17th Apr 2026. 10.17am

Weekly Briefing – Friday 17th April

| Market | Movement this week (%)* |

|---|---|

| FTSE 100 | -0.19% |

| FTSE 250 | +2.04% |

| FTSE All-Share | +3.13% |

| AIM 100 | +2.21% |

| AIM All-Share | +2.84% |

* Price movement from Monday's open at 8am

Regency View:

Weekly Briefing – Friday 17th April

Market Overview

Dear Investor,

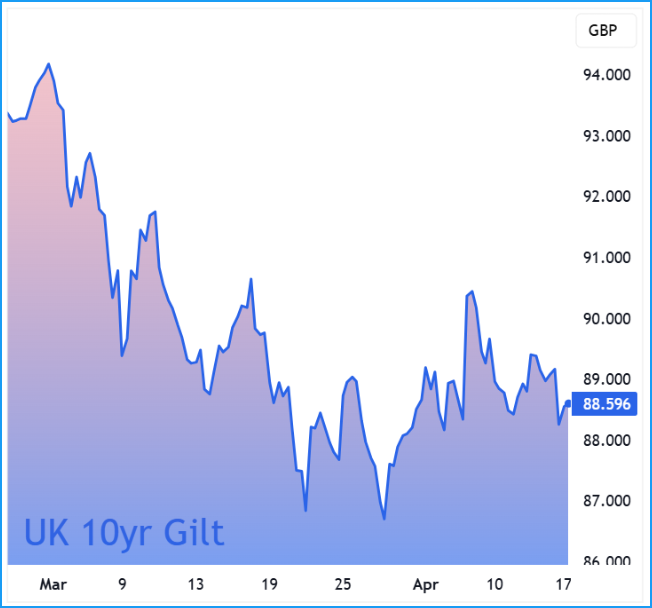

While stocks have been holding firm, the bond market has been telling a different story. With the S&P 500 pushing into fresh highs and the FTSE sitting just 3.5% off its peak, you would be forgiven for thinking markets are looking straight through the conflict in the Middle East, but under the surface, there are signs that investors are becoming a little more cautious.

The shift is showing up in government borrowing. The UK, France and Italy are all having to offer higher yields to attract buyers for their debt, which in simple terms means investors are demanding a better return for taking on the risk. It is not a crisis, but it is a change in tone, and these moves tend to happen before they show up elsewhere.

The driver is fairly clear. Higher energy prices risk keeping inflation sticky at a time when governments are already under pressure to spend more on defence and energy security. That combination matters, because it points to more borrowing at a time when balance sheets are already stretched.

This is where the UK starts to come into sharper focus. Alongside France and Italy, it falls into the camp of economies that do not have much room for manoeuvre, so when borrowing costs rise, the market pays closer attention. The risk is not just higher costs today, but the potential for those costs to compound if confidence wobbles.

For now, equity markets are choosing to focus on momentum, and that has served investors well. The underlying trend remains intact, and periods like this often create selective opportunities rather than broad-based risk. The message from the bond market is worth keeping in the back of your mind, but it is not a reason to step aside, it is simply a reminder to stay focused on quality, positioning and timing.

Wishing you a great weekend,

Tom

Thomas Light – Chartered FCSI

Director of Research

Market Movers

On the rise: Intertek (LSE:ITRK) +28.6% on the week

Shares in Intertek (ITRK) moved sharply higher this week after private equity group EQT confirmed it had submitted an indicative proposal to acquire the company, valuing the business at around £7.9bn. The approach, which equated to 5,150p per share, was rejected by the board, with EQT now considering its next steps ahead of a formal deadline in mid May.

The market reaction was immediate, with the shares jumping more than 13% on the day, making Intertek the top performer on the FTSE 100. While there is no certainty that a formal offer will materialise, the announcement has placed a spotlight back on the company, particularly given the premium implied by the proposal and the strategic interest from a large global investor.

This type of situation often creates a period of sustained attention, even if no deal ultimately emerges. With a clear timeline now in place under takeover rules, investors will be watching closely for any further developments, while the current share price is likely to remain sensitive to headlines and speculation around a potential bid.

Regency View: We recommended Intertek to FTSE Investor clients in January, attracted by its strong returns on capital, consistent cash generation and resilient operating model. The emergence of takeover interest has helped reprice that quality, with momentum now firmly back on the side of the bulls as the market reassesses the value of the business.

Shares in Imperial Brands (IMB) fell around 6% this week, slipping to their lowest level since late July 2025, as investors reacted to a cautious tone around the second half outlook despite broadly stable guidance.

The company reiterated its full-year expectations, pointing to low single digit revenue growth in the first half and a second half weighted performance. However, it flagged that while there has been no material impact from the Middle East conflict so far, the potential effect on trading conditions in the second half remains uncertain.

Alongside this, Imperial indicated it expects a modest reduction in market share across its top five markets in the first half, even as pricing continues to support revenue growth. Progress in next generation products remains ongoing, although this continues to come with increased investment and near term pressure on profitability.

Regency View: The fundamentals remain intact, but the market is starting to focus more on what could go wrong than what is already working. With momentum firmly to the downside, the shares are struggling to attract fresh buying interest despite the underlying cash generation.

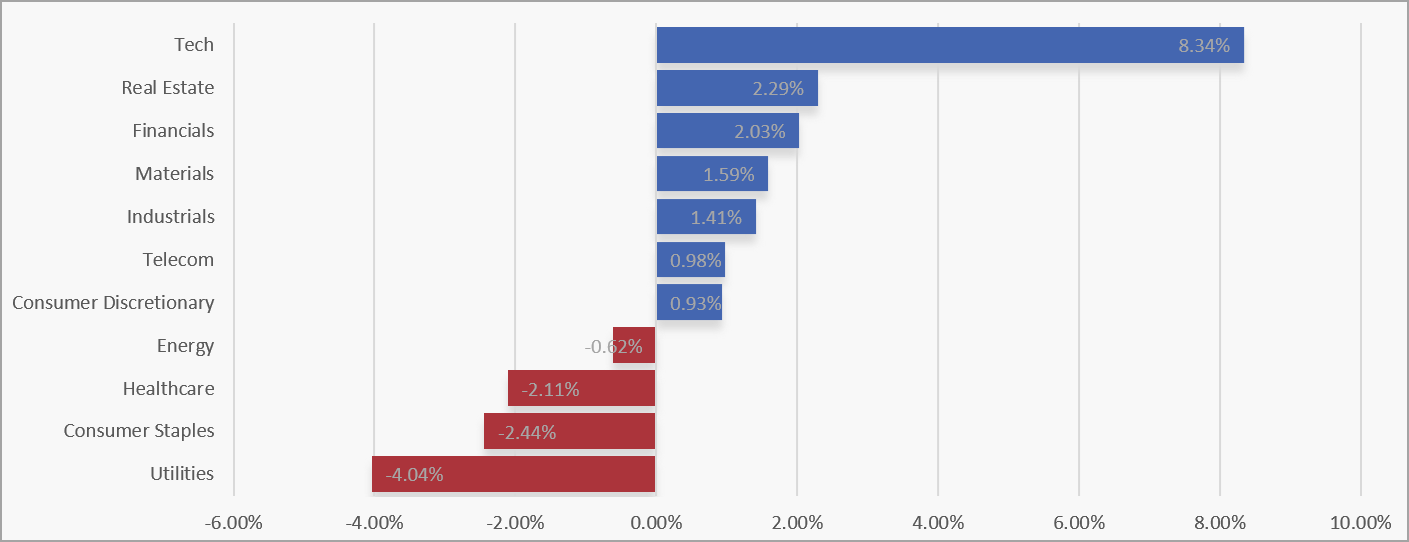

Sector Snapshot

Tech has dominated this week, surging well clear of the rest of the market and setting the tone. Real Estate and Financials followed with solid gains, while Materials and Industrials also moved higher, reinforcing the shift back towards cyclical exposure and growth-sensitive areas.

At the other end of the spectrum, Utilities and Consumer Staples came under the most pressure, with Healthcare also drifting lower. Energy slipped slightly after its recent strength, continuing the rotation away from defensives and prior leaders as capital is redeployed elsewhere.

UK Sector Performance (7-Days)

UK Price Action

It is a new week and the FTSE has largely tread water, consolidating near its recent highs after the sharp recovery seen earlier this month. Price is now forming a tight flag structure, suggesting the market is pausing to digest gains rather than showing any meaningful signs of rejection. In the context of the broader trend, this type of behaviour typically points to continuation, with the key question now being whether buyers have enough momentum to push through overhead resistance and extend the move higher.

UK100 Daily Candle Chart

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.