27th Feb 2026. 10.40am

Weekly Briefing – Friday 27th February

| Market | Movement this week (%)* |

|---|---|

| FTSE 100 | +1.89% |

| FTSE 250 | -0.07% |

| FTSE All-Share | +1.70% |

| AIM 100 | +0.66% |

| AIM All-Share | +0.77% |

* Price movement from Monday's open at 8am

Regency View:

Weekly Briefing – Friday 27th February

Market Overview

Dear Investor,

This week we turn our attention across the pond to AI’s most dominant player, Nvidia, which released earnings on Wednesday. The numbers were, once again, formidable. Revenues surged, profits hit fresh records and guidance comfortably cleared expectations. In isolation, it was another statement performance from the company that sits at the heart of the AI infrastructure build-out.

The scale of the business today is extraordinary. Revenues have multiplied in just a few short years, operating margins remain near 60%, and returns on capital are in rarefied territory. Data centre demand continues to drive the story, with hyperscalers still committing vast sums to AI compute. This is not a fragile growth narrative, it is a company generating enormous cash flows with a balance sheet to match.

And yet, the market’s reaction was subdued. After an initial bounce, the shares settled back into a broad trading range that has defined much of the past six months. Technically, the stock is pressing against prior resistance rather than breaking decisively higher. When record profits fail to produce record price moves, it often signals that expectations are already elevated.

This is what a maturing theme looks like. Early in a structural boom, strong growth is enough to drive valuation expansion. Later on, the market starts asking tougher questions. How sustainable is hyperscaler spending? How concentrated is demand? Can margins remain at these levels if supply constraints ease? The AI build-out is real, but the scrutiny is increasing.

None of this suggests the AI story is fading. Nvidia remains the central supplier to one of the most powerful investment trends of the decade. But the tone has shifted from breathless enthusiasm to measured assessment. For investors, that shift matters. The next leg higher will likely require continued delivery rather than simply another impressive headline.

Wishing you a fantastic weekend,

Tom

Thomas Light – Chartered FCSI

Director of Research

Market Movers

On the rise: HSBC (LSE:HSBA) +6.7% on the week

HSBC delivered a solid set of full year numbers, with underlying performance doing the heavy lifting beneath a layer of one off charges. Reported profit before tax dipped to just under 30 billion dollars, largely due to impairment and restructuring items, but strip those out and profit actually rose strongly. Revenue increased by 4% to over 68 billion dollars, supported by strength in Wealth and Transaction Banking, while net interest income edged higher as the structural hedge continued to roll into better yields.

Return on tangible equity came in at 13.3% on a reported basis, but 17.2% excluding notable items, up meaningfully on the prior year. That underlying return profile is what caught the market’s attention. The bank also finished the year with a robust capital position, a stable CET1 ratio of 14.9% and a total dividend of 75 cents per share for the year, maintaining its 50% payout policy.

Looking ahead, management has raised its ambition. HSBC is now targeting a return on tangible equity of 17% or better for each of the next three years, alongside year on year revenue growth and disciplined cost control. Banking net interest income is expected to remain resilient, even as the rate backdrop evolves. In short, this is a bank talking confidently about growth, profitability and capital returns rather than retrenchment.

Regency View: HSBC continues to do exactly what we want from a large cap bank, generate solid returns, maintain capital strength and reward shareholders, all while the shares press to fresh highs. Having recommended the stock to our FTSE Investor clients, we remain comfortable riding the momentum while the fundamentals and price action stay aligned.

Aston Martin returned to the headlines this week with a sweeping cost cutting plan, announcing up to 20% of its workforce will be reduced as it looks to steady the ship. Management expects the move to deliver around 40 million pounds of annual savings, with the bulk of that benefit flowing through this year. At the same time, the group has trimmed its five year capital spending plan by delaying investment into electric vehicles, lowering the total envelope to 1.7 billion pounds.

The backdrop remains challenging. US import tariffs have been described as extremely disruptive, while demand in China has been subdued. The company continues to grapple with high debt levels of around 1.4 billion pounds and weak cash generation. In 2025, it posted an operating loss of more than 250 million pounds, underlining how far there is to go before profitability is restored.

Management is pointing to a material improvement in 2026, helped by cost savings and deliveries of its new Valhalla hybrid model. There has also been a small boost from a recent deal to monetise branding rights linked to its Formula One team. The shares did bounce after nine straight sessions of decline, but zoom out and the broader trend remains under clear pressure, with the stock still well below its highs and momentum weak.

Regency View: Aston Martin has an iconic badge, but at the moment this is a balance sheet and cash flow story rather than a glamour one. Until we see consistent evidence of improving margins and debt reduction, we are content to watch from the sidelines rather than try to catch a falling knife.

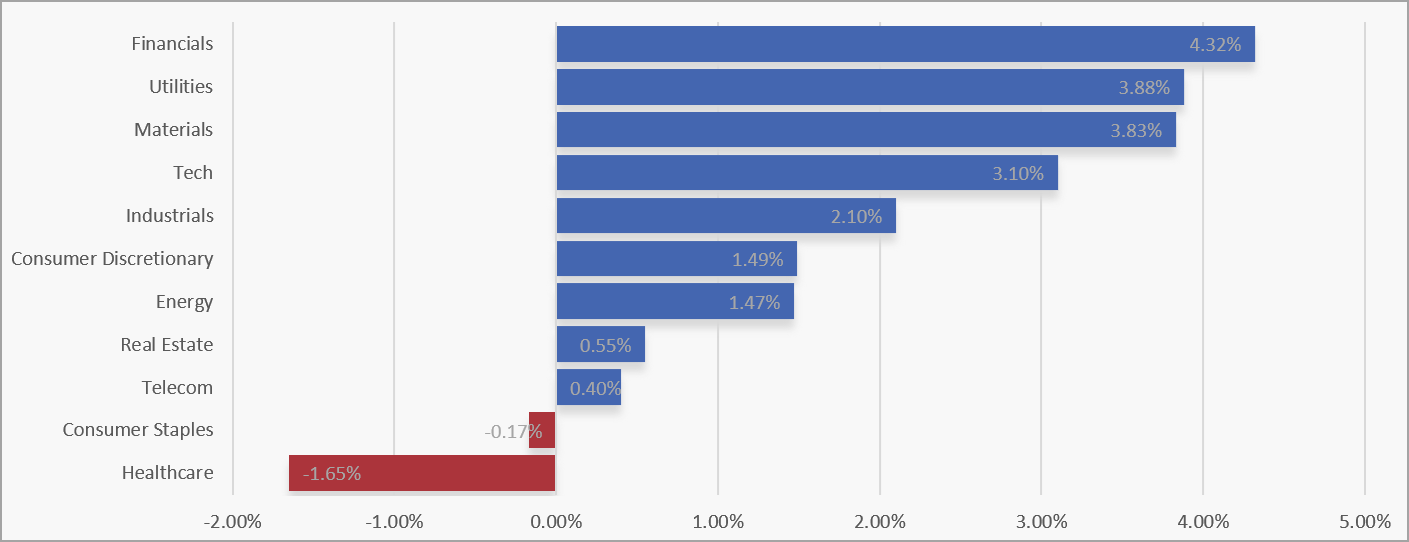

Sector Snapshot

Financials topped the table this week, with Utilities and Materials close behind, pointing to a strong and fairly broad-based rally. Tech and Industrials also delivered healthy gains, while Consumer Discretionary and Energy added to the positive tone, suggesting confidence across both cyclical and infrastructure-linked areas.

At the weaker end, Healthcare slipped back after recent strength, while Consumer Staples were marginally lower. Real Estate and Telecom posted only modest gains, indicating that leadership sat firmly with sectors offering earnings leverage and pricing power rather than pure defensiveness.

UK Sector Performance (7-Days)

UK Price Action

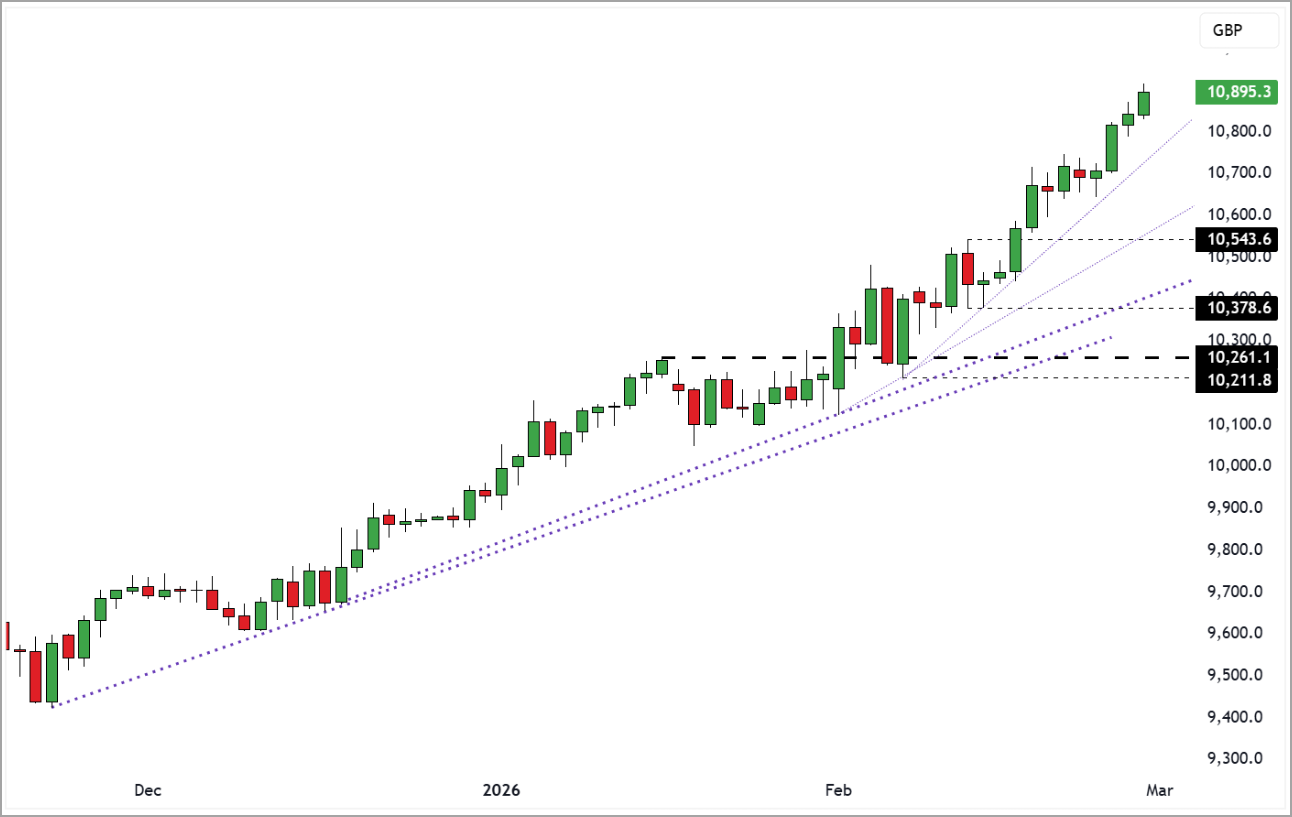

It has been more of the same for the FTSE this week, with the market continuing to grind higher within a well-defined uptrend. Price action remains orderly, with higher highs and higher lows building on what has already been an impressive start to the year.

The fan of rising trendlines continues to underline the strength of momentum, with each shallow pullback finding willing buyers. Until we see a meaningful break of that structure, the path of least resistance remains higher.

FTSE 100 Rolling Futures (Daily Candle Chart)

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.