29th Aug 2025. 11.34am

Weekly Briefing – Friday 29th August

| Market | Movement this week (%)* |

|---|---|

| FTSE 100 | -1.32% |

| FTSE 250 | -0.90% |

| FTSE All-Share | -1.26% |

| AIM 100 | -0.16% |

| AIM All-Share | +0.32% |

* Price movement from Monday's open at 8am

Regency View:

Weekly Briefing – Friday 29th August

Market Overview

Dear Investor,

This week has been dominated by earnings from the world’s most expensive company, Nvidia. The AI poster child once again delivered results that most businesses could only dream of, with revenue up 56% year on year and net income jumping close to 60%. Management guided above expectations for the current quarter, though they chose to leave China chip sales out of the forecast while export rules are still being clarified. Despite that note of caution, the market reaction was measured. Nvidia’s shares remain comfortably within their recent trading range and sit less than 3% from all-time highs.

For investors, the debate was never about whether Nvidia could post another set of stellar numbers. The real interest lay in how management would frame the future. China remains the obvious swing factor, with a licensing deal for the H20 chip yet to be codified. The company suggested shipments of two to five billion dollars could flow if approvals are secured, but for now they have kept guidance clean of those revenues. From a UK perspective, that conservatism is probably no bad thing, removing some of the political noise from what is otherwise a robust growth story.

Outside China, demand remains exceptional. Data centre sales now account for nearly 90% of revenue, and the latest generation Blackwell Ultra chips are already ramping into production. Jensen Huang struck a typically bullish tone, pointing to a global AI race that is still only just getting started. The big hyperscalers have doubled capital spending to around six hundred billion dollars a year, and governments from Europe to the Middle East are rolling out sovereign AI programmes. The scale of future demand is hard to ignore.

Valuation is of course stretched, with Nvidia trading at more than thirty times sales and close to forty times forward earnings. That leaves little room for error, but the company’s track record of execution continues to reassure the market. A new sixty billion dollar buyback adds another layer of support, and with free cash flow generation running at extraordinary levels, few companies can match its financial firepower. For UK investors watching from afar, Nvidia remains a defining stock of the cycle, even if portfolio discipline is essential at these heights.

What matters for the broader market is that Nvidia’s results helped steady the ship at a sensitive moment. The S&P 500 pushed to fresh record highs this week, underlining how central AI has become to sentiment. For all the debate about valuation and policy risk, the structural tailwind remains firmly in place. Nvidia’s update may not have been explosive, but it did enough to keep the market narrative intact.

Wishing you a fantastic weekend,

Tom

Thomas Light – Chartered FCSI

Director of Research

Market Movers

On the rise: Empire Metals (AIM:EEE) + 39.7% on the week

Shares in AIM-listed miner Empire Metals have been surging higher in recent weeks following a drilling update on 18th August at its Pitfield titanium project in Western Australia. The company announced outstanding assay results from the Thomas prospect, including multiple intercepts above 6% titanium dioxide across a 3.6 kilometre strike length. Nearly two thirds of drillholes averaged more than 4% titanium dioxide, with over 90% exceeding a 2% cut-off grade.

The drilling campaign, which comprised 382 holes for more than 32,000 metres, confirmed the presence of a large, high-grade central core averaging around 6% titanium dioxide. Empire said the continuity of mineralisation near surface would underpin its maiden JORC-compliant Mineral Resource Estimate and that assays had been received ahead of schedule, allowing resource modelling to proceed at pace.

Further news this week added to the momentum, with the company reporting a breakthrough in metallurgical testwork. Results showed Pitfield’s weathered ore could be processed using conventional methods, achieving recoveries of around 67% and producing a high-purity titanium dioxide product grading 99.25%. Empire said this confirmation of processing suitability provided a clear pathway toward commercial development.

REGENCY VIEW:

Empire Metals is still firmly in the exploration stage with no revenues on the books, which explains the stretched valuation ratios and low quality metrics. For now the whole story rests on Pitfield, where drilling and metallurgical work have pointed to a giant titanium system and a processing route capable of producing a high-purity product.

Shares in Park Plaza Hotels owner PPHE Hotel dropped sharply this week following the release of a disappointing set of interim results. The Group reported total revenue of £199.9 million for the six months ended 30 June 2025, representing an increase of 4.7% compared with the previous year. However, despite improved occupancy levels, margins remained under pressure as normalising room rates and higher social security costs weighed on profitability. Reported EBITDA fell by 5.7% to £45.5 million, while like-for-like EBITDA declined by 4.9%. Adjusted EPRA earnings per share also slipped, down 4.8% to 119 pence over the last 12 months compared with 125 pence at the end of 2024.

The company highlighted ongoing investment in its property portfolio, with recently opened hotels in London and Rome continuing to build momentum. Strategic activity included the acquisition of a development site near the City of London for £17.5 million, which is earmarked for the Group’s first Radisson RED hotel in the capital. Further expansion came through the purchase of 514,947 shares in its subsidiary Arena Hospitality Group for €18.5 million, taking its stake to 65.5%. Post balance sheet, the Group also acquired the freehold of its Park Royal hotel and adjoining development site in London for £10 million.

Looking ahead, PPHE reaffirmed its expectation that the new pipeline of recently opened properties will generate at least £25 million of incremental EBITDA once stabilised. However, the Group cautioned that short-term profitability will continue to be affected by lower contributions from art’otel London Hoxton, as its opening is being phased in line with long-term performance goals. The Board also noted potential cost headwinds in 2026 and beyond, including possible changes to VAT rates on hotels in the Netherlands and UK business rates.

REGENCY VIEW:

PPHE continues to grow its footprint with new openings in London and Rome alongside strategic acquisitions that expand its development pipeline. While revenues are rising, margin pressure from higher costs and phased hotel ramp-ups means the immediate focus remains on efficiency and stabilisation before the expected earnings uplift from new properties comes through.

Sector Snapshot

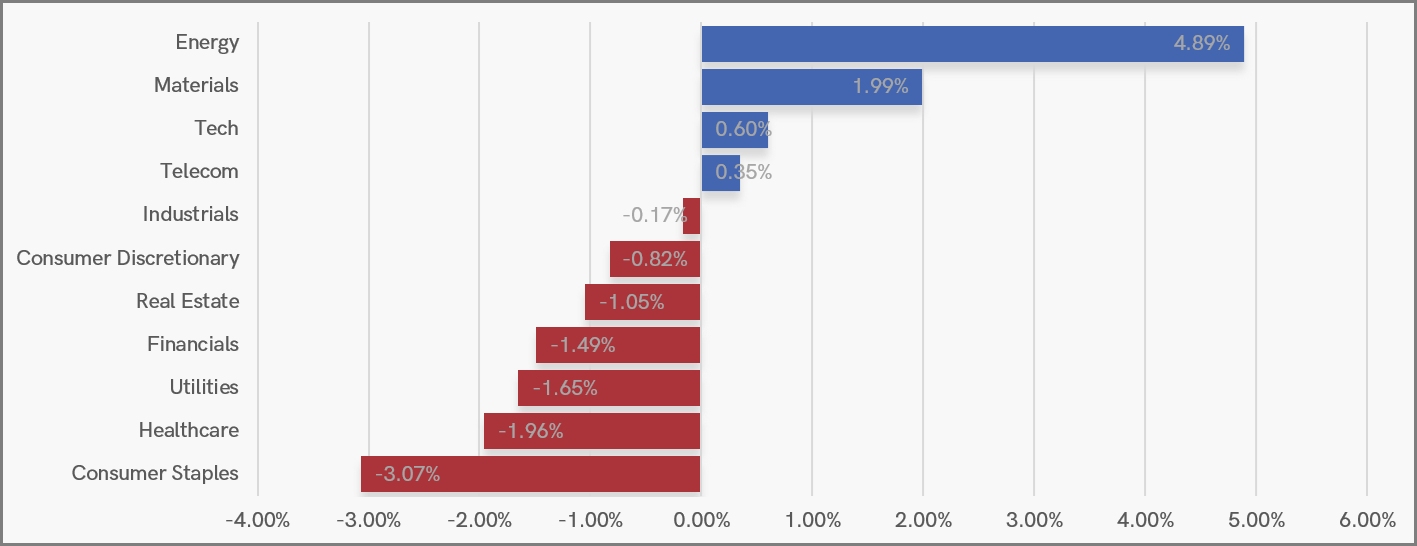

After finishing last week at the bottom of the pile, Energy staged a strong rebound to lead the market, with Materials also posting healthy gains. Tech and Telecom added modest support, leaving the leadership concentrated in cyclical and resource-linked sectors rather than the defensives that dominated previously.

On the flip side, Healthcare and Consumer Staples, which were last week’s stars, dropped to the weakest performers, joined by Utilities in negative territory. Financials and Real Estate also drifted lower, underscoring a clear rotation away from margin protecting defensives and back into areas more exposed to the economic cycle.

UK Sector Performance (7-Days)

UK Price Action

The FTSE’s breakout fizzled this week as the index gave back more than half of its recent gains. The pullback has been controlled, bringing prices back to the top of the old range where broken resistance will now be tested as support.

FTSE 100 Rolling Futures (Daily Candle Chart)

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.