14th Aug 2024. 9.05am

Regency View:

Update

Regency View:

Update

Aviva sees 14% profit surge amid UK economic stability

Aviva (AV.) reported a 14% rise in first-half adjusted operating profit to £875 million, driven by strong performance in its general insurance business, where premiums increased by 15% to £6 billion. This growth was supported by better underwriting in the UK and Ireland.

The company’s CEO, Amanda Blanc, emphasised that the “greater economic stability and political certainty” in the UK is making it a more attractive market for investment and growth. Aviva is maintaining strong pricing discipline in an inflationary environment, especially in home and motor insurance.

Assets under management in Aviva’s wealth business grew to £186 billion, thanks to higher net inflows compared to the first half of last year. However, sales in its retirement division saw a slight decline, with bulk annuity sales dropping from £2.4 billion to £2.3 billion. Despite this, Aviva remains on track to meet its three-year target of £15 billion to £20 billion in deals.

The company’s capital coverage ratio under Solvency II was 205%, slightly lower than at the year-end but still ahead of expectations. Analysts anticipate earnings upgrades following these strong results, with Citigroup and Jefferies noting the company’s robust performance.

In addition, Aviva’s investment management business agreed to sell a portfolio of 32 UK wind farms to a consortium led by Hong Kong’s CK Infrastructure, further demonstrating the company’s strategic moves in the market.

AV. Daily Candle Chart

Barclays deliver strong results

Barclays (BARC) released a strong set of results at the turn of the month, showcasing notable achievements despite a 9% decline in profit for the first half of 2024. This decrease, while significant, was less severe than many had feared, largely due to the bank’s impressive performance in certain areas, particularly within its investment banking division.

A standout feature of Barclays’ results was the remarkable success of its investment banking sector. The bank saw a substantial 24% increase in equities revenue during the second quarter. This growth in trading income played a crucial role in offsetting the decline in overall profits and highlighted the strength of Barclays’ trading operations. This performance in equities was especially noteworthy when compared to other major banks, surpassing the gains reported by rivals such as Morgan Stanley, Goldman Sachs, and JPMorgan.

In addition to the strong trading results, Barclays also announced a substantial share buyback program of £750 million ($957 million) and revised its long-term earnings guidance upward. The bank now expects to achieve a return on tangible equity (ROTE) greater than 12% by 2026, an improvement over its previous target of 10% for 2024. Barclays also raised its forecast for annual income to £30 billion by 2026 and committed to returning at least £10 billion to shareholders through dividends and buybacks between 2024 and 2026.

Despite these positive developments, the bank faced challenges in its UK retail banking sector and corporate banking operations. The return on tangible equity for its UK corporate bank dropped significantly, and revenues in the UK retail bank fell by 4%. These declines were attributed to increased competition in lending and adverse dynamics in deposit rates.

BARC Daily Candle Chart

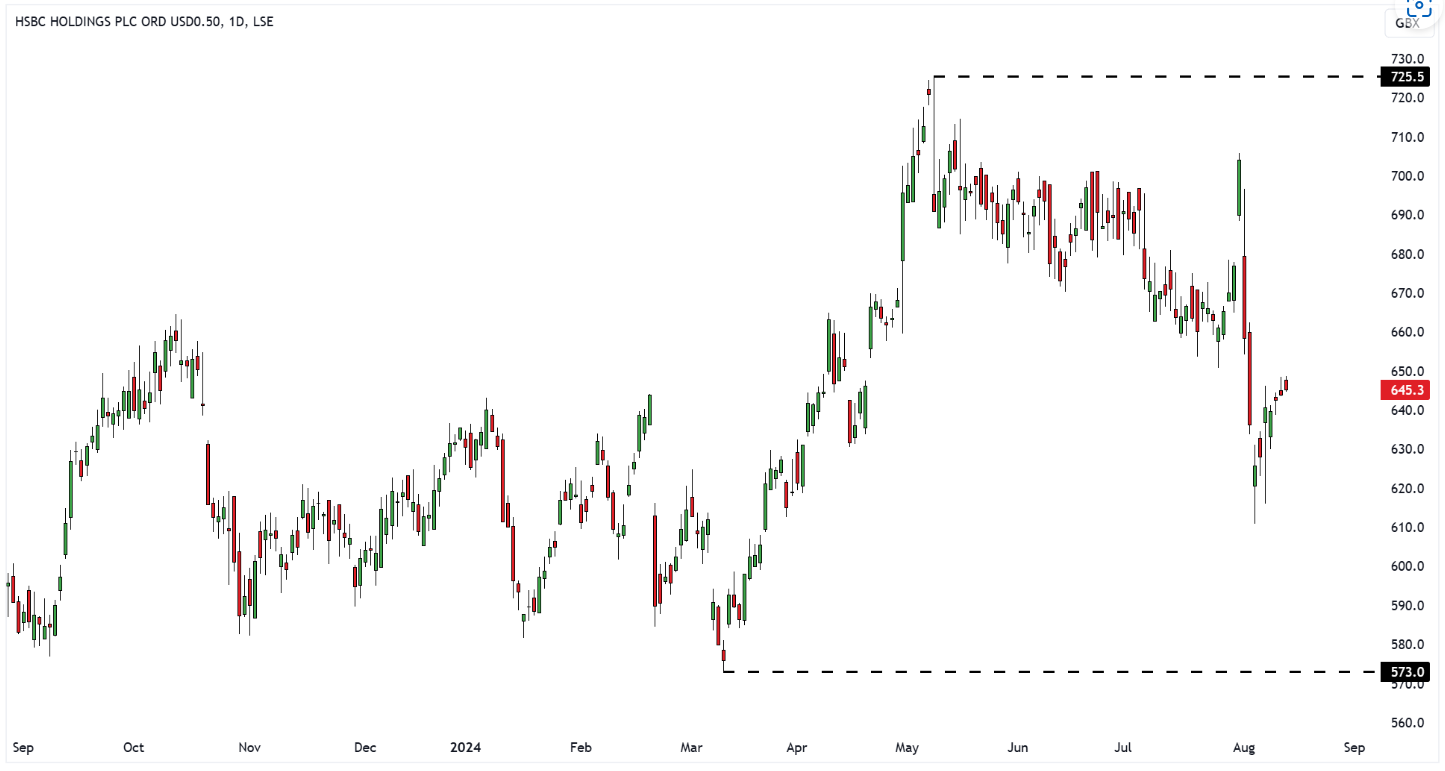

HSBC announce $3bn buyback

Just prior to the global stock sell-off at the start of the month, HSBC (HSBA) released a strong set of interim results, which caused the bank’s shares to jump higher at the end of July.

HSBC reported a robust 12% increase in wealth management revenue, signalling strong performance in its private banking and asset management divisions. The bank’s pretax profit for the first half of 2024, although slightly down by 0.4% to $21.6 billion, surpassed market expectations, reflecting resilience in its core operations amidst global economic uncertainties.

In addition, HSBC’s announcement of a $3 billion share buyback program and an upgraded income forecast for 2024 were significant drivers of the share price increase. The buyback, coupled with the bank’s new target for return on average tangible equity in the mid-teens by 2025, underscored its commitment to delivering shareholder value and growth.

These positive results, along with a decrease in HSBC’s sensitivity to global interest rate cuts due to effective hedging strategies, contributed to a surge in its share price as investors responded favourably to the bank’s strong financial performance and strategic initiatives.

However, this optimistic momentum was short-lived as a broader global stock sell-off at the beginning of the month began to affect market sentiment. The sell-off, driven by a variety of macroeconomic and geopolitical factors, eventually overshadowed HSBC’s strong interim results, leading to a reversal in the bank’s share price gains.

HSBA Daily Candle Chart

Smith & Nephew’s Q2 results hit the right notes

Smith & Nephew (SN.) released a solid set of Q2 results at the start of this month, demonstrating strong performance across several key metrics.

For the second quarter ending 29 June 2024, the company achieved a revenue of $1.441 billion, reflecting a 5.6% increase on an underlying basis compared to the same period last year.

The revenue growth was driven by robust performances across all business units. In Orthopaedics, revenue grew by 5.8%, supported by improvements in Hip and Knee Implants outside the US and progress in other areas such as Trauma & Extremities. The Sports Medicine & ENT division saw a 7.6% increase, with strong growth across all segments despite the ongoing impact of China’s sports medicine Value-Based Purchasing (VBP) program. Advanced Wound Management also showed a 3.3% revenue increase, marking a return to growth with contributions from all segments.

In terms of profitability, Smith & Nephew reported an operating profit of $328 million for the quarter, up 19.5% year-over-year, reflecting enhanced efficiency and productivity. The trading profit margin expanded to 16.7%, exceeding the top end of the company’s guidance range, driven by positive operating leverage.

The company’s cash flow also saw a significant improvement, with $368 million generated from operations, compared to $215 million in the previous year. Trading cash flow surged to $284 million, up from $110 million, and the trading cash flow conversion rate improved to 60% from 26% last year, highlighting the company’s enhanced cash generation capabilities.

Earnings per share (EPS) for the quarter reached 24.5 cents, marking a 24.6% increase from the previous year, driven by improved profitability and operational efficiencies. Overall, the results underscored Smith & Nephew’s continued progress and we’re more than happy to continue to hold the stock in our list of FTSE Investor open positions.

SN. Daily Candle Chart

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.