3rd Oct 2025. 10.51am

Weekly Briefing – Friday 3rd October

| Market | Movement this week (%)* |

|---|---|

| FTSE 100 | +2.16% |

| FTSE 250 | +2.43% |

| FTSE All-Share | +2.18% |

| AIM 100 | +2.01% |

| AIM All-Share | +1.60% |

* Price movement from Monday's open at 8am

Regency View:

Weekly Briefing – Friday 3rd October

Market Overview

Dear Investor,

The FTSE 100 surged to fresh highs this week, extending a rally that has been firmly in place since mid-April. The heavyweights in healthcare were the main drivers once again, with AstraZeneca, GSK and Hikma all climbing after sentiment improved around US drug pricing. A deal struck by Pfizer with the US administration eased concerns about tougher regulation, and given the scale of pharma within the FTSE, the move was more than enough to push the index higher.

Global conditions added further fuel. Anticipation is building into today’s US jobs data, with investors increasingly convinced that the Federal Reserve’s September rate cut will not be a one and done scenario. Hopes of a more sustained easing cycle have lifted equities across the board, while the political noise of a US government shutdown has nudged capital towards London’s internationally diversified blue chips. Against that backdrop, the FTSE has remained an attractive destination for global flows.

At home, the picture has been supportive as well. September house prices ticked higher, hardly the sign of a roaring economy but a welcome counterweight to some of the gloom hanging over UK property. This fed into a stronger showing for banks and consumer names, giving the rally more breadth than simply leaning on pharma alone. It shows how even small positives can be enough to keep the buying pressure alive when momentum is already strong.

That said, investors should not get too carried away. The FTSE now trades on a price to earnings ratio of 19.9 times, above its three year average of 15.9 times. Valuations are no longer cheap, and the discipline of taking profits into strength and keeping a firm eye on quality becomes all the more important. Our FTSE Investor service has been doing just that, banking several triple digit profits during this rally and keeping subscribers focused on the right opportunities. If you missed last week’s note, we have also moved to monthly subscriptions, making it more flexible than ever to follow our recommendations and research.

Wishing you a fantastic weekend,

Tom

Thomas Light – Chartered FCSI

Director of Research

Market Movers

On the rise: CRH (LSE:CRH) +7.5% on the week

CRH’s share price gapped higher this week following its investor day update, where the company laid out a new five-year growth plan. Shares rose nearly 6% in premarket trading to around $121.70 after management reaffirmed 2025 guidance, which includes adjusted EBITDA in the range of $7.5 to $7.7 billion. The construction materials group also presented long-term ambitions, highlighting an adjusted EBITDA margin target of between 22% and 24% by 2030, compared with its current levels.

Alongside its margin goals, CRH set financial targets for average annual revenue growth of 7% to 9% between 2026 and 2030. These objectives were positioned as part of the company’s next era of growth, aiming to build on its strong performance through both organic initiatives and operational improvements. The announcement reinforced CRH’s strategy of scaling its global presence in construction solutions while delivering stronger returns across its core operations.

Market reaction reflected the renewed confidence in the company’s trajectory. As of the latest close, CRH shares were up around 24% year-to-date, with momentum boosted by the latest update. Data from LSEG showed that 20 of 24 brokerages currently rate the stock as a “buy” or higher, with the remaining four assigning a “hold” rating. The median price target stands at $124, broadly in line with the trading levels reached in the wake of the announcement.

REGENCY VIEW:

CRH stands out as a high-quality large cap with strong earnings growth forecasts, solid returns on capital, and momentum firmly on its side. Valuation looks a little stretched on metrics like price to free cash flow and EV/EBITDA, but with double-digit EPS growth projected and a healthy balance of revenue scale and profitability, it remains a heavyweight in the basic materials sector.

Flutter Entertainment’s shares came under heavy pressure this week, snapping two straight days of gains with a 10% drop in New York on Tuesday. The fall followed the launch of a new sports-betting product from US exchange Kalshi. Its “build your own combo” parlay feature allows users to link multiple contracts on a single game, drawing comparisons with FanDuel’s existing offering. The product was unveiled ahead of Monday night’s NFL fixtures, with 90% of Kalshi’s betting volume already tied to sports contracts.

Despite the market reaction, Flutter maintained support from analysts, with Benchmark reiterating its “buy” recommendation and a $365 price target. The broker pointed to the strength of FanDuel’s performance during the third week of the NFL season, suggesting the group remains in a strong competitive position in its core US market. The price target implies an upside of more than 40% from the stock’s latest close.

In the UK, political developments added to investor unease. At the Labour Party conference, the Chancellor said that betting companies should “pay their fair share of taxes”, fuelling speculation that the upcoming November Budget could include higher levies on the sector. With shares already sensitive to regulatory risk, the prospect of additional taxes weighed further on sentiment, keeping the sector under pressure.

REGENCY VIEW:

Flutter shows strong earnings momentum with forecast EPS growth above 70%, though current multiples leave it trading at a premium. Solid quality scores and resilient revenues keep the business well supported despite the richer valuation backdrop.

Sector Snapshot

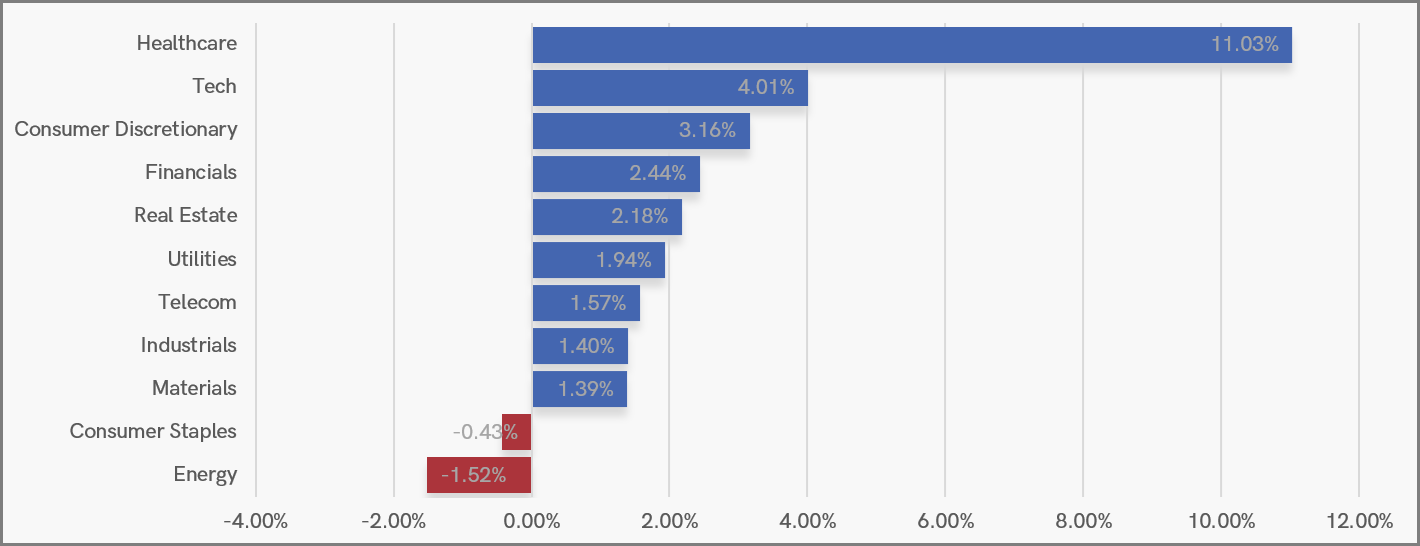

Healthcare dominated the leaderboard this week with double-digit gains, far outpacing the rest of the market and driving a decisive shift in sector leadership. Tech and Consumer Discretionary also delivered strong performances, while Financials and Real Estate added to the upbeat tone, showing that investors were willing to back both growth and cyclicals.

Utilities, Telecom, Industrials and Materials all posted steady gains, leaving the overall picture broadly positive. The only notable weakness came from Consumer Staples and Energy, which slipped into the red, underscoring a rotation away from defensives and commodities in favour of higher-growth and earnings-led sectors.

UK Sector Performance (7-Days)

UK Price Action

The FTSE has broken decisively higher from the bullish consolidation pattern we have been tracking over the past few weeks. This breakout confirms that the uptrend remains intact, with momentum carrying price into fresh territory above the September range.

The zone around 9,350–9,360, which capped rallies throughout late summer, should now act as support on any pullback. For traders who missed the initial breakout, this area could offer a second-chance entry to align with the trend, provided buyers step in to defend it.

FTSE 100 Rolling Futures (Daily Candle Chart)

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.