11th Jul 2025. 11.08am

Weekly Briefing – Friday 11th July

| Market | Movement this week (%)* |

|---|---|

| FTSE 100 | +1.20% |

| FTSE 250 | +0.16% |

| FTSE All-Share | +1.07% |

| AIM 100 | -0.32% |

| AIM All-Share | -0.24% |

* Price movement from Monday's open at 8am

Regency View:

Weekly Briefing – Friday 11th July

Market Overview

Dear Investor,

If ever you needed evidence of the old saying “markets rise on a wall of worry”, this week has delivered it in spades…

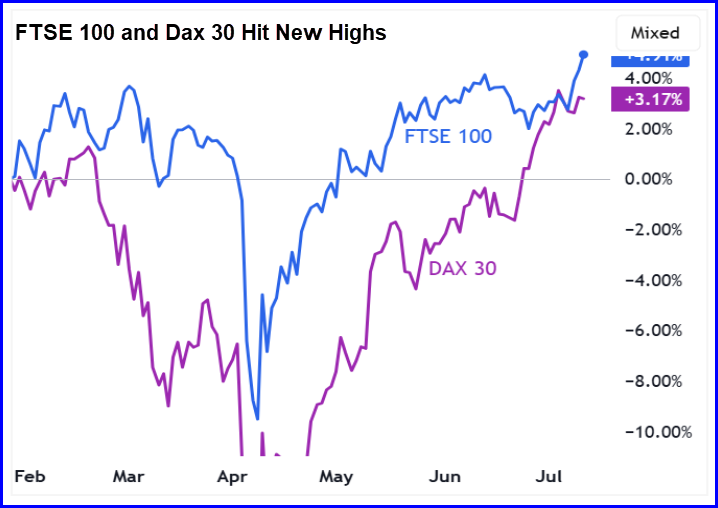

While Donald Trump unleashed a new wave of tariff threats, hitting copper imports with a 50% levy and promising the same for a growing list of countries, global equity markets have quietly marched to new highs. The FTSE 100 and Germany’s DAX both broke out to fresh records, following last week’s breakout in the S&P 500. That’s three major indices at all-time highs, even as headlines scream trade war and central banks warn about inflation.

The contrast couldn’t be sharper. Trump’s copper tariffs, set to take effect at the start of August, were justified on national security grounds, with the former president tying the metal to everything from ammunition to data centres. Chile, the US’s top supplier, has pushed back firmly, saying the US doesn’t have the capacity to replace its refined copper. Brazil, facing a similar 50% tariff on broader goods, has already signalled it will retaliate. The list of targeted countries is growing, and the rhetoric is political, strategic and pointed, often in equal measure.

Yet for all the noise, the market’s reaction has been surprisingly calm. Copper prices surged on the initial news, but equities haven’t flinched. Investors seem to be looking past the headlines and focusing on fundamentals. Inflation is easing, rate cuts remain on the table, and corporate earnings have been better than feared. Even the Federal Reserve, which flagged the risk of tariffs causing persistent effects on inflation, hasn’t shifted its stance in any meaningful way.

It’s also worth noting that while the tariffs grab attention, the practical impact may be more limited than it first appears. The US imports about 17 billion dollars of copper and derivatives annually, with much of it coming from long-established trade partners. Chile has said it will simply sell its copper elsewhere. Meanwhile, global copper demand continues to be driven by the energy transition and AI infrastructure, structural trends that no tariff can unwind overnight.

For now, markets are telling their own story. While the headlines churn, the trend remains up. That doesn’t mean investors should be complacent, but it does remind us that markets often price in fear long before it materialises. And right now, they seem far more interested in growth than geopolitics.

Wishing you a fantastic weekend,

Tom

Thomas Light – Chartered FCSI

Director of Research

Market Movers

On the rise: Metals One (AIM:MET1) +28.8% on the week

Shares in Metals One have continued to push higher following the release of their full-year results at the end of June 2025 and a flurry of portfolio-expanding activity since then. The group more than doubled the mineral resource at its flagship Black Schist Project in Finland during FY24, with over 57 million tonnes now estimated to contain substantial volumes of nickel, copper, cobalt and zinc. A preliminary economic assessment published earlier this year showed the project is highly leveraged to commodity prices, laying a foundation for future upside in a rising metal market.

Exploration success has also continued in Norway, where fresh drilling at the Råna Project intercepted new nickel-copper mineralisation, further strengthening the geological case for scale. But what is really capturing investor attention is the pace of Metals One’s post-period expansion. Since April, the company has announced a string of strategic acquisitions across Finland, Norway and the United States, adding copper, uranium, vanadium, gold and platinum group element assets to its pipeline. These moves are positioning the company not just as a critical minerals explorer, but as a diversified resource platform closely aligned with the energy transition theme.

Chair Craig Moulton described the company as “markedly more diversified” than it was just months ago, and that ambition is already being reflected in the market reaction. With fresh funding secured and drilling tenders already in motion for its newest projects, Metals One appears to be shifting gears from pure exploration to aggressive portfolio building. Investors seem to be warming to the strategy, and the momentum reflects growing confidence that this small-cap explorer is thinking much bigger.

REGENCY VIEW:

Metals One is a high-risk high-reward explorer with no revenue to speak of but a rapidly expanding portfolio of critical and precious metal projects across Europe and the US. While the fundamentals remain speculative, the company is clearly positioning itself to ride long-term themes like the energy transition and resource security, which will appeal to investors with a taste for early-stage potential and a strong stomach for uncertainty.

Shares in WPP dropped sharply this week following a disappointing first-half trading update that revealed weaker-than-expected revenue and profit performance. The company warned that like-for-like revenue less pass-through costs for the first half of 2025 is expected to fall between 4.2% and 4.5%, with a steeper decline of up to 6% in the second quarter alone. Management attributed the slump to a tougher macroeconomic backdrop and softer new business momentum, while also noting one-off factors and severance costs at WPP Media that have further pressured margins.

The result is a significant downgrade to full-year guidance. WPP now expects a decline of 3% to 5% in like-for-like revenue less pass-through costs for 2025, compared to its earlier forecast of flat to down 2%. Operating profit margins are also set to contract by up to 175 basis points year-on-year, a notable shift from the company’s previous expectation of maintaining flat margins. The combination of falling revenues and the need to absorb restructuring costs is forcing the group to walk a tightrope between preserving profitability and investing in long-term growth.

Chief Executive Mark Read acknowledged that trading conditions have worsened, particularly in June, and warned that the soft momentum seen in the first half is likely to continue into the second. Despite the downgrade, WPP remains focused on cost discipline and longer-term investment. However, with client budgets under pressure and new business wins falling short of expectations, the near-term outlook looks increasingly challenging. Investors appear to be recalibrating expectations accordingly.

REGENCY VIEW:

Despite the sell-off, WPP now trades on just 5.7 times forward earnings with a dividend yield pushing 8%, a valuation that screams deep value even if sentiment is firmly against it. With momentum firmly in reverse and the share price down over 50% from its highs, this is one for the contrarians keeping a cool head and a long-term view.

Sector Snapshot

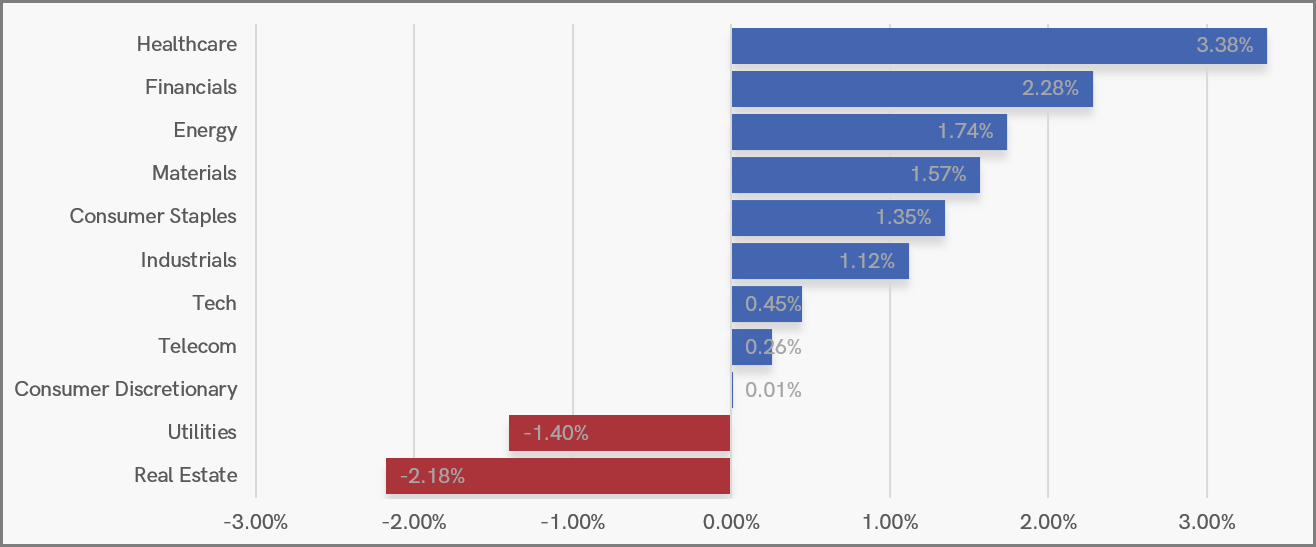

It’s been a strong week for UK stocks, with gains across most sectors led by a strong showing in Healthcare and Financials. Energy and Materials also added to the upside, supported by stable macro data and improved sentiment around earnings resilience.

Defensives were less convincing. Utilities slipped into the red, while Real Estate ended the week firmly at the bottom of the pile. The rotation suggests a market still favouring fundamentals and cash flow strength over rate-sensitive, asset-heavy names.

UK Sector Performance (7-Days)

UK Price Action

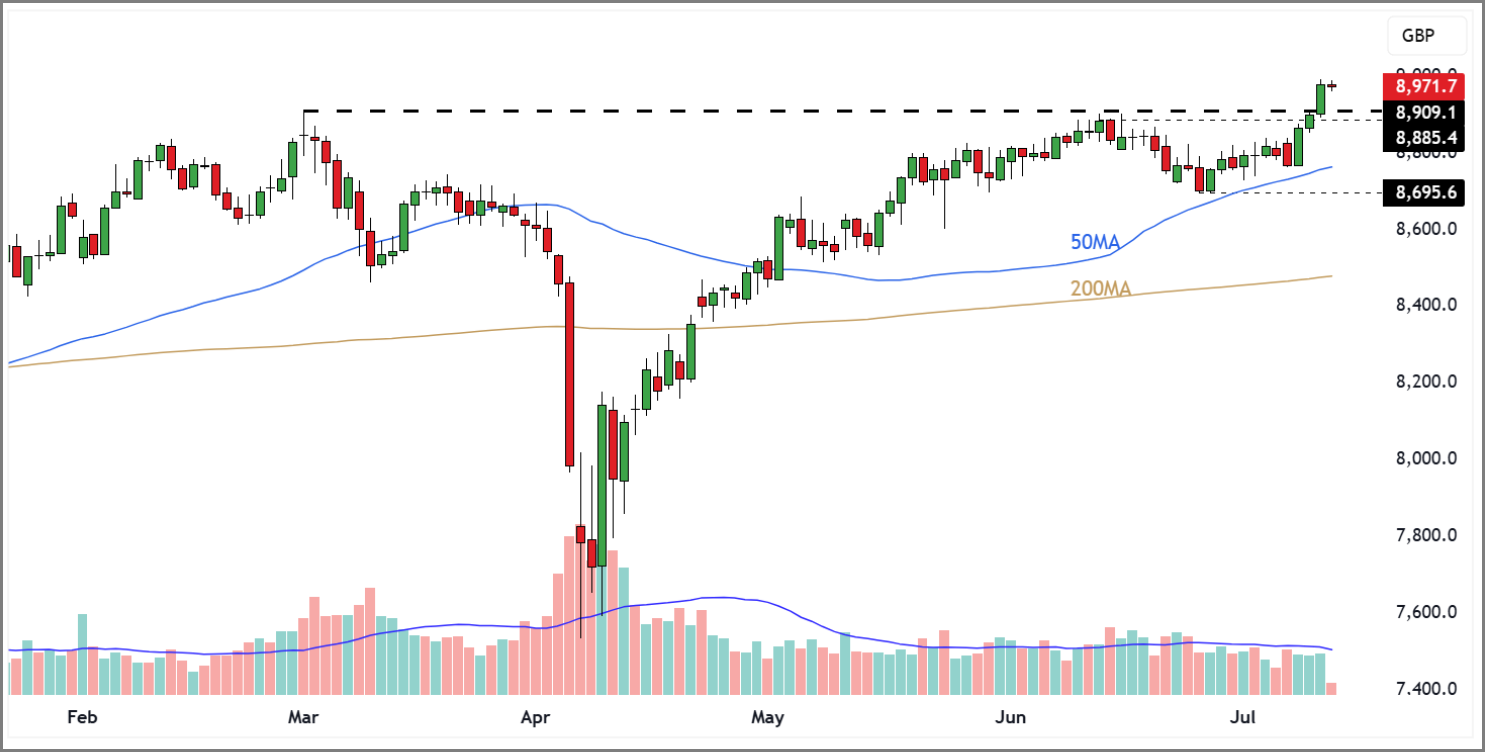

After spending nearly two months consolidating below a key resistance level, the FTSE has finally broken higher. The move aligns with the prevailing long-term uptrend, though it is notable that the breakout has not been accompanied by a meaningful pickup in volume, which is not unusual for this time of year. Attention now turns to whether broken resistance can hold as support in the sessions ahead.

FTSE 100 Rolling Futures (Daily Candle Chart)

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.