18th Jul 2025. 10.52am

Weekly Briefing – Friday 18th July

| Market | Movement this week (%)* |

|---|---|

| FTSE 100 | +0.59% |

| FTSE 250 | +1.35% |

| FTSE All-Share | +0.67% |

| AIM 100 | +0.46% |

| AIM All-Share | +0.12% |

* Price movement from Monday's open at 8am

Regency View:

Weekly Briefing – Friday 18th July

Market Overview

Dear Investor,

This week has been dominated by US bank earnings, which serve as a barometer of both the health of the global financial sector and the wider economy. As we review the results from heavyweights like JPMorgan, Citi, Wells Fargo, and BlackRock, it’s clear that the US economy remains resilient, despite the ongoing economic uncertainty. The headlines are a mixture of optimism and caution, but overall, the numbers seem to suggest an economy that is holding up better than many had expected.

At the centre of these results is the US consumer. Both JPMorgan and Citi have reported that, despite high inflation and rising interest rates, the consumer remains “healthy.” Citi’s CEO, Jane Fraser, highlighted how the strength of the American entrepreneur and consumer is exceeding expectations, which has supported strong performance in both their wealth management and trading businesses. This sentiment was echoed by JPMorgan, whose CFO, Jeremy Barnum, pointed out that consumer spending remains stable, with no signs of significant stress despite the economic headwinds.

However, not all results have been positive. BlackRock, the world’s largest asset manager, posted a record $12.5 trillion in assets under management, underscoring its market dominance. But despite this, inflows were weaker than expected, with a large client withdrawing a hefty $52 billion. The firm still managed to weather the storm, but it’s a reminder that even the biggest players in the game can face challenges when it comes to maintaining client confidence in volatile markets.

For UK investors, the key takeaway here is the resilience of the US consumer, which continues to drive earnings for the banks. While some challenges remain, particularly in asset management and market volatility, the overall outlook for the financial sector is cautiously optimistic.

Wishing you a fantastic weekend,

Tom

Thomas Light – Chartered FCSI

Director of Research

Market Movers

On the rise: Ocado (LSE:OCDO) +32.1% on the week

Ocado’s shares bounced from long-term lows this week, buoyed by a strong first-half performance. The group reported a 77% increase in underlying earnings and a 13.2% rise in revenue, surpassing expectations. Ocado’s strategy of reducing costs and improving efficiency is paying off, as demonstrated by a significant £93 million reduction in cash outflows compared to the same period last year. This solid performance has reaffirmed the company’s goal of becoming cash-flow positive in its 2025/26 financial year, with the expectation to reach full-year cash positivity in 2026/27.

Despite challenges in its grocery retail partnerships, such as slower rollouts by major clients like Kroger and Sobeys, Ocado remains optimistic about future growth. The company’s key technology division, which saw a 15% revenue increase, continues to be a major driver. CEO Tim Steiner expressed confidence in securing new grocery clients as exclusivity agreements with current partners expire later this year. This opens the door for Ocado to expand its footprint in markets where it has already made significant inroads, notably in Spain with its expanded partnership with Bon Preu.

Investors are showing renewed confidence in Ocado, as evidenced by the 13% surge in its stock price. This rally comes after a challenging start to the year, where Ocado’s shares were down 12% amid market concerns about the pace of new technology deals. However, with a strong performance in the first half and a promising pipeline of new partnerships, Ocado is positioning itself for a more profitable future. The company’s ability to sign new clients and manage its cost base effectively will be crucial in ensuring continued growth and improving investor sentiment going forward.

REGENCY VIEW:

Ocado is still navigating a bumpy road with negative returns on capital and equity, making it a risky bet for those seeking stability. That said, if the company can land new partnerships and get its financial house in order, there could be some upside just don’t expect a smooth ride.

Shares in Churchill China dropped sharply on Thursday following a disappointing trading update that revealed the company’s financial performance in May and June was well below expectations. The manufacturer of performance ceramic products has struggled with reduced demand, particularly in export markets. While UK and USA sales have been solid, European and Rest of the World markets, especially Germany, have underperformed. Additionally, a shift from more expensive non-round pressure cast products to lower-priced round products has further pressured margins.

The restaurant sector, particularly independent establishments, has faced significant challenges, with cost pressures leading to market contraction. New installation projects have slowed, and increased competition has intensified the strain. However, Churchill noted that replacement business has remained steady, driven by its extensive installed base. Unfortunately, the shift towards lower-margin products has weighed on profitability, leading to reduced factory recoveries.

To address these issues, Churchill has scaled back production in line with weaker demand, contributing to lower margins. The company is also focused on improving its cost base and enhancing operational agility, having completed several capital projects to boost efficiency. New product launches, especially in inkjet and pressure cast products, are being fast-tracked to support growth. Despite these efforts, Churchill has warned that both revenue and profits for the full year will be significantly lower than last year, with market conditions remaining difficult.

REGENCY VIEW:

Churchill China has had a rough ride recently, with its stock down 55% over the past year as export demand falters and margins shrink. While the company is still in solid financial shape, the market is clearly cautious, and unless it can turn around sales outside the UK and USA, investors may need to brace for more bumps along the way.

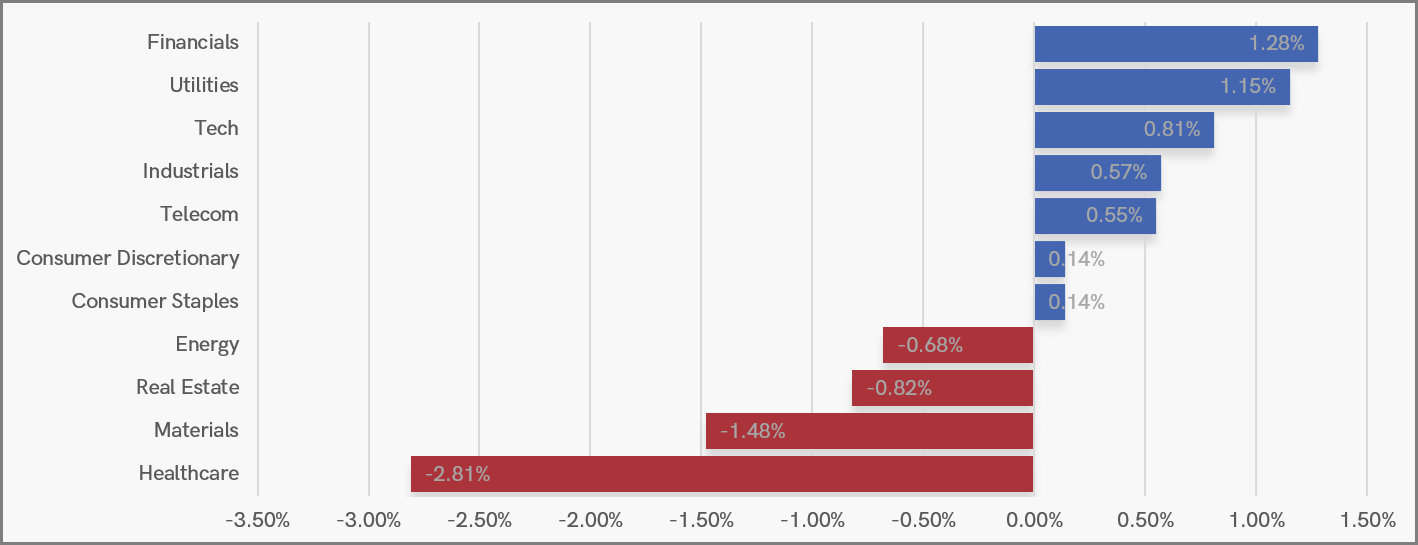

Sector Snapshot

Financials led the way this week, buoyed by strong results from their US counterparts which lifted sentiment across the sector. Utilities also posted solid gains, hinting at a layer of underlying caution despite the broader market hovering near record highs. Tech, Industrials and Telecoms added to the positive momentum, while Consumer Staples held firm.

Healthcare was the clear laggard, dragged lower by stock-specific losses in names like Convatec and Smith & Nephew. Consumer Discretionary and Materials also slipped, while Energy and Real Estate remained under pressure as the rotation away from rate-sensitive and cyclical names continued.

UK Sector Performance (7-Days)

UK Price Action

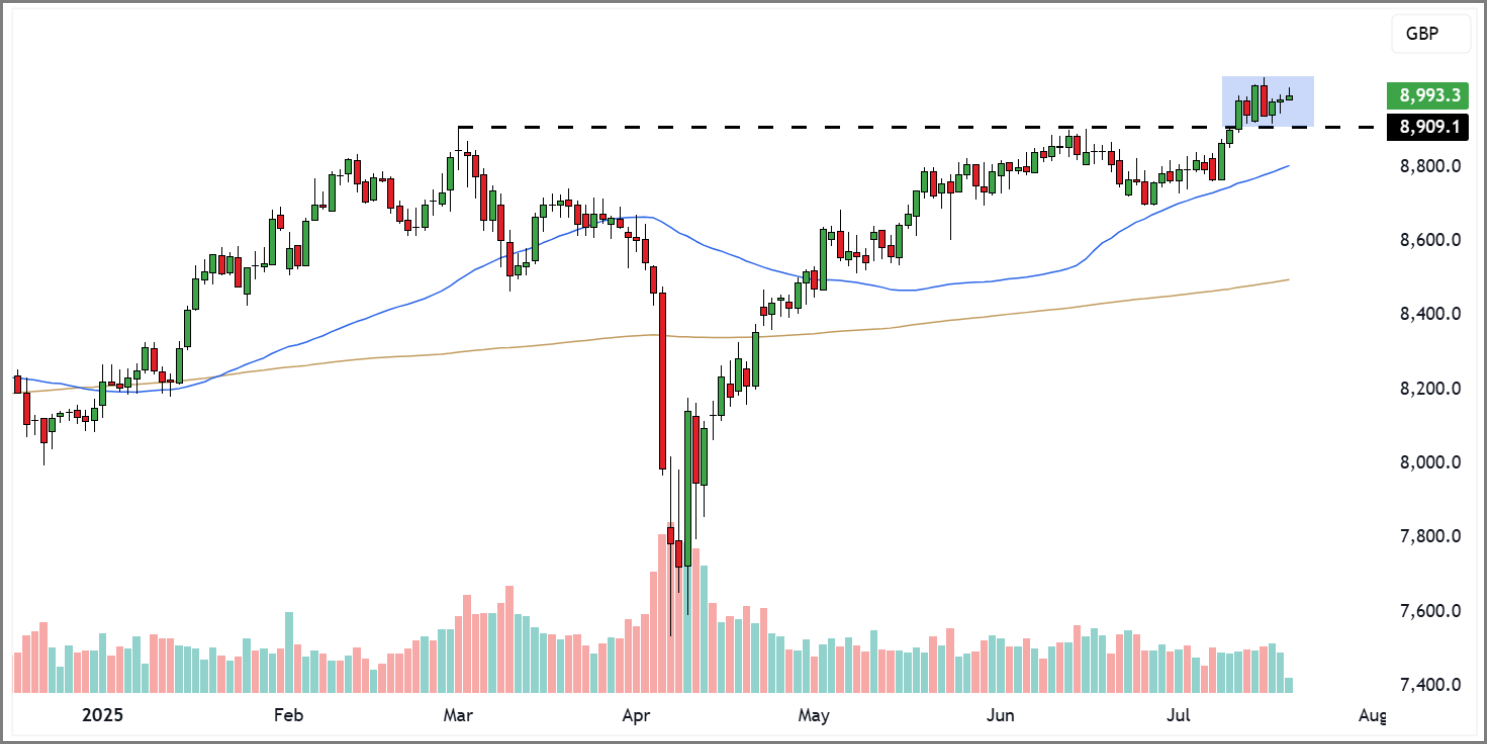

After last week’s breakout, we’ve seen a steady week of consolidation above the breakout zone. This is a bullish sign and suggests that the market is digesting the recent gains before potentially continuing higher. The FTSE 100 has held key support levels, and the consolidation pattern suggests that buyers are still in control, with any further upward movement likely to attract more momentum.

FTSE 100 Rolling Futures (Daily Candle Chart)

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.