30th May 2025. 9.47am

Weekly Briefing – Friday 30th May

| Market | Movement this week (%)* |

|---|---|

| FTSE 100 | +0.39% |

| FTSE 250 | +1.46% |

| FTSE All-Share | +0.53% |

| AIM 100 | +1.26% |

| AIM All-Share | +1.21% |

* Price movement from Monday's open at 8am

Regency View:

Weekly Briefing – Friday 30th May

Market Overview

Dear Investor,

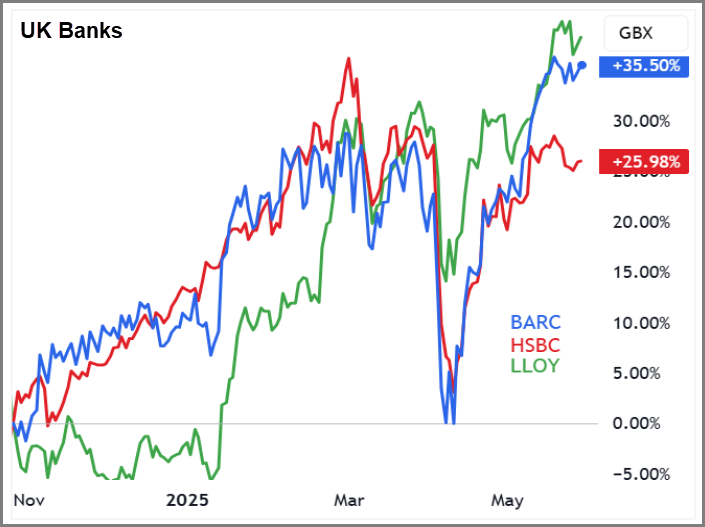

This week we are turning the spotlight on the FTSE’s standout sector. Financials may not grab the headlines, but they have quietly become the best-performing part of the UK market over one year, three years and five. Dominated by the banking giants, this sector has delivered the strongest total return across multiple timeframes. While others were distracted by the rise and fall of tech or commodity swings, financials kept climbing with quiet consistency.

So what has been driving this performance? Yes, higher interest rates have helped, but this is more than a yield story. Over the past decade, UK banks have rebuilt their balance sheets, stripped out costs and focused on capital discipline. They are now better capitalised than at any point in a generation and have become efficient cash-generating machines. The result is a sector that combines value with stability, and plenty of shareholder returns along the way.

The big three names in the sector are all showing signs of strength. Barclays has broken above long-standing resistance following a well-received investor update and a commitment to return £10 billion to shareholders. HSBC continues to benefit from its pivot to Asia and improving capital efficiency, with clearer guidance and higher returns in focus. Lloyds remains a more domestic story but has been steadily executing on margin management and capital return, with the share price quietly grinding higher in line with a more confident UK consumer backdrop.

The momentum in these names reflects a broader investor shift. For years, UK banks were seen as value traps, weighed down by regulation and low growth. But today, that narrative is changing. They are leaner, more focused and far more willing to return excess capital. Crucially, they are also starting to re-rate from very low multiples, offering both income and growth for those prepared to look past the old baggage.

Our FTSE Investor clients have been well-positioned throughout this theme. We took profits on Barclays in December following a strong run, while holding two tranches of HSBC as the turnaround began to build momentum. And with Barclays now staging a convincing breakout above its long-term ceiling, we stepped back in this week to ride the next leg higher.

Wishing you a fantastic weekend,

Tom

Thomas Light – Chartered FCSI

Director of Research

Market Movers

On the rise: Qinetiq (LSE:QQ.) +4.9% on the week

Qinetiq’s share price has continued to rally following last week’s impressive preliminary results, with fresh momentum coming from the announcement of a £1.54 billion extension to its Long Term Partnering Agreement. The five-year deal with the UK Ministry of Defence significantly boosts the company’s already strong order backlog, now standing at approximately £5 billion. Despite a tougher trading environment in the final quarter, Qinetiq ended the year with record order intake of nearly £2 billion, up 12% on the previous year, underlining the strength of demand for its defence and security capabilities.

Management acknowledged a challenging end to the year, particularly within the UK Intelligence and US divisions, where performance was impacted by geopolitical uncertainty and delays to short-cycle contracts. The group has responded with a clear restructuring plan aimed at streamlining operations and aligning more closely with the evolving needs of NATO and allied forces. Although statutory profits were hit by one-off charges linked to US legacy operations and restructuring costs, the underlying business remains resilient, with revenue up 2% on an organic basis and cash generation continuing to impress. Leverage has been reduced to just 0.4 times, highlighting the financial strength of the balance sheet.

Looking ahead, Qinetiq expects revenue growth of around 3% in the year to March 2026 and a sharp rebound in earnings per share of 15 to 20 percent as the benefits of the restructuring begin to come through. The company has also reinforced its commitment to shareholder returns, completing £103 million of its £150 million buyback during the year and preparing to launch a further £200 million programme from June. With sector sentiment supported by easing trade tensions between the US and EU, and defence indices pushing to record highs, Qinetiq looks well placed to capture further upside as it reshapes for long-term growth.

REGENCY VIEW:

Qinetiq’s recent surge reflects strong order momentum and upbeat EPS forecasts, but with a weak quality score and pricey cashflow multiples, it’s more of a momentum trade than a value play. The restructuring narrative is gaining traction, yet the fundamentals still need to catch up to justify a sustained re-rating.

Auto Trader’s share price dropped sharply this week following the release of its full-year results, despite delivering record revenues and solid profit growth. Investors appear to have focused on slowing momentum in the company’s Retailer segment, where a faster-than-expected speed of sale has limited the revenue uplift from its slot-based advertising model. Although core Auto Trader revenue rose 7% to £565 million and group operating profit climbed 8%, a soft outlook for retailer revenue growth in the first half of the new financial year may have prompted some caution. The impact of the UK’s Digital Services Tax, which took £10.2 million off the bottom line for the first time, may also have contributed to the market’s reaction.

Management remains upbeat, highlighting continued dominance in its category with over ten times the audience of its nearest competitor. A key focus has been the rollout of its AI-powered Co-Driver platform and the ongoing expansion of Deal Builder, now embedded into its core offering. Both initiatives are aimed at streamlining the car-buying process and improving retailer efficiency. Auto Trader also pointed to record engagement levels, with cross-platform visits climbing to 81.6 million per month and more than three-quarters of all minutes spent on UK car marketplaces taking place on its site.

Looking ahead, Auto Trader expects retailer revenue growth to pick up to between 5% and 7% over the course of FY26, supported by improved pricing power and stronger product uptake. While the drag from declining used car stock levels is expected to persist, management anticipates this will be offset by better performance from prominence products and improved contribution from new pricing modules. The group also expects reduced losses from Autorama and a lift in overall operating margins. Although the immediate market reaction was negative, Auto Trader’s strong competitive position, consistent cash generation and focus on tech-led growth continue to underpin its long-term appeal.

REGENCY VIEW:

Auto Trader is a high-quality, high-margin business that continues to grow earnings at a healthy clip, but the valuation is looking stretched with a forward PE near 25 and limited free cash flow yield. The recent drop may cool off short-term sentiment, yet the long-term uptrend remains firmly intact.

Sector Snapshot

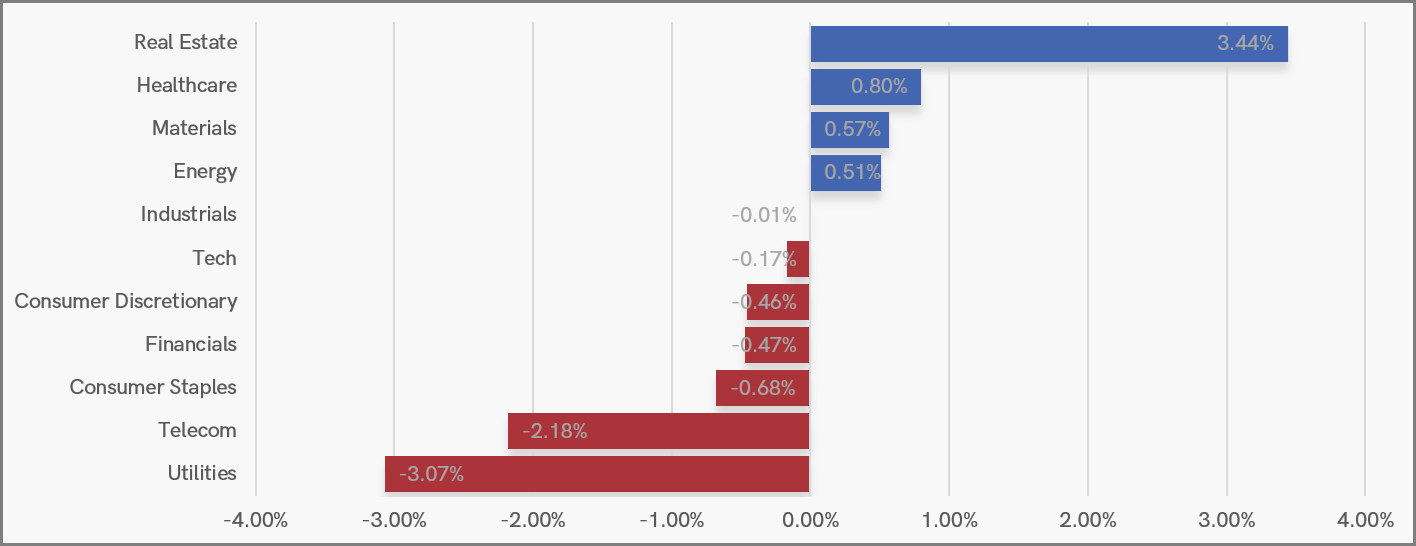

Real Estate led the charge this week, comfortably outpacing all other sectors and extending its run of relative strength. Healthcare and Materials also found support, helped by a modest risk-on tilt and signs of selective buying across cyclical names.

In contrast, traditional defensives came under pressure. Utilities and Telecoms were firmly at the bottom of the pile, with Consumer Staples not far behind. The divergence hints at a market reassessing its safe havens, favouring income-producing assets with growth optionality over pure defensiveness.

UK Sector Performance (YTD)

UK Price Action

The FTSE has paused just below the key resistance zone we flagged last week, around the highs from February and March. So far there’s been no sharp rejection, and price action still looks like a sideways consolidation within the broader uptrend.

FTSE 100 Rolling Futures (Daily Candle Chart)

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.