15th Aug 2025. 9.43am

Weekly Briefing – Friday 15th August

| Market | Movement this week (%)* |

|---|---|

| FTSE 100 | +0.95% |

| FTSE 250 | -0.36% |

| FTSE All-Share | +0.78% |

| AIM 100 | -0.34% |

| AIM All-Share | -0.18% |

* Price movement from Monday's open at 8am

Regency View:

Weekly Briefing – Friday 15th August

Market Overview

Dear Investor,

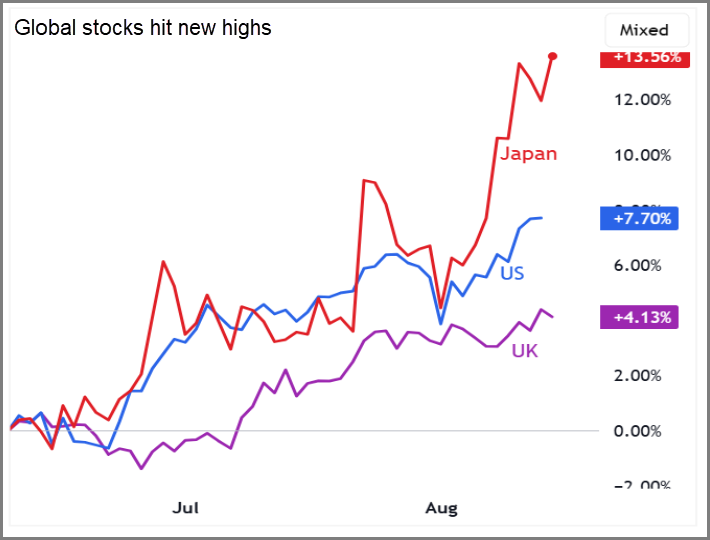

Global stocks have had a strong week as markets shrugged off lingering trade concerns and extended their rally. US inflation came in exactly as expected, giving traders fresh confidence that the Fed is likely to cut rates next month. That sense of certainty has flowed through Wall Street and across the globe, lifting indices in Europe and Asia to new highs and reminding investors that sentiment can be a powerful force when data aligns with expectations.

In Asia, Japan’s Topix hit an all-time high, while South Korea’s Kospi and Taiwan’s Taiex have marched steadily higher. A key driver has been the strong demand for semiconductors from the US, supporting major tech names and chipmakers. Companies such as SK Hynix and Sony Group saw solid gains, while Taiwan Semiconductor Manufacturing Company hit a fresh record, reflecting investor confidence that global tech demand remains robust even in the face of tariffs.

European markets have also enjoyed the tailwind, with the Stoxx Europe 600 and Germany’s Dax posting steady gains. The extension of the US-China trade truce has eased fears of immediate disruption, while expectations of lower US borrowing costs have boosted the markets view on European equities. Investors appear willing to focus on growth potential rather than headline trade noise, driving a mood that feels more optimistic than earlier in the year.

China and Hong Kong have been buoyed by domestic policy support for consumers and businesses, helping local equities recover. A weaker US dollar has added extra fuel to the rally, giving exporters in the region a natural boost. Combined, these factors are supporting the narrative that Asia is in a sweet spot for now: strong external demand, targeted policy support, and the tailwind of lower borrowing costs globally.

Wishing you a fantastic weekend,

Tom

Thomas Light – Chartered FCSI

Director of Research

Market Movers

On the rise: Spirax (LSE:SPX) +14.9% on the week

Shares in engineering group Spirax shot higher this week following the release of its half-year results, which showed revenue broadly in line with expectations despite a challenging macroeconomic environment.

Statutory operating profit and profit before tax were lower than the prior year, impacted by restructuring costs and currency headwinds, while adjusted figures were largely stable, reflecting steady underlying performance. Organic revenue growth outpaced global industrial production, supported by continued demand across key markets.

Segment performance varied across the business. ETS sales increased, driven by semiconductor demand, WMFTS orders grew in the Biopharm sector, and STS sales were stable organically, excluding large projects in China and Korea. Adjusted operating profit margins were largely unchanged on a reported basis, with organic margins improving slightly, and adjusted cash conversion rose, reflecting disciplined management of working capital and capital expenditure.

The group reiterated its full-year guidance, expecting second-half organic sales growth to accelerate, supported by strong order books and continued demand in high-margin segments. Currency headwinds and restructuring costs are anticipated to persist through the remainder of the year. Operational efficiency programmes and the phasing of benefits from restructuring are expected to contribute to margin improvement and cash conversion in the second half.

REGENCY VIEW:

Spirax continues to deliver a steady mix of quality and momentum, with strong returns on capital and equity underpinning its industrial footprint. Solid margins, healthy forecast earnings growth, and a consistent dividend illustrate a business that balances operational discipline with growth opportunities across its key markets.

Sage Group’s share price has continued its recent underperformance following its end-July trading update, despite reporting revenue growth across its cloud and AI-powered solutions.

Total revenue for the first nine months rose 9% to £1,862m, with Sage Business Cloud expanding 13% and recurring revenue up 10%, supported by continued growth in software subscriptions and strong penetration of cloud services. Growth was recorded across all regions, with North America up 11%, the UKIA region up 9%, and Europe up 7%, while sterling strength created an exchange rate headwind on reported figures.

On an organic basis, excluding the impact of acquisitions, total revenue increased 9% and recurring revenue rose 9%, reflecting momentum in Annualised Recurring Revenue (ARR). Cloud-native revenue grew 22% to £645m, and subscription penetration reached 83%, highlighting the continued contribution of recurring software sales to overall revenue. In the third quarter alone, total revenue increased 9% to £620m compared with the same period last year.

This week, European software stocks experienced broad declines, with heavyweight peers such as SAP, Dassault Systemes, and Nemetschek all falling sharply. Sage’s shares were also affected during this sector-wide selloff, coinciding with market concerns over the potential impact of artificial intelligence on the software industry.

REGENCY VIEW:

Sage’s cloud and AI-driven solutions continue to deliver steady growth, supported by a recurring revenue base that now accounts for the bulk of sales. Strong operating margins and a return on equity of nearly 37% underline the efficiency of its business model and the quality of its underlying performance.

Sector Snapshot

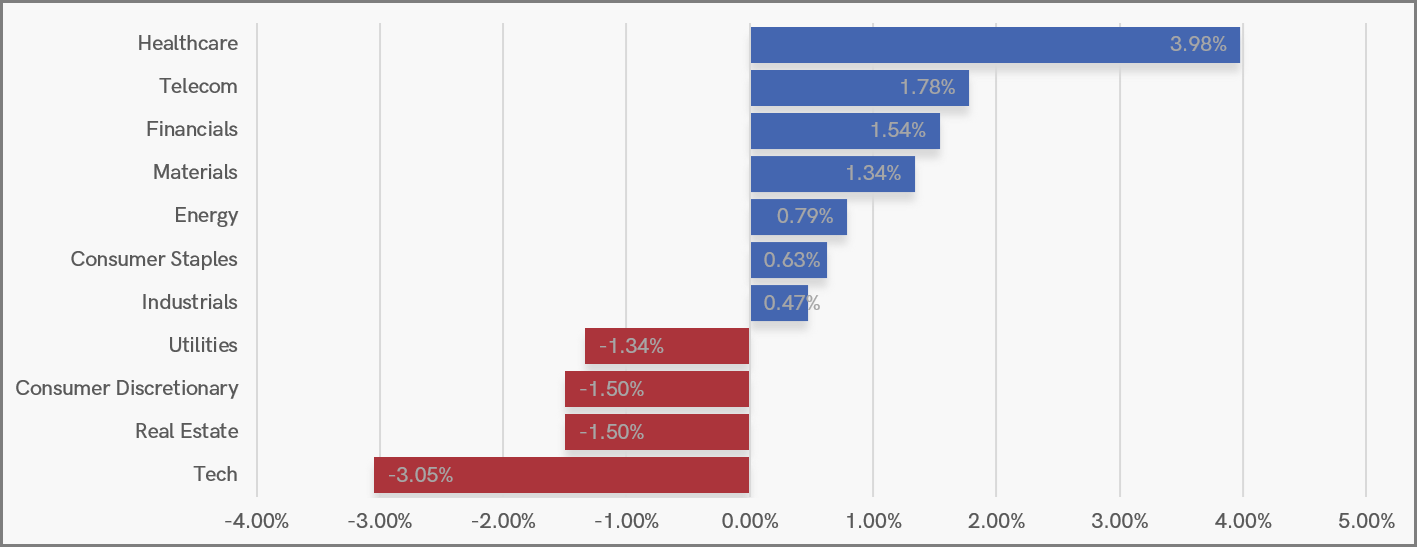

Healthcare led the way this week with strong gains, joined by Telecom and Financials in positive territory. Materials and Energy also contributed, while Consumer Staples and Industrials added modest support.

At the other end, Tech posted the sharpest decline, with Real Estate and Consumer Discretionary also under pressure. Utilities slipped too, leaving defensives struggling to find traction in this summer bull market.

UK Sector Performance (7-Days)

UK Price Action

Last week’s range on the FTSE has given way in line with the long-term uptrend. Traders will be watching for a weekly close above resistance at 9,175 to confirm the breakout and reduce the risk of the index slipping back into the previous range.

FTSE 100 Rolling Futures (Daily Candle Chart)

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.