27th Jun 2025. 10.45am

Weekly Briefing – Friday 27th June

| Market | Movement this week (%)* |

|---|---|

| FTSE 100 | +0.04% |

| FTSE 250 | +2.15% |

| FTSE All-Share | +0.32% |

| AIM 100 | +1.21% |

| AIM All-Share | +1.11% |

* Price movement from Monday's open at 8am

Regency View:

Weekly Briefing – Friday 27th June

Market Overview

Dear Investor,

This week has been dominated by moves in crude oil and crypto, with both markets telling very different stories. While crypto surged on a rare win out of Washington, crude oil has started to roll over as traders respond to signs that the conflict in the Middle East may be cooling off. One market is catching a tailwind from regulation, the other is losing its war premium, and the contrast couldn’t be clearer.

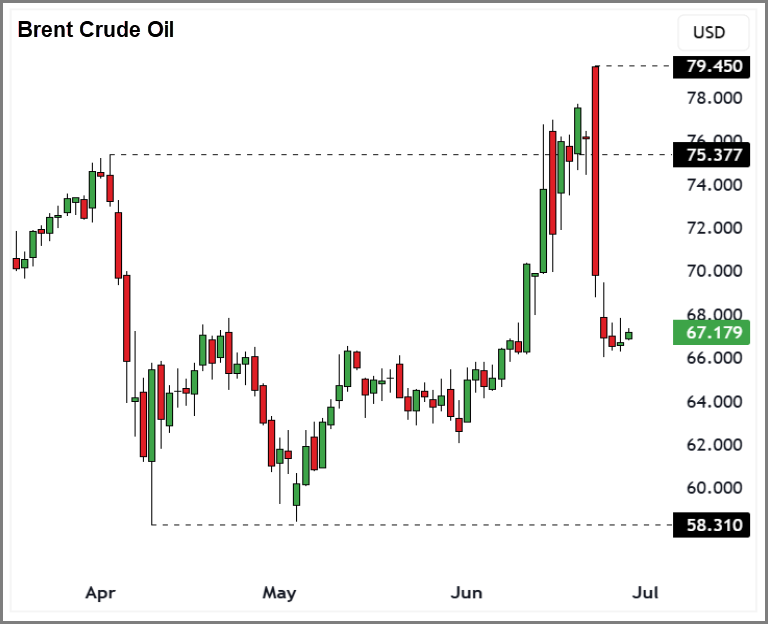

Crude oil looked unstoppable last week, surging into resistance as the US Iran situation escalated. Then came the twist. After gapping higher on Monday following reports that President Trump had authorised strikes on Iranian nuclear facilities, Brent reversed hard. Iran’s response, a missile attack on a US base in Qatar, landed with more of a political message than real escalation. Traders recognised the move as carefully choreographed, not a trigger for further conflict, and oil promptly gave back its gains. By the close, Brent had printed a bearish engulfing candle, a strong technical reversal signal, and the tone had flipped.

The market started drawing comparisons with early 2020, when US Iran tensions followed a similar arc. Threats, retaliation, and plenty of noise, followed by quiet de-escalation behind the scenes. Once again, it looks like the fear premium may have overshot. Brent’s failure to hold above resistance suggests the bulls are running out of reasons to stay aggressive, at least for now.

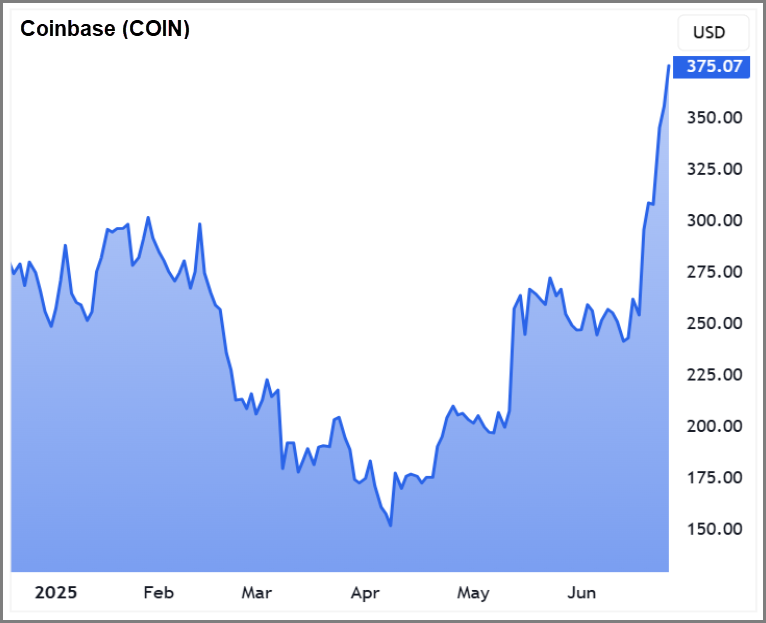

Meanwhile, over in crypto, the mood is very different. The US Senate passed the GENIUS Act, a landmark piece of legislation aimed at regulating stablecoins, and that has put a serious bid under names like Coinbase. The stock has surged more than 50% during the last two weeks as investors reacted to the prospect of regulatory clarity, full reserve backing requirements, and monthly audits for stablecoin issuers. Coinbase, which co-founded USDC and earns 50% of the reserve income, stands to benefit in a big way if this market becomes institutionally scalable.

So, what we are seeing here is a tale of two asset classes, one shedding risk premium, the other gaining legitimacy. Oil looks like it has run out of reasons to rally, while crypto, for once, is rallying on policy, not hype. For traders and investors alike, it is a reminder that the biggest moves often come when the narrative flips.

Wishing you a fantastic weekend,

Tom

Thomas Light – Chartered FCSI

Director of Research

Market Movers

On the rise: Dialight (LSE:DIA) +49.8% on the week

Shares in industrial LED lighting maker Dialight have surged higher this week following a return to profitability and a confident outlook from management in its full year results.

The company reported an underlying operating profit of 4.2 million dollars for the 12 months to 31 March 2025, compared to a 1.9 million dollar loss the previous year. Gross margins improved significantly to 35.6%, driven by tighter pricing discipline and cost savings. Revenue edged up to 183.5 million dollars, while underlying cash flow strengthened to 19.5 million dollars, helping to reinforce investor confidence in the turnaround.

Dialight, which provides rugged and energy efficient LED lighting for hazardous and industrial environments, also absorbed one off costs of 21.6 million dollars linked to its settlement with manufacturing partner Sanmina and its wider transformation plan. Although this pushed statutory losses deeper into the red, management made it clear that these legacy issues are now behind the business. With a leaner structure, improved commercial discipline and stronger internal engagement across teams, Dialight is starting to look more robust and better positioned for the challenges ahead.

Looking forward, the company noted a positive start to the new financial year and said it remains confident in delivering further progress. A new Strategy and Innovation Committee has been set up to explore technologies and applications that will drive future growth, signalling a shift in focus from recovery to expansion. While the global backdrop remains uncertain, particularly with regard to tariffs and component sourcing, Dialight’s operational momentum and clear medium term strategy appear to have won over investors.

REGENCY VIEW:

Dialight has caught fire in the short term, with the share price up more than 70% in a month as investors warm to its turnaround story. But with a forward PE pushing 130, no dividend, and margins still in the red, this is one for momentum traders not valuation purists.

Shares in Ultimate Products dropped sharply this week following a downbeat trading update that lowered expectations for both the current year and next. While the Group reported a 3% year-on-year rise in revenue over the four months to May, this was largely driven by lower margin product categories and sales channels. As a result, gross margins remained under pressure and adjusted EBITDA for the period was flat at £3.6 million, despite a fall in freight rates.

Ultimate Products designs, sources and distributes homeware goods under well known brands including Salter and Beldray. Although the company has made notable operational improvements in recent years such as deploying automation and AI, its latest update highlighted soft consumer sentiment and delayed orders from retailers, with over £4 million in sales pushed into the next financial year. Full year revenue is now expected to decline by around 4% versus last year, and adjusted EBITDA is forecast at £12.5 million, falling short of the £14.3 million analysts had been expecting.

Looking ahead, the outlook remains cautious. The order book for FY26 is currently tracking 7.5% below the same point last year, and management now expects revenue next year to be broadly in line with that weaker starting position. The Board said it is focusing on upgrading the sales function to match the operational gains already achieved and reiterated confidence in the Group’s long term potential. But with earnings under pressure and growth stalling, investors appear to be taking a wait and see approach.

REGENCY VIEW:

Ultimate Products looks cheap on paper, trading at just 9 times earnings with a chunky 5.4% yield and solid returns on capital but the market’s not buying it, with the share price down over 65% from its highs. Momentum is clearly broken for now, but for contrarians who believe in fundamentals over sentiment, this could be one to quietly accumulate while the crowd looks away.

Sector Snapshot

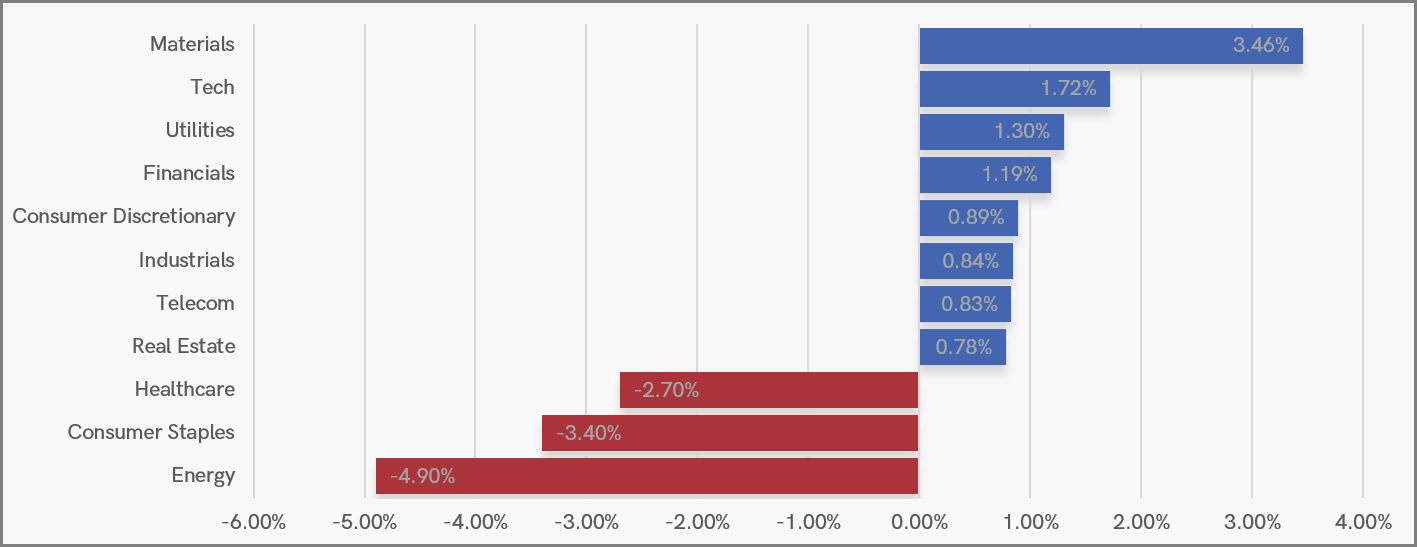

Despite another mild week for the broader market, Materials took the spotlight with a strong rebound, while Tech and Utilities also saw decent gains. Financials and Consumer Discretionary added to the upside, hinting at selective buying in both growth and cyclical names.

At the bottom end, Healthcare, Consumer Staples, and Energy came under pressure, dragging down the more traditionally defensive areas of the market. The divergence points to a market in rotation mode, with investors showing less interest in safety plays and more appetite for sectors with earnings leverage and commodity exposure.

UK Sector Performance (YTD)

UK Price Action

The FTSE has posted a second consecutive week of mean reversion, with prices drifting back toward the 50-day moving average. While there’s been no decisive rejection at resistance, short-term traders will be alert to signs of building bearish momentum. If the pullback continues in its current low-volatility form, the door remains open for a potential retest of resistance.

FTSE 100 Rolling Futures (Daily Candle Chart)

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.