26th Jul 2023. 8.57am

Regency View:

Update

Regency View:

Update

Aviva posts strong first half and announces Barclays home insurance tie-up

Aviva (AV.) recently revealed an impressive trading update, forecasting a robust performance in the first half of 2023.

The insurance giant expects an operating profit of approximately £700m during this period, with a promising outlook for the full year, projecting a 5-7% year-on-year profit growth.

In a significant development, Aviva also finalised a groundbreaking agreement with Barclays UK. The deal entails the acquisition of Barclays’ home insurance portfolio, which currently serves a considerable customer base of 350,000 policyholders.

This strategic move bolsters Aviva’s vision of expanding its retail insurance business and cementing its dominant position in the fiercely competitive home insurance market.

The market has enjoyed Aviva’s recent newsflow and the shares have started to build some bullish momentum over the last two weeks.

AV. Daily Candle Chart

Experian reports strong revenue growth despite market challenges

In a trading update released earlier this month, Experian (EXPN) said revenue for the first-quarter of its financial year jumped 5% – in-line with market expectations.

The revenue growth was not confined to specific regions; instead, it showed a broad-based expansion across geographies. Latin America particularly stood out, with a substantial increase in its free membership base, reaching an impressive 95m. Businesses in the region also embraced Experian’s suite of data tools, contributing to overall growth.

However, Experian faced challenges in North America, primarily due to the recent turmoil in the global banking industry. The closure of regional banks and the failure of a major bank shook consumer confidence in the sector, adversely impacting lending volumes and credit demand. Despite these obstacles, Experian managed to offset the downturn by gaining contributions from buy-now-pay-later clients and witnessing a rise in the free membership base, which reached 64m.

In the UK, lenders exercised caution in light of soaring inflation, leading to repricing and reduced credit supply in specific categories. Nevertheless, Experian’s UK and Ireland revenue demonstrated resilience, still achieving 1% growth during the first quarter through June.

Looking ahead, Experian maintains a positive outlook and reaffirms its expectation of organic revenue growth in the range of 4% to 6%.

EXPN Daily Candle Chart

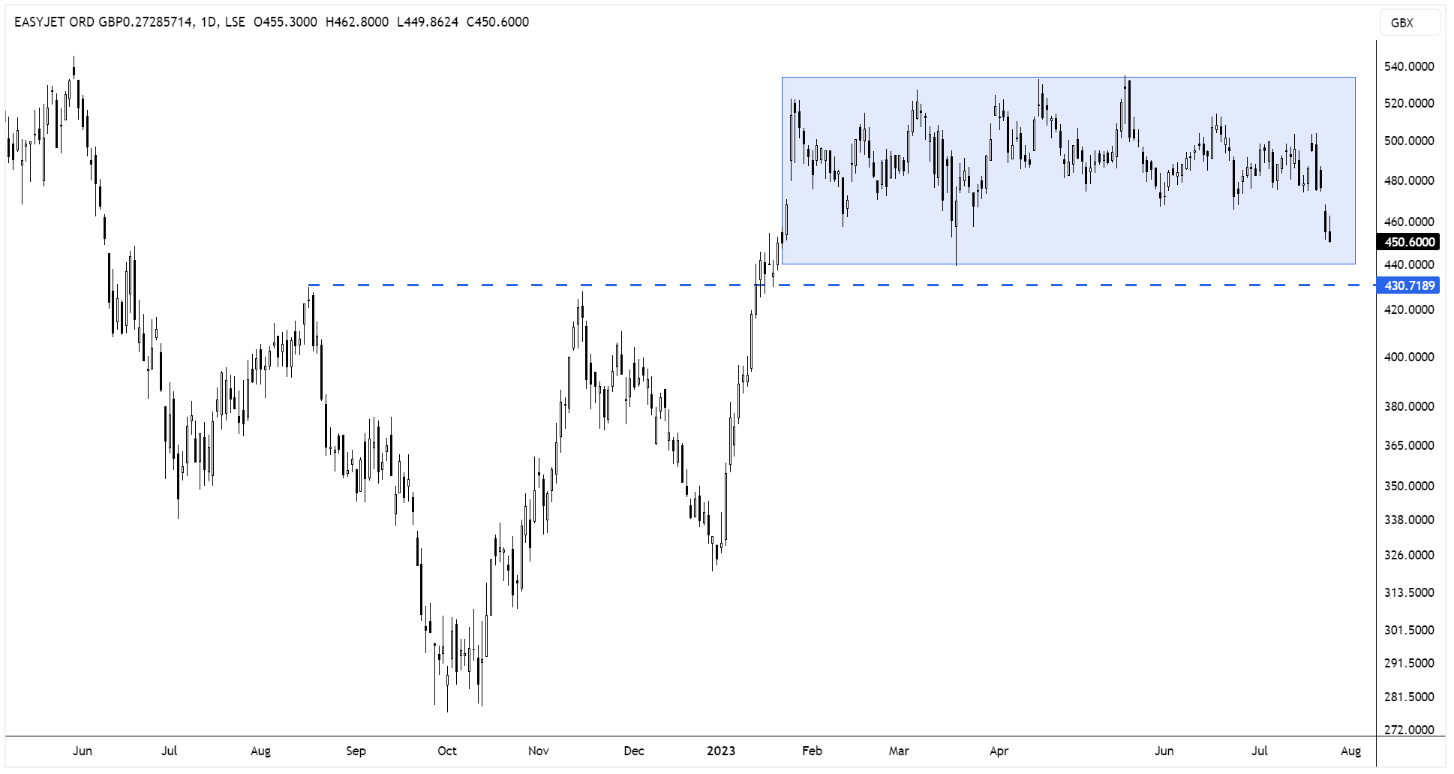

EasyJet report record profits amidst air traffic turbulence

EasyJet (EZJ) has reported record pre-tax profits of £203m for the three months to end June, a significant improvement from a loss of £114m in the same period last year.

The surge in profits is attributed to high ticket prices and strong demand for travel, which has remained unaffected by the weak economy.

The budget airline expects to achieve another record pre-tax profit in the current quarter ending in September. However, it warns that its performance is dependent on navigating “unprecedented” air traffic control disruptions caused by the closure of around 20% of Europe’s airspace following Russia’s invasion of Ukraine, as well as air traffic control staff shortages and strikes.

Looking ahead, EasyJet has seen promising booking momentum for the winter, indicating that the demand for travel is expected to continue beyond the current summer period.

The airline is also in the process of securing new planes to replace some of its older aircraft, demonstrating its commitment to modernisation and growth.

On the price chart, the shares continue to chop sideways within a well-defined trading range. A positive reaction to Easyjet’s trading update has been offset by downbeat comments from Ryanair CEO about the global macroeconomic picture.

EZJ Daily Candle Chart

Glencore forecasts strong growth for second half of 2023

Glencore’s (GLEN) CEO, Gary Nagle, reported a solid first-half production performance for their key assets in copper, coal, and zinc, which met expectations and previous guidance.

The second half of 2023 is expected to see increased production volumes from Collahuasi, Kazzinc, Mount Isa, and INO.

In the first half of 2023, copper production was 4% lower than the same period in 2022 due to mining sequences at Collahuasi and Antamina, as well as lower copper by-products outside the Copper department. However, cobalt production increased by 5% compared to H1 2022, driven by improved recoveries at Katanga.

Zinc production, on the other hand, decreased by 10% from H1 2022, mainly due to the disposal of South American zinc operations and the closure of Matagami. Nickel production also declined by 20% from H1 2022, primarily due to higher INO third-party production necessitated by the strike at Raglan mine in 2022. Coal production remained largely unchanged from H1 2022.

The full-year production guidance remains unchanged from earlier projections. For the year, Glencore expects to produce approximately 1,040 ± 30 kt of copper, 38 ± 5 kt of cobalt, 950 ± 30 kt of zinc, 112 ± 5 kt of nickel, 1,310 ± 30 kt of ferrochrome, and 110 ± 5 mt of coal.

GLEN Daily Candle Chart

Moneysupermarket’s insurance division surges

Moneysupermarket (MONY) reported its interim results this week, highlighting steady growth with robust margins and strong cash generation.

During the six months leading to June, the insurance and travel divisions performed exceptionally well, while the money and home services businesses faced constraints due to rising interest rates and volatile energy markets.

The housing market was impacted by rising mortgage rates, resulting in a 2% decline in revenue (£52m) for the money division, as fewer individuals were interested in moving or refinancing. Additionally, the volatile energy market kept prices close to the capped level, causing a 1% decrease in home services revenue.

On the bright side, the insurance business, accounting for 49% of revenue, thrived amidst the squeeze on mortgages and energy prices. Households on tight budgets actively sought better deals, leading to an impressive 23% increase in revenue for the insurance division.

Moneysupermarket demonstrated effective cost management, with operating costs rising by only 3%. This efficiency boost raised the operating margin from 22.7% to 26%, allowing for a 3% increase in the half-year dividend.

MONY Daily Candle Chart

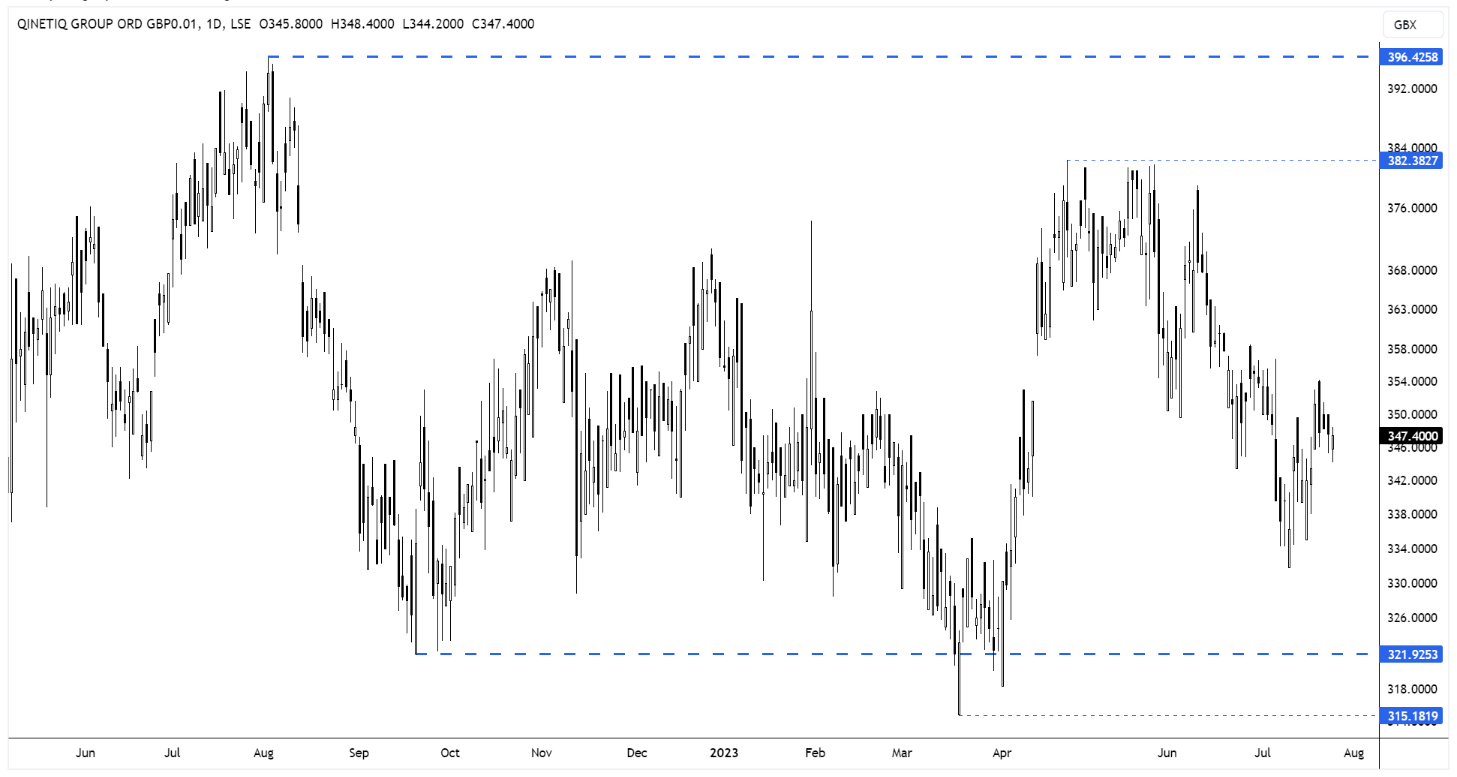

Qinetiq on track after strong first quarter

Qinetiq (QQ.) announced a positive quarterly trading update in which it said it was on track to meet expectations.

The defence tech company said order intake remains strong, and revenue, profit, and cash performance are satisfactory. The visibility on revenue under contract for 2024 rose to £1.3bn, up from £1.1bn in April, reinforcing their confidence in meeting full-year expectations.

Steve Wadey, the CEO, emphasised the continued importance of defence and security due to the global security situation:

“We continue to see a significant opportunity from the widening threat spectrum, with our six distinctive offerings well aligned to areas of the defence and security budgets where greatest priority and funding is being directed, such as experimentation and technology, cyber and information advantage, and training and mission rehearsal.”

Among their key business wins during the quarter, Qinetiq secured a notable $40m research and engineering contract from the Prototypes and Experiments Director for the Under Secretary of Defence for Research and Engineering in the US.

Additionally, QinetiQ won a £38m contract extension with Defence Digital in the UK, and they have an impressive $86m backlog on their Joint Adversarial Training and Testing Services contract in Australia.

The company’s Global Products segment is being renamed Global Solutions due to the increasing focus on high-value services compared to traditional products. Qinetiq’s performance momentum in the US is strong, integration activities are on track, and progress is being made on new business opportunities. And the EMEA Services segment continues to perform well across all metrics.

QQ. Daily Candle Chart

Ten Entertainment well set to meet market expectations

Ten Entertainment Group (TEG) reported steady growth in their half-year trading update with like-for-like sales up +1.6% compared to the same period in 2022 and sales now 57% higher than pre-Covid levels.

The bowling company expects pretax profit for H1 2023 to be slightly ahead of last year, even without the benefits from reduced rate VAT and business rates relief.

TEG managed cost pressures effectively, offsetting labour inflation through operational and supplier efficiencies. They also benefit from secure, low electricity prices until September 2024, and have signed a new deal securing renewable energy with price certainty until September 2026.

TEG foresees low single-digit sales growth for the rest of 2023, aiming to meet market consensus for full-year profits. The company plans to open new centres and introduce innovative games and activities.

CEO Graham Blackwell said:

“We are well set to continue to drive profitable growth in the second half of the year and to meet market expectations.”

The shares are consolidating in a tight range near recent highs and this indicates that TEG’s long-term uptrend will continue.

TEG Daily Candle Chart

Unilever beats sales expectations as CEO signals confidence in peaking inflation

Unilever (ULVR) reported better-than-expected sales growth in the first half of the year.

The consumer goods giant said underlying sales increased by 9.1%, surpassing analysts’ expectations. However, sales volumes remained flat, and Unilever faced a decline in market share.

Outgoing CFO, Graeme Pitkethly, stated that inflation had peaked, but price rises would still contribute to sales growth in the second half of the year. Unilever increased prices by 9.4% in the first half, lower than the 13.3% increase in the previous three months.

Price increases led to a decrease in the company’s volumes, with Europe being particularly affected due to a broad-based increase in private market share and consumers buying less and down-trading.

Despite these challenges, Unilever’s Q2 results exceeded sales growth forecasts, mainly due to the company raising prices to offset higher costs. Unilever’s new CEO, Hein Schumacher raised the consumer goods giant’s revenue growth forecast for the year to more than 5%.

The market cheered the update and Unilever’s share price gapped higher on Tuesday, making further gains throughout the session. This burst of bullish price momentum should lead to a retest of trend highs – an area we may look at to take some profit.

ULVR Daily Candle Chart

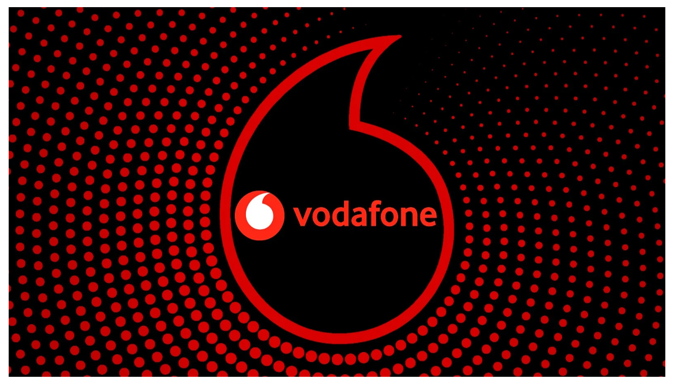

Vodafone reports better than expected quarterly numbers

It’s been a long time coming, but Vodafone (VOD) have finally reported some positive newsflow…

The troubouled telecom giant has reported better than expected quarterly service revenues. Group service revenue, which includes sales from contract payments, network use, and roaming, rose 3.7% to €9.1bn in the three months to June 30, outperforming the average estimate of 2.9%.

This growth was driven by higher prices in its home market and increased customer numbers. The group’s enterprise division, which provides cloud and cyber security services to companies, also contributed to the revenue boost.

However, Vodafone faced a challenge in its biggest market, Germany, where service revenue declined for the fifth consecutive quarter. Though the decline narrowed to 1.3%, reaching €2.8bn, thanks to a broadband price increase, it resulted in a loss of more than 120,000 customers for broadband services.

Despite this, Margherita Della Valle, the new chief executive who took over in April, expressed confidence in the gradual improvement of service revenue performance in Germany, acknowledging there is more to be done in the overall turnaround of the company.

VOD Daily Candle Chart

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.