becoming clear: Trump’s push for protectionism has turned the global trade order on its head. We may not know yet whether this will lead to recession or inflation, but the unpredictability itself is likely to be the biggest challenge.

Wishing you a fantastic weekend,

Tom

Thomas Light – Chartered FCSI

Director of Research

Market Movers

On the rise: Currys (LSE:CURY) +14.1% on the week

Currys’ share price jumped higher on Thursday following an upbeat trading update and raised guidance for the current financial year. The UK-based electricals retailer reported that trading has remained robust since the start of January, with positive like-for-like sales growth across both the UK & Ireland and the Nordics. As a result, Currys has increased its profit expectations for the year, now anticipating an adjusted profit before tax of around £160 million. This is a notable upgrade from its previous guidance of £145-155 million, reflecting stronger-than-expected performance as the financial year draws to a close.

Investors reacted positively to the news, with Currys’ shares rising as much as 10.2% to 98.05p, making it the top gainer on the FTSE mid-cap index. The company also announced that it expects to finish the year in a strong net cash position, underlining its improved financial health. In contrast to the broader retail sector, where stocks like Tesco and Sainsbury gained more modestly by around 1.1% to 1.4%, Currys’ significant rise signals renewed investor confidence driven by the upgraded outlook.

The final trading update for the 53 weeks ending 3 May 2025 is scheduled for 21 May, and the market will be closely watching for confirmation of the improved profit figures. Currys’ ability to increase guidance at a time when other retailers are still navigating a challenging economic environment highlights the company’s operational resilience. After a year that saw the stock fall by approximately 6.3%, Thursday’s surge represents a welcome boost, driven by signs that Currys is weathering the current retail landscape more effectively than some of its peers.

REGENCY VIEW:

Currys is showing strong momentum with a positive outlook for the current financial year, having raised its profit guidance to £160 million, up from previous estimates. The group’s solid revenue performance, combined with a strong cash position, suggests stability in a challenging retail environment, positioning it well as it heads towards the year-end.

Burberry’s share price has taken a significant hit this week, contributing to a more than 40% decline from its highs in February. This downturn is largely due to growing concerns over U.S. President Trump’s new tariffs, which include a 20% rate on European Union goods and a 31% tariff on Swiss products, both of which are major markets for luxury brands like Burberry. These new duties are sparking fears that the luxury sector could face rising inflation, further delaying any potential interest rate cuts, which were previously hoped to provide some relief.

Additionally, analysts have expressed concern about the broader economic outlook for 2025, particularly in relation to luxury goods exports. The luxury sector, which is highly reliant on the Chinese market, is already seeing worrying signs, with a notable 8.4% decline in imports to China in the early part of the year. This, coupled with the weakening of the U.S. dollar and the strengthening of the euro, creates a tough environment for European luxury brands. The sector’s vulnerability to currency fluctuations, especially given that production is based in Europe while sales are predominantly in USD-related currencies, adds further pressure.

Burberry, alongside other luxury brands, is also grappling with the broader impact of these tariff changes, especially in light of the expected hit to margins for companies like Richemont and Swatch Group, which have already been operating on thin margins. While Burberry’s diversified offerings and strong brand equity have provided resilience in the past, the combination of trade tensions, inflation fears, and a challenging global economic landscape is creating significant headwinds, reflected in its weakened stock performance.

REGENCY VIEW:

Burberry’s brand faces challenges, including declining revenue and rising costs, alongside macroeconomic concerns, such as US tariffs and a slowdown in China—key markets for luxury goods. While Burberry’s stock has suffered, its valuation remains relatively high, with a P/E ratio of 30.7, which suggests a market still weighing the potential for recovery despite current pressures.

Sector Snapshot

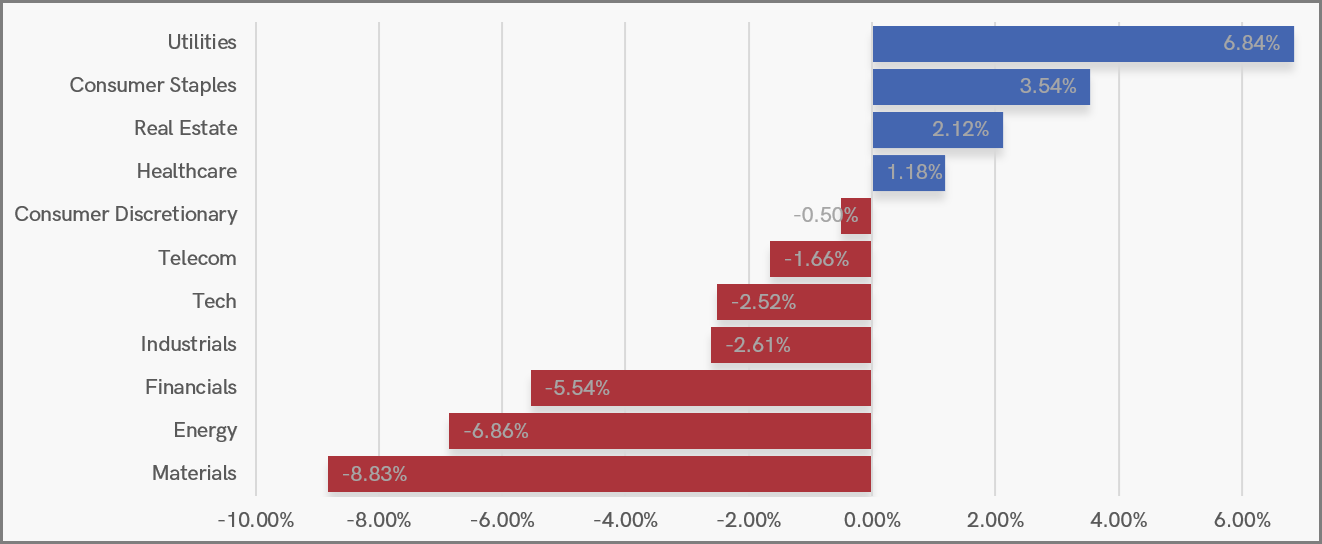

Trump’s ‘Liberation Day’ tariffs have drawn a clear line between the winners and losers in the UK markets. Defensive sectors have come out on top, with Utilities leading the charge, followed by Consumer Staples. As investors seek safety amid economic uncertainty, these traditionally resilient areas are seeing renewed interest.

On the flip side, cyclical sectors have taken a hit, with Materials, Energy, and Financials bearing the brunt of the sell-off. Concerns over global growth and the impact of higher tariffs on industrial output and energy demand have left these sectors particularly vulnerable. As sentiment shifts towards caution, investors are rotating away from economically sensitive stocks.

UK Sector Performance (YTD)

UK Price Action

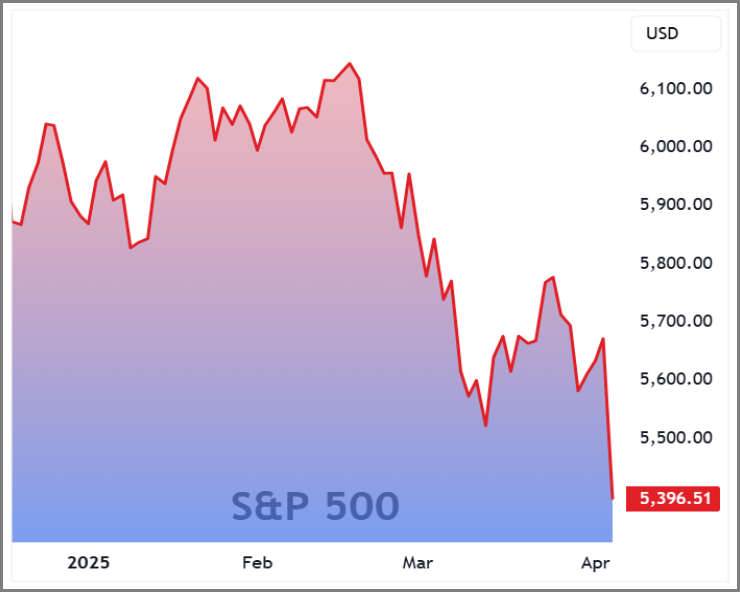

In last week’s UK Price Action we mentioned that the “intensifying period of price compression signals that we may be gearing up for a decisive directional move soon”. The decisive directional move came to the downside and the index has almost erased all of the gains it made earlier in the year.

The FTSE is now pressing down into a key support zone which comprises of broken resistance turned support and the 200 day moving average.

FTSE 100 Rolling Futures (Daily Candle Chart)

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.