23rd Jan 2026. 11.03am

Weekly Briefing – Friday 23rd January

| Market | Movement this week (%)* |

|---|---|

| FTSE 100 | -0.96% |

| FTSE 250 | -0.17% |

| FTSE All-Share | -0.86% |

| AIM 100 | +2.12% |

| AIM All-Share | +2.07% |

* Price movement from Monday's open at 8am

Regency View:

Weekly Briefing – Friday 23rd January

Market Overview

Dear Investor,

This week, Donald’s Davos shenanigans dominated proceedings. Trump loves Davos not because of policy nuance or global cooperation, but because it guarantees attention. Put simply, if the world’s press is in one place, Trump will find a way to turn it into a stage and this week was no exception.

Markets initially took the bait. Tariff threats tied to Greenland, pointed rhetoric towards Europe, and the usual air of brinkmanship knocked risk appetite early in the week. Those moves were likely amplified by thin conditions, with US markets closed on Monday for Martin Luther King Day, allowing the narrative to run a bit hotter than it otherwise might have done.

As has often been the case, cooler heads eventually prevailed. By mid week, Trump had begun to backtrack, ruling out force over Greenland and stepping away from near term tariff action. Markets responded in kind, recovering much of the early weakness as investors reassessed how much of the noise was likely to translate into policy reality.

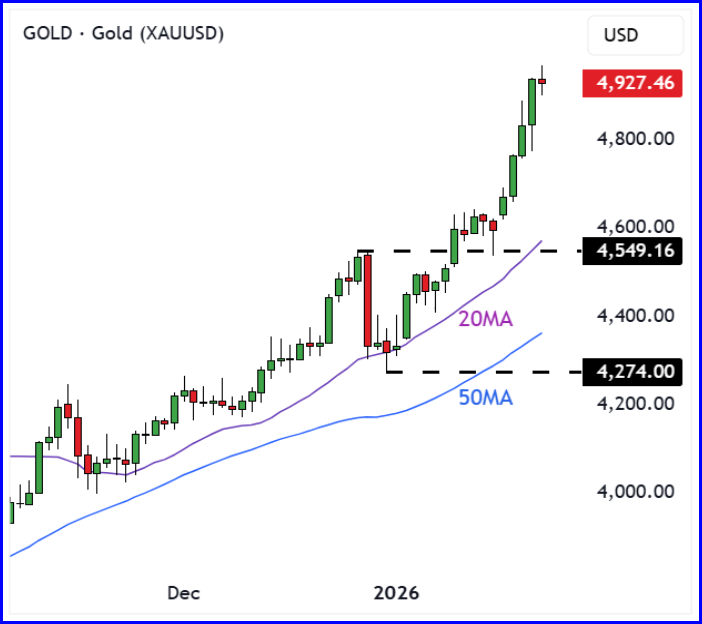

One area that didn’t look back was gold. The metal pushed to fresh highs as investors sought insurance against political unpredictability and growing unease around central bank independence in the US. That move felt less like panic and more like positioning, a quiet reminder that while equity markets can shrug off headlines, portfolios are still being built with hedges in mind.

The broader takeaway is familiar by now. Trumps political theatre remains a short term market mover, but its shelf life is getting shorter. For UK investors, the lesson is not to ignore the noise, but not to chase it either. This remains a market where patience, selectivity, and an ability to separate headlines from lasting impact matter far more than reacting to every twist in the script.

Wishing you a fantastic weekend,

Tom

Thomas Light – Chartered FCSI

Director of Research

Market Movers

On the rise: Funding Circle (LSE:FCH) +29.3% on the week

Funding Circle shares jumped this week after the group delivered a standout full year trading update that comfortably beat market expectations. Revenue rose to around £204m, up 28% year on year, while profit before tax reached roughly £20m, well ahead of forecasts and marking a sharp improvement on last year.

The real headline was strategic execution. Funding Circle achieved its FY26 revenue target a full year early, driven by continued strong demand from UK SMEs and growing traction across newer products such as FlexiPay and its cashback credit card. Credit extended rose 29% to £2.5bn, underlining that demand has remained resilient despite a choppy macro backdrop.

Investors also welcomed the capital return story. The company continues to progress its share buyback programme, having already repurchased a significant portion of its issued share capital, reinforcing confidence in the platform’s profitability and capital light model as it enters 2026.

Regency View: This update shows a business that has moved decisively from turnaround to execution mode, with growth now translating into meaningful profitability. While valuation is no longer trivial, momentum and operating leverage are clearly back on Funding Circle’s side.

Flutter’s share price drifted lower again this week, extending a decline that has been in place for several months despite the absence of any major company specific negative update. The weakness reflects a broader loss of momentum rather than a single catalyst, with investors reassessing growth expectations across the US online gambling space.

Part of the recent narrative has focused on the rise of prediction markets such as Kalshi and Polymarket, which allow users to trade simple yes or no outcomes on sporting events and other topics. While these platforms have seen rapid growth in volumes, their emergence has reignited concerns about competitive pressure on established sportsbooks, contributing to renewed caution around sector leaders like FanDuel.

That said, the longer term picture remains more nuanced. Forecasts suggest prediction markets may ultimately sit alongside traditional sportsbooks rather than replace them, with both benefiting from the structural shift from physical gambling to online platforms. For now though, sentiment has turned against the sector, and Flutter has been caught on the wrong side of that rotation.

Regency View: Flutter remains a business with enviable scale and strong underlying market positions, but the share price is telling us that confidence has ebbed. Until momentum stabilises and the narrative around competition and regulation cools, investors appear content to stay on the sidelines.

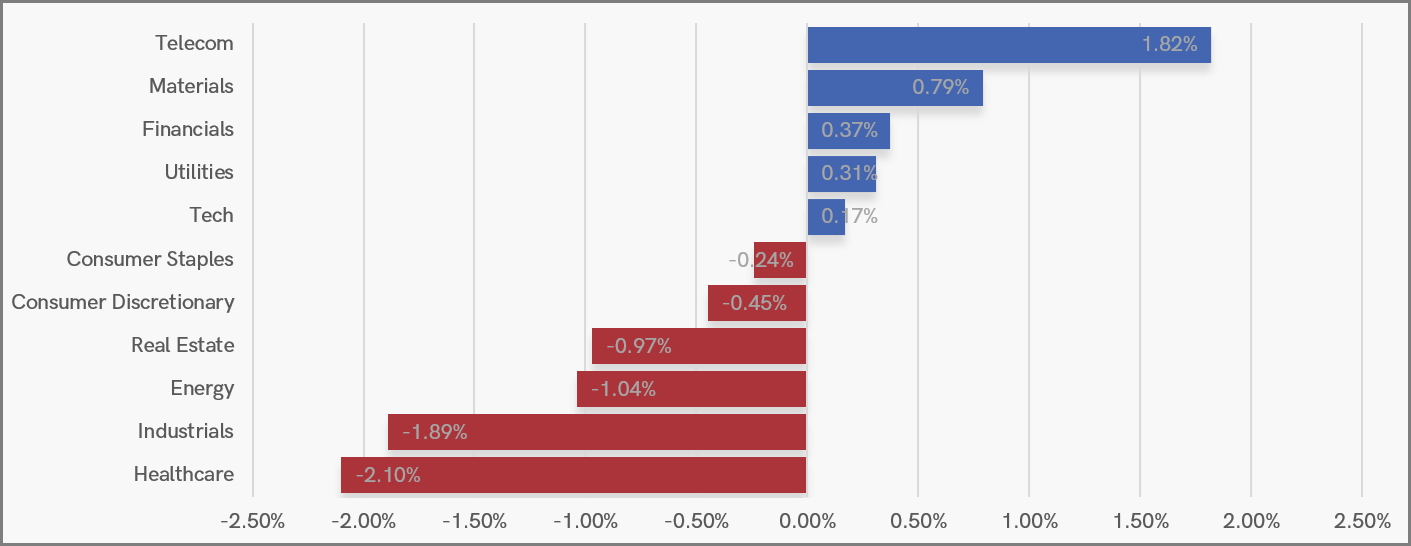

Sector Snapshot

This week marked a subtle shift in leadership compared with recent commodity-led moves. Telecoms topped the table, supported by steady demand for income and reliability, while Materials and Financials also managed modest gains. Utilities and Tech edged higher too, but overall leadership was narrow rather than broad-based.

At the other end, Healthcare and Industrials were the weakest performers, with Energy and Real Estate also slipping back. Consumer Staples and Consumer Discretionary both drifted lower, pointing to a market that is neither fully risk-on nor fully defensive, but instead feeling its way forward with a preference for stability over conviction.

UK Sector Performance (7-Days)

UK Price Action

Recent price action suggests the FTSE is cooling off rather than rolling over. We saw a pullback earlier in the week as the index moved in sympathy with European markets following renewed trade tariff rhetoric from Trump, which briefly unsettled short term momentum.

Since then, a partial walk back in tone has helped the market find its feet, with buyers stepping back in and steadying prices. The rebound has been measured rather than aggressive, pointing towards a phase of sideways consolidation as the market digests its recent run to new highs. With the broader trend still firmly intact, this looks more like a pause to reset momentum than the start of anything more sinister.

FTSE 100 Rolling Futures (Daily Candle Chart)

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.