12th Sep 2025. 10.45am

Weekly Briefing – Friday 12th September

| Market | Movement this week (%)* |

|---|---|

| FTSE 100 | +1.29% |

| FTSE 250 | +0.49% |

| FTSE All-Share | +1.18% |

| AIM 100 | +0.54% |

| AIM All-Share | +0.48% |

* Price movement from Monday's open at 8am

Regency View:

Weekly Briefing – Friday 12th September

Market Overview

Dear Investor,

This week saw some key themes reignite with defence demand and central bank divergence leading the way, as investors weighed currency moves and the next turn in the rate cycle…

Geopolitical tensions ramped up as Russian drones crossed into Polish airspace and Israel struck Hamas leadership in Qatar, marking a new level of risk in regions already simmering with conflict. For investors this was more than just another headline, it was a reminder that defence spending is not a passing theme but a structural shift that is gathering momentum. Defence stocks showed their strength with BAE Systems – a stock we highlighted to our FTSE Investor members some weeks ago – surging more than 8% this week.

The monetary policy picture told a different story. The European Central Bank opted to hold rates at 2%, emphasising the resilience of the eurozone economy and pointing to balanced risks rather than fresh worries. Inflation is hovering just above target and growth forecasts were nudged higher, which allowed Christine Lagarde to strike a more confident tone. Markets welcomed the pause, seeing it as confirmation that the ECB has room to watch and wait rather than being forced into further action.

Across the Atlantic the Federal Reserve faces a more complex challenge. Inflation ticked up to 2.9% in August, but the real concern is the labour market, where jobless claims hit their highest level since 2021 and payroll growth slowed dramatically. The market reaction has been decisive, with traders pricing in a September cut and beginning to lean towards a faster pace of easing. It looks increasingly clear that the Fed is at the end of its cycle, caught between still-elevated inflation and a weakening jobs market. That contrast with the ECB’s steadier tone has pushed EUR/USD within touching distance of four-year highs.

For UK investors this divergence has clear implications. A softer dollar environment tends to lift risk appetite globally, while a stronger euro reflects a degree of confidence in Europe that had been absent through much of the past two years. Sterling is left somewhere in the middle, but the broader takeaway is that central banks are no longer moving in lockstep.

Stepping back, the message of the week is twofold. Geopolitical risk is fuelling sustained interest in defence and security sectors, a theme that continues to deliver returns for investors who moved early. At the same time monetary policy divergence is becoming the dominant macro driver.

Wishing you a fantastic weekend,

Tom

Thomas Light – Chartered FCSI

Director of Research

Market Movers

On the rise: Anglo American (LSE:AAL) +13.3% on the week

Anglo American is one of the FTSE’s highest risers this week following news that it has agreed to merge with Canada’s Teck Resources in a deal that will create a $50bn copper-mining group. The combined company, to be called Anglo Teck, will be headquartered in Vancouver but retain its primary listing in London, alongside secondary listings in Johannesburg, Toronto and New York. Anglo will own 62.4% of the new group, while Teck shareholders will hold the remainder, with shareholder votes scheduled for the coming months and regulatory approvals expected to take up to 18 months.

The merger reflects Anglo American’s strategic push into copper, a metal in high demand as economies shift towards electrification and renewable energy. Anglo produced 770,000 tonnes of copper last year, while Teck is on track to deliver up to 525,000 tonnes in 2025 with expansion plans later this decade. The two companies already share ownership of large copper projects in Chile, including the Collahuasi and Quebrada Blanca mines, which will now be consolidated under the new entity.

Both companies have faced takeover pressure from larger rivals in recent years, most notably BHP’s £39bn bid for Anglo which fell through in 2024. The newly announced structure includes a $4.5bn special dividend for Anglo shareholders and is expected to deliver annual pre-tax cost savings of $800mn. Teck’s controlling shareholder Norm Keevil has given his backing, while the leadership of the new company will be split between Anglo’s Duncan Wanblad as chief executive and Teck’s Jonathan Price as deputy chief executive, with board representation evenly divided between the two groups.

REGENCY VIEW:

Anglo American is doubling down on copper just as demand for the metal heats up. The Teck deal gives it serious scale and a stronger hand in the energy transition.

Dunelm dropped sharply this week following cautious guidance in its full-year results, which highlighted a lack of sustained recovery in consumer demand despite a solid set of numbers. The company reported sales of £1.77bn for the year to 28 June 2025, up 3.8% on the prior year, with profit before tax increasing 2.7% to £211m, in line with market expectations. However, management warned that while early trading in the new financial year had been encouraging, consumer spending remained constrained by inflationary pressures, slow interest rate cuts and fragile confidence.

The retailer said regular promotions and discounts had been key to maintaining customer traffic, while investment in artificial intelligence-powered search tools was being used to strengthen digital engagement. Dunelm is also pushing ahead with store expansion, with plans to open between five and ten new superstores in fiscal 2026, following the milestone opening of its 200th store and first inner London location during the year. Outgoing chief executive Nick Wilkinson said the business had adapted to a volatile consumer environment, with Sainsbury’s executive Clodagh Moriarty set to take over leadership in October.

Analysts described the results as broadly solid, but sentiment was weighed down by the lack of evidence that consumer demand is staging a meaningful recovery. The update comes against a backdrop of concerns across the UK retail sector, with retailers warning the government earlier in the summer that higher taxes and labour costs could squeeze household budgets further. Shares in Dunelm fell 7.3% as investors reacted to the outlook, even as the group reiterated confidence in its long-term target of reaching 10% market share in the homewares and furniture sector.

REGENCY VIEW:

Dunelm’s financial strength is clear with high returns on capital and a well-covered dividend yield above 5%, but the latest results underline the drag from weak consumer demand. With growth forecasts modest and the market yet to show signs of a real recovery, investors are weighing the income appeal against a tougher trading backdrop.

Sector Snapshot

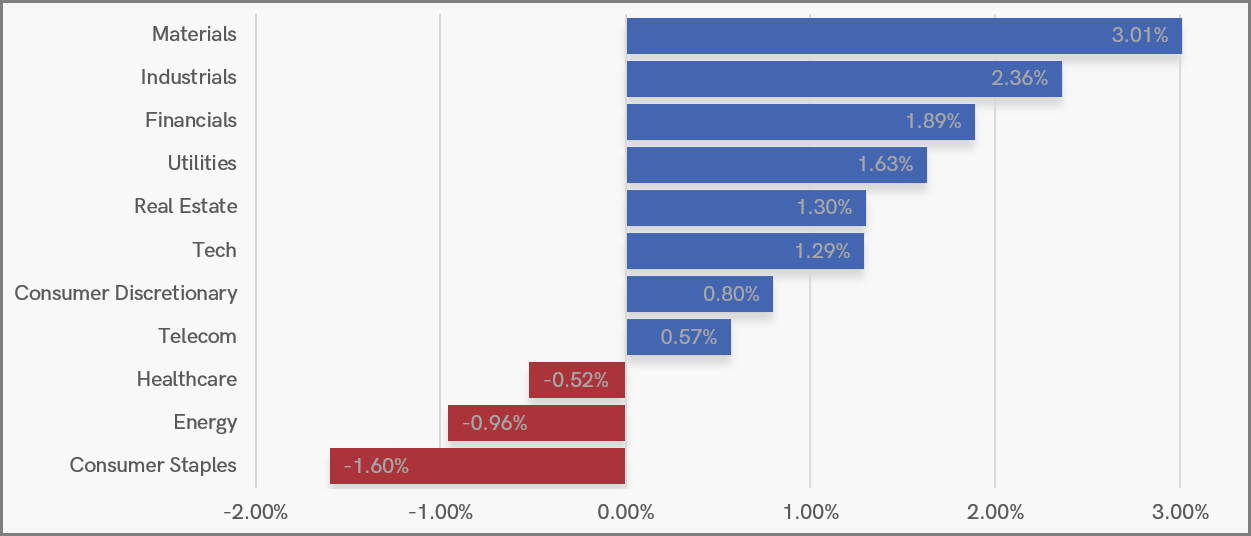

Materials and Industrials were out in front this week, with Financials also delivering strong gains as investors rotated towards sectors more closely tied to economic activity. Utilities, Real Estate and Tech added to the momentum, giving the market a broad base of support.

On the downside, Healthcare, Energy and Consumer Staples all slipped, leaving defensives and commodity-linked names mixed. Consumer Discretionary and Telecom managed modest gains, but leadership clearly rested with the cyclicals.

UK Sector Performance (7-Days)

UK Price Action

The FTSE has been a standout example of trend continuation in recent weeks. After digesting gains with a steady pullback inside a descending channel, the market has broken higher and now looks poised for a run back towards the August swing highs.

FTSE 100 Rolling Futures (Daily Candle Chart)

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.