12th Feb 2025. 8.59am

Regency View:

Update

Regency View:

Update

Airtel Africa breaks higher as growth accelerates

Airtel Africa’s (AAF) share price has continued its stellar start to the year, breaking to new trend highs on the back of an impressive set of Q3 results.

The latest results show the business continuing to deliver on its strategy, with a 7.9% increase in its total customer base to 163.1 million and rising demand for data and mobile money services. Data customers grew by 13.8%, with usage per customer up 32.3%, while mobile money transaction values surged by 33.3% in constant currency. The company’s investment in network expansion, with 2,850 new sites and a 20.8% increase in capacity, is paying off as it captures growing demand across its footprint.

Revenue growth of 20.4% in constant currency terms highlights the company’s resilience, despite currency devaluations dragging on reported figures. Mobile money and data services remain the core growth engines, with revenues rising by 29.6% and 29.5%, respectively, as customer penetration deepens. EBITDA margins have expanded quarter-on-quarter, reflecting the early success of cost efficiency measures, while the company continues to strengthen its capital structure by reducing foreign currency debt exposure. A second $100 million share buyback programme reinforces the Board’s confidence in long-term growth, providing further support for the share price.

With signs of stabilisation in key currencies and the recent regulatory decision in Nigeria allowing tariff adjustments, the operating environment is starting to look more favourable. Airtel Africa’s focus on execution, network investment, and digital services is positioning it well to benefit from the structural growth story in its markets. As demand for connectivity and financial inclusion accelerates, investors are increasingly backing the company’s ability to sustain its upward trajectory.

AAF Daily Candle Chart

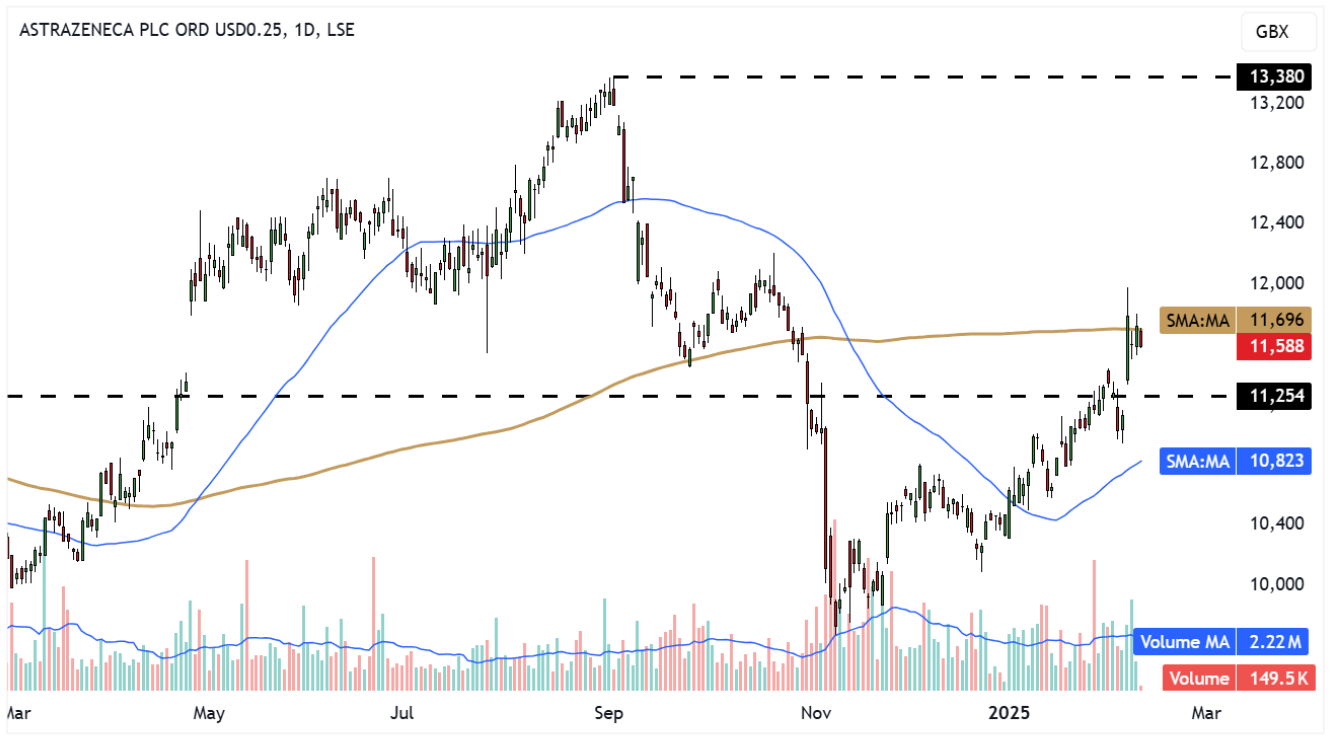

AstraZeneca rides strong sales growth despite China woes

AstraZeneca (AZN) delivered an 18% jump in fourth-quarter revenue, beating analyst expectations despite a decline in sales in China and the arrest of its top executive in the country.

The pharma giant reported $14.9bn in quarterly sales, surpassing forecasts of $14.2bn, while core earnings per share came in at $2.09. Investors welcomed the results, pushing shares up as much as 5% in early London trading. Looking ahead, AstraZeneca expects revenue to grow at a high single-digit rate in 2025, with core earnings per share rising by a low double-digit percentage.

The company’s troubles in China remain a key challenge. Sales in the country fell 3% in the quarter, impacted by a mild winter reducing demand for respiratory drugs and budget caps at Chinese hospitals. AstraZeneca is also under investigation over suspected unpaid import taxes of $900,000, which could lead to a fine of up to $4.5mn. Meanwhile, the arrest of former China head Leon Wang in October, as part of a broader crackdown on the healthcare sector, has added further uncertainty. AstraZeneca has since appointed Iskra Reic to lead its China operations, aiming to stabilise its position in the market.

Despite these headwinds, AstraZeneca remains focused on long-term growth. CEO Pascal Soriot highlighted the company’s strong 2024 performance and pointed to upcoming late-stage trial results for seven new medicines. The firm plans to increase capital investment by 50%, boosting manufacturing and IT infrastructure, while raising its annual dividend to $3.20 per share. However, AstraZeneca’s UK operations faced a setback after scrapping plans for a £450mn vaccine plant due to a lack of government support. While challenges persist, the company remains committed to expansion, particularly in China, where it sees significant long-term potential.

AZN Daily Candle Chart

Babcock surge on Q3 update and full-year expectations upgrade

Babcock International (BAB) saw its shares gap significantly higher last week following the release of an impressive Q3 trading update which included an upgrade to its full-year expectations for FY25.

The company’s strong performance during the first half of the financial year continued into the third quarter, with positive preliminary results for January further boosting investor confidence. The Board has now revised its revenue forecast to approximately £4.9 billion, driven by double-digit organic growth in Nuclear and significant expansion in the Marine sector. This upgrade reflects a solid execution of the company’s strategy, which is yielding impressive results.

The Nuclear division is a major driver of growth, benefiting from increased activity in civil nuclear new builds and decommissioning, as well as a rise in submarine support and infrastructure revenues. The Marine sector has also seen strong performance, buoyed by higher volumes in Large Government Equipment (LGE) and the ramp-up of the Skynet programme. These factors have collectively propelled Babcock to exceed the top end of analyst revenue and profit expectations for the year. The company’s strategic focus and operational excellence continue to attract strong demand for its engineering services both in the UK and internationally.

Notable recent developments include Babcock’s progress on critical defence projects. In January, HMS Victorious entered the 9-Dock facility at Devonport as part of a £560 million programme to modernise and refit the submarine, which plays a crucial role in the UK’s national defence. Additionally, Babcock is advancing the Type 31 Inspiration Class frigate programme and has secured a new 17-year contract with the French government for military air training solutions, marking a significant expansion of its operations in France. These developments underline Babcock’s growing portfolio of strategic contracts and reinforce its position as a leader in defence and engineering services.

BAB Daily Candle Chart

BP rally following on Elliott Investment stake amid challenging results

BP (BP.) shares jumped on Monday following the news that activist investor Elliott Investment Management has taken a stake in the oil giant, although the exact size of the holding remains undisclosed.

Elliott is reportedly pushing for transformative actions to unlock shareholder value, citing BP’s current undervaluation, with the company’s market cap standing at £69 billion—less than half of rival Shell’s. The announcement comes on the back of BP’s mixed financial results for Q4 and the full year of 2024, which highlighted significant challenges in its downstream and refining sectors. The company reported a $2.0 billion loss for Q4, a stark contrast to the $0.4 billion profit reported in the same period in 2023. This was largely due to lower refining margins, weaker oil trading performance, and higher asset impairments.

Despite these setbacks, BP showed resilience, with an underlying replacement cost profit of $1.2 billion for Q4, bolstered by strong performance in its gas, low-carbon energy, and oil operations. The company’s operational focus and higher realisations helped mitigate the impact of weaker refining results. BP also announced a 10% increase in its dividend, with an 8-cent dividend per ordinary share, signalling continued shareholder returns despite the tough quarter.

Looking ahead to 2024, BP is placing a strong emphasis on restructuring its business and investing in high-potential projects, such as offshore wind partnerships and a gas joint venture. Alongside these efforts, the company has been focused on cutting costs, achieving $0.8 billion in structural savings, and maintaining capital discipline with a $1.75 billion share buyback program. These moves are seen as key steps in addressing the challenges faced in 2024 and positioning BP for long-term growth.

BP. Daily Candle Chart

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.