13th Feb 2026. 10.25am

Weekly Briefing – Friday 13th February

| Market | Movement this week (%)* |

|---|---|

| FTSE 100 | +0.53% |

| FTSE 250 | +0.62% |

| FTSE All-Share | +0.54% |

| AIM 100 | +0.42% |

| AIM All-Share | +0.39% |

* Price movement from Monday's open at 8am

Regency View:

Weekly Briefing – Friday 13th February

Market Overview

Dear Investor,

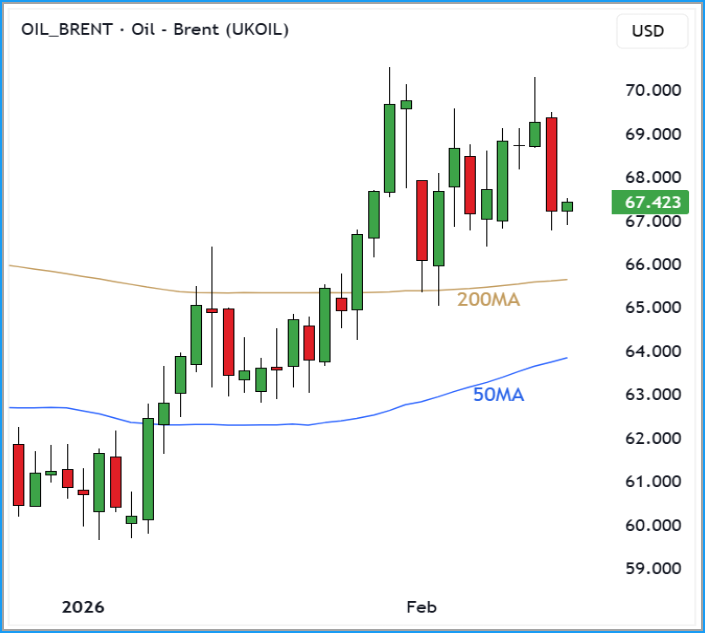

With headline news relatively thin this week, it has been oil quietly setting the tone.

OPEC’s latest report pointed to a small second-quarter surplus ahead of its early March production decision, yet Brent crude continues to trade as if the market is more focused on the bigger picture. On OPEC’s own numbers, full-year demand still outpaces current output, and that longer-term deficit narrative appears to be carrying more weight than near-term surplus projections.

The chart reflects that shift in tone. After carving out a base into the turn of the year, Brent has pushed through its short-term downtrend and reclaimed its 50-day moving average. The 200-day is now flattening just beneath price, suggesting the market is transitioning from correction to recovery rather than fading into another leg lower. Momentum has improved, but it has done so in a controlled fashion.

For the FTSE, this matters. Energy remains one of the index’s key pillars, and a stable to firm oil price provides an important underpinning. In recent weeks we have seen sector leadership rotate rather than break down. Oil holding near trend highs supports that broader picture of capital reallocation rather than risk aversion.

It may not have been a week packed with dramatic macro headlines, but when commodities start firming quietly in the background, it often tells you something about positioning. With OPEC+ set to decide on output in early March, oil could soon move from quiet support act to main stage catalyst.

Wishing you a fantastic weekend,

Tom

Thomas Light – Chartered FCSI

Director of Research

Market Movers

On the rise: Griffin Mining (AIM:GFM) +11.5% on the week

Griffin Mining moved higher after confirming that gold production has successfully commenced in Zone III of the Yuan Long orebody at its Caijiaying Mine. While gold initially represents around 5 to 10 per cent of daily output, the transition into sustained gold-only stopes marks an important operational milestone and introduces a recurring higher-margin feed source into the plant mix.

The real excitement sits beneath the headline. Ongoing drilling continues to return eye-catching high-grade intercepts, including 6 metres at 31.5 g/t and 5.9 metres at 71.2 g/t in the newly defined Fu Long feeder system. Management believes this high-grade corridor could materially expand the production footprint and enhance long-term flexibility, reinforcing the idea that Caijiaying remains a living, growing system rather than a mature, static asset.

Gold now becomes more than a discovery story. It is moving into the production profile, and importantly, doing so quickly. That operational agility has long been a hallmark of Griffin, with new discoveries being incorporated into mining plans at pace rather than sitting idle in the resource statement.

Regency view: Griffin combines operational momentum with a strengthening balance sheet and net cash position, while price action continues to reflect strong relative strength. After a powerful run, the key will be sustained grade delivery translating into cash flow growth rather than simply drill headline excitement.

St James’s Place fell sharply this week as concerns over artificial intelligence disruption rippled through the wealth management sector. The sell-off was triggered by weakness in US brokerage stocks after fintech platform Altruist unveiled AI-enabled tax planning tools, reigniting fears that technology could erode traditional advice models. Shares in St James’s Place dropped more than 10% at one stage, with Quilter and other European financial names also under pressure.

Importantly, there was no stock-specific trading update to justify the move. Analysts at RBC suggested the reaction appeared driven more by positioning and sympathy with US peers rather than a fundamental shift in outlook. Still, the speed of the decline highlights how quickly sentiment can turn when markets begin questioning whether established fee structures are defensible in an AI-enhanced world.

This comes against a backdrop of strong prior momentum. Despite recent weakness, the shares had recovered well from earlier lows and continue to trade on a mid-teens forward multiple, with forecast earnings broadly stable. The balance sheet remains relatively clean, leverage is modest, and dividend cover has improved, but markets are clearly demanding reassurance that advice-led models can demonstrate durability in an increasingly tech-driven landscape.

Regency view: The share price reaction feels more sentiment-led than structural at this stage. That said, when narratives shift from growth to disruption risk, volatility tends to persist until management clearly articulates how technology becomes an opportunity rather than a threat.

Sector Snapshot

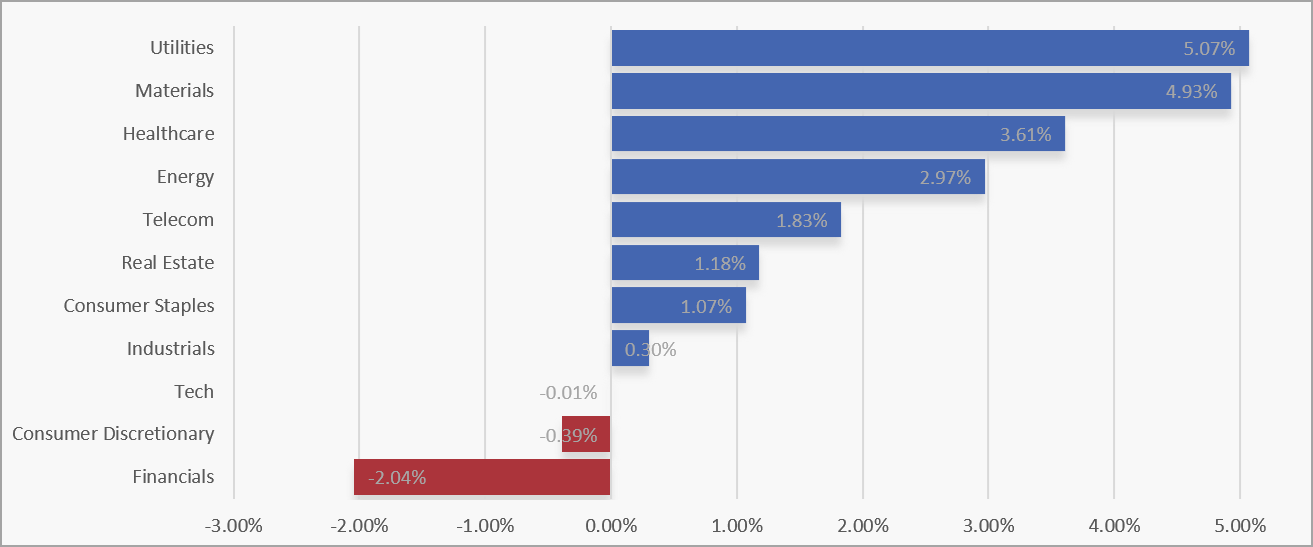

Utilities led the market this week, closely followed by Materials, with Healthcare and Energy also delivering strong gains. The leadership mix points to investors favouring a blend of defensiveness and hard-asset exposure, while Telecom, Real Estate and Consumer Staples added to the positive tone. Industrials were broadly flat, suggesting a more cautious approach to cyclical risk.

At the weaker end, Financials slipped back and stood out as the main laggard of the week. Tech and Consumer Discretionary were little changed to slightly lower, reinforcing the idea that leadership is currently sitting with sectors offering either stability or tangible asset backing rather than pure growth.

UK Sector Performance (7-Days)

UK Price Action

In the context of the wider trend, it has been another solid week for the FTSE, with the market pushing on to fresh highs and keeping the broader bullish structure firmly intact. The index continues to trade well above its rising 50 day moving average, which remains a reliable guide to the underlying trend.

That said, there are a few subtle signs that a deeper pullback could be on the cards. The break to new highs was followed by a close back below the prior swing resistance the very next session, a small but notable sign that momentum may be starting to cool. On its own this is not a reversal signal, but combined with the stretched run into February it does suggest the market may need to pause or retrace before the next leg higher can get going.

FTSE 100 Rolling Futures (Daily Candle Chart)

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.