10th Sep 2025. 9.03am

Regency View:

Update

Regency View:

Update

It’s been a relatively quiet fortnight for newsflow on our FTSE stocks after the busy summer earnings period. We’ve seen a small mix of trading updates and strategic shifts, with themes of resilient growth, regulatory scrutiny, and sector-defining deals. From robust order books in tech services to nuclear life extensions in energy and consolidation in global mining, companies continue to shape their long-term narratives.

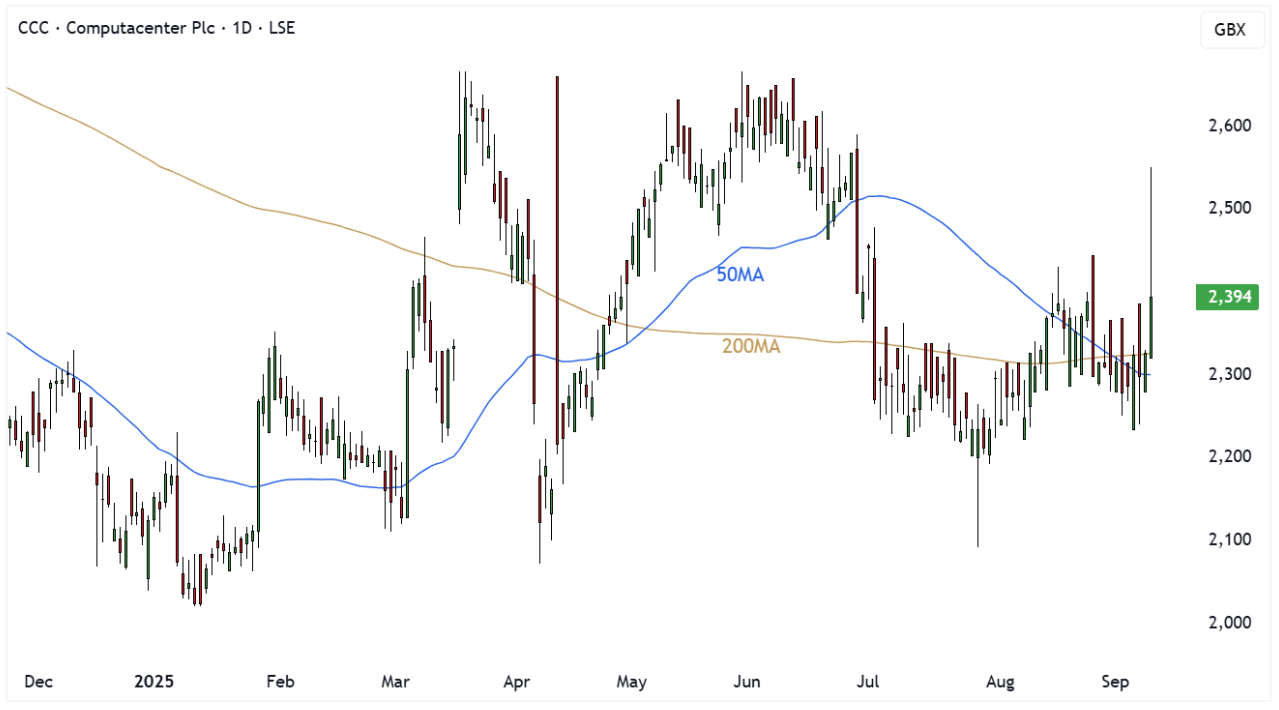

Computacenter rides North American momentum

Computacenter (CCC) reported half year results showing revenue growth of 28.5% to £3.99bn and gross profit up 6.8% to £504m. Strength in Technology Sourcing, particularly in North America, was the standout driver, with operating profits in the region nearly doubling year on year. The UK also returned to growth, although public sector weakness in Germany and France weighed on performance.

Margins came under pressure, with gross margin falling from 15.2% to 12.6%, reflecting a mix shift towards lower-margin product sales and higher investment in strategic initiatives. Net funds reduced to £115m after completing a £200m share buyback in late 2024, but the balance sheet remains sound with £278m of adjusted net funds. The interim dividend edged higher to 23.6p, continuing a track record of consistent shareholder returns.

We believe the attraction lies in Computacenter’s scale and proven ability to capture share in large technology markets. North America now represents 44% of adjusted operating profit, and a strong order backlog points to further gains. While European softness is a near-term drag, management expects recovery in the German public sector in H2, underpinning guidance for full year profit growth.

CCC Daily Candle Chart

Centrica extends nuclear output

Centrica (CNA) confirmed that its Heysham 1 and Hartlepool nuclear power stations will continue running until March 2028, extending their operational lives by one year. The extension is expected to add around 3 terawatt hours of generation between 2026 and 2030, strengthening the UK’s domestic energy supply.

The announcement highlights the role of legacy nuclear assets in bridging the UK’s energy transition. For Centrica, additional output from these plants enhances cash flow visibility and provides a modest earnings uplift, while also improving security of supply at a time of continued volatility in European power markets.

Centrica’s balance sheet and cash generation remain in focus following recent shareholder distributions, and incremental nuclear capacity helps underpin future dividends. The extension does not transform the investment case on its own, but it supports the broader theme of a more stable and predictable earnings base, which investors value highly in a volatile sector.

CNA Daily Candle Chart

Drax under the regulator’s microscope

Drax (DRX) disclosed that the Financial Conduct Authority has launched an investigation into past statements about its biomass sourcing between January 2022 and March 2024. The probe centres on the accuracy of sustainability claims, an issue that has already attracted media and political scrutiny.

Operationally, Drax continues to generate cash from its biomass and hydro portfolio, but investor confidence has been shaken by recurring questions over governance and transparency. An FCA investigation raises the stakes materially, with potential regulatory, reputational, and financial consequences depending on its outcome.

For shareholders, the near-term risk is less about immediate earnings and more about sentiment and valuation. Until the matter is resolved, the shares are likely to carry a governance discount, offsetting otherwise stable fundamentals. Longer term, clarity from the FCA process should allow us to reassess whether the current yield and cash flow are sufficient compensation for regulatory risk.

DRX Daily Candle Chart

Glencore gains from copper consolidation

Glencore (GLEN) found itself in the spotlight after Anglo American and Teck Resources agreed to merge into a new company, Anglo Teck. The combined entity will be London-listed with a market value of over $53bn and cost synergies of $800m, creating a heavyweight rival in copper.

Glencore had previously pursued Teck, so the deal effectively closes off a key acquisition path. However, the formation of Anglo Teck highlights the industry’s focus on copper, where demand is expected to surge thanks to electric vehicles and energy-hungry data centres. For Glencore, the rally in its shares reflects the market reassessing its own position within this reshaped competitive landscape.

Investors should note that Glencore retains one of the deepest copper portfolios globally, alongside strong trading and marketing operations. While the Anglo Teck deal raises competitive pressure, it also reinforces the structural copper bull case, from which Glencore is set to benefit. In the near term, the shares may continue to ride copper sentiment, but management’s next strategic move will be closely watched.

GLEN Daily Candle Chart

Kainos sets sights higher

Kainos (KNOS) issued its scheduled H1 trading update, guiding revenue for FY26 to the upper end of consensus at around £385m to £393m. Adjusted profit before tax is expected to be in line with forecasts at roughly £66m, with momentum strongest in its Workday Products division, which has just surpassed $100m in annual recurring revenue.

The company continues to execute across all three divisions. Digital Services secured high-profile contracts in the Home Office, NHS England and DVSA, providing visibility into H2 growth. Workday Services returned to growth across Europe and North America, with international expansion into Australia, New Zealand and Mexico also contributing.

The market enjoyed the update which caused the shares to surge higher. We believe Kainos offers a combination of recurring revenues, long-term public sector contracts, and exposure to structural drivers such as AI adoption and regulatory change. With a strong backlog, solid balance sheet and a clear runway for international growth, Kainos looks well placed to deliver compounding returns, even if the commercial sector remains subdued in the short term.

KNOS Daily Candle Chart

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.