3rd May 2023. 8.59am

Regency View:

Update

Regency View:

Update

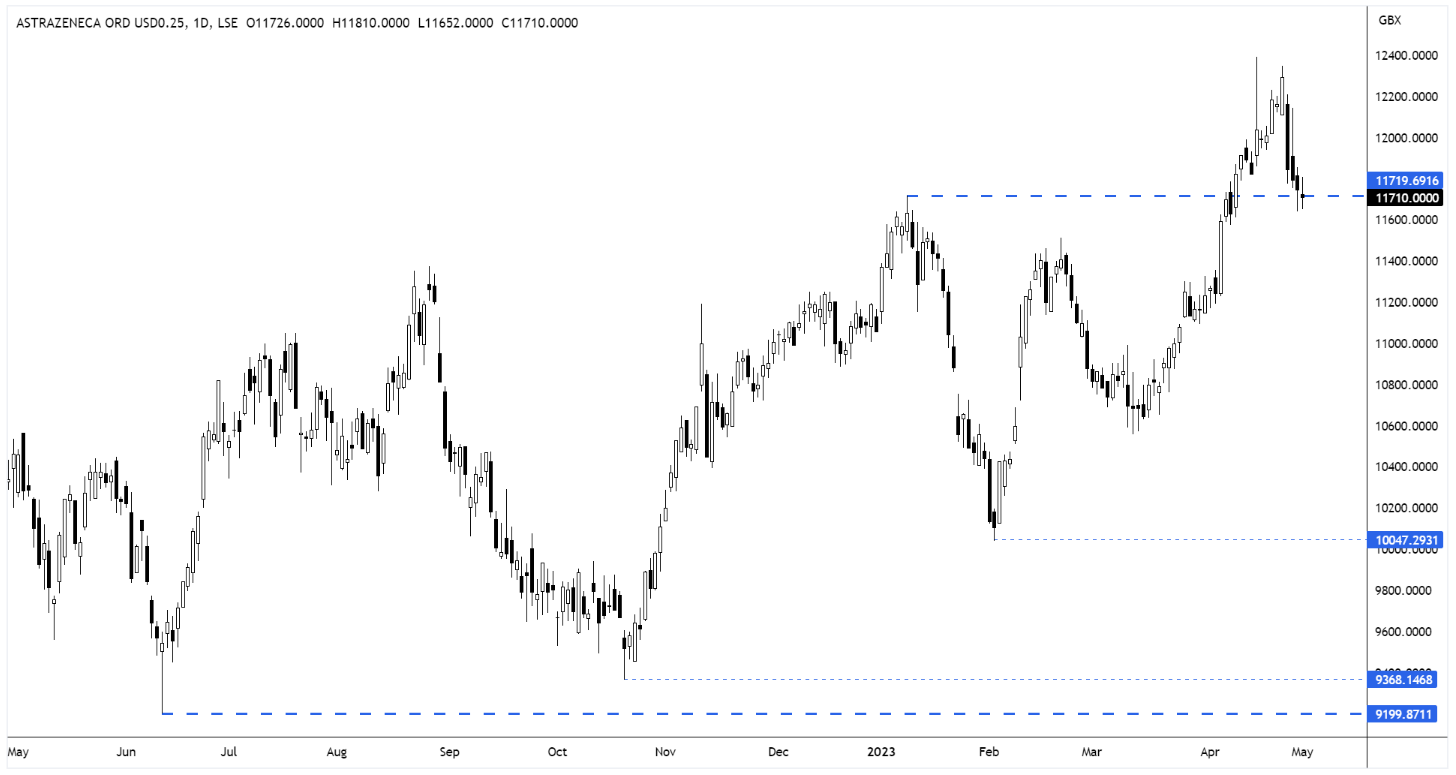

AstraZeneca beats estimates on strong emerging market sales

AstraZeneca (AZN) beat expectations for first-quarter profit and revenue, as buoyant sales of cancer treatment Imfinzi and strong demand for its roster of drugs in emerging markets helped to offset dwindling COVID product sales.

The pharma giant’s cancer drug, Imfinzi generated $900m revenue in Q1, comfortably beating estimates market expectations of $735m.

And sales of its rare blood disorder drugs Soliris and Ultomiris – which it acquired via a $39bn acquisition of Alexion in 2021 – also beat expectations.

CEO Pascal Soriot said AstraZeneca’s performance in emerging markets was particularly strong.

Excluding sales of its COVID-19 products, sales rose 22% to $3.1bn in emerging markets on a constant currency basis.

However, AstraZeneca’s trading update highlighted the rapid decline of its COVID vaccine, its best-selling product in 2021 at the height of the pandemic, which has struggled to compete with rival shots developed by Pfizer and Moderna.

Sales of its COVID-19 vaccine dropped to $28m in the first quarter, versus $1.14bn over the same period last year, as the company lost ground to rival mRNA vaccines.

The market’s tepid reaction to the numbers indicates that the strong performance in emerging markets was priced in. The shares have now pulled back to an area of broken resistance, which we would expect to provide support moving forward.

AZN Daily Candle Chart

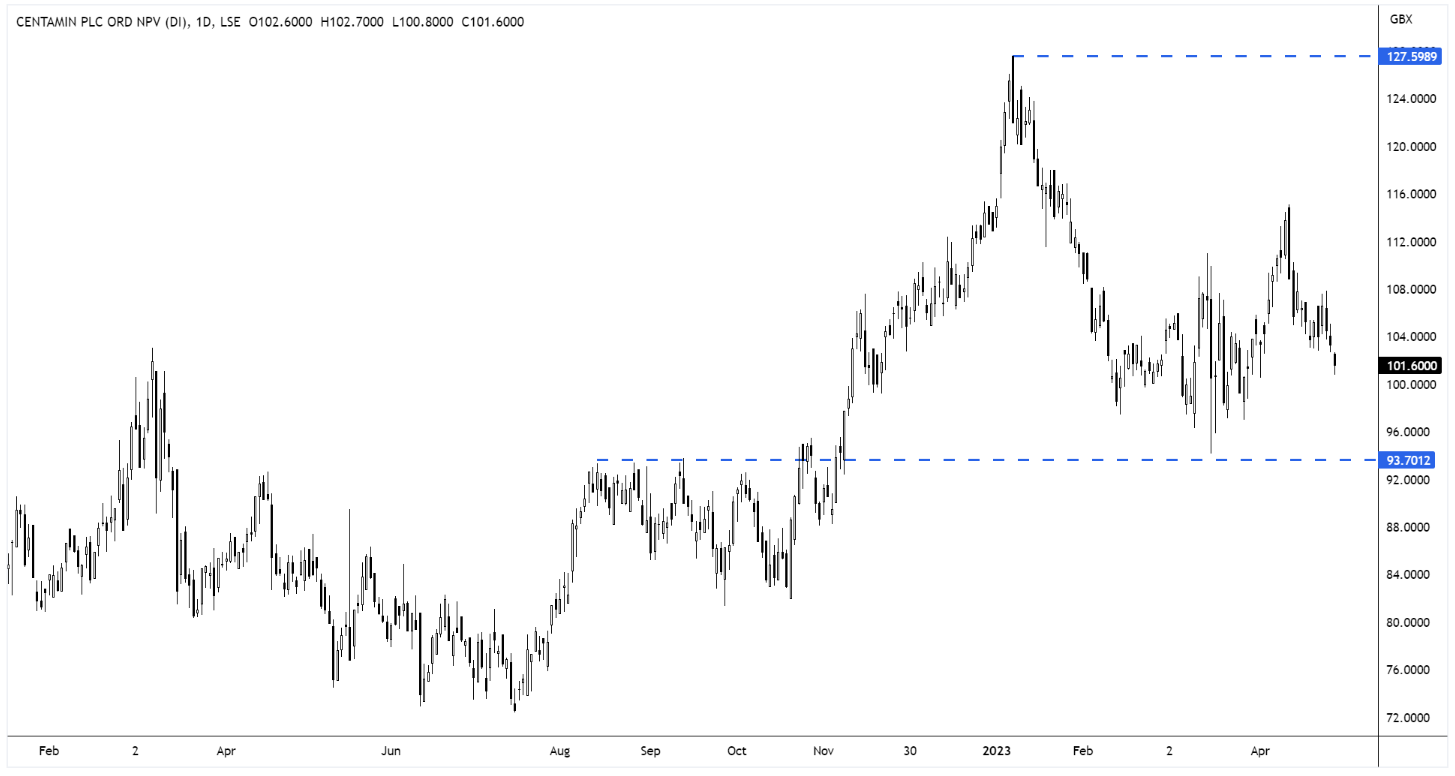

Centamin release ‘in-line’ operational performance

In a report released last week, Centamin (CEY) said Q1 gold production from the Sukari Gold Mine was 105,875 ounces (oz).

Revenue for the quarter came in at $205 million, an 18% increase from Q1 2022, generated from gold sales of 107,661 oz at an average realised gold price of US$1,902/oz sold.

Q1 cash costs were US$937/oz produced and all-in sustaining costs (AISC) were US$1,348/oz sold.

CEO Martin Horgan said:

“We reiterate our 2023 guidance and look forward to reporting later in the year on several additional projects which will deliver growth and underpin returns. These include connecting Sukari to the grid which will reduce carbon emissions and save costs, publishing an optimised Sukari life of mine plan, commencing drill testing on our Egyptian Eastern Desert blocks and completing the PFS at our advanced Doropo Project in Côte d’Ivoire.”

Centamin kept gold production guidance unchanged at a range of 450,000 to 480,000 oz per annum weighted towards the second half of the year.

CEY Daily Candle Chart

Glencore to pay Norsk Hydro $700m for Brazilian assets

Norwegian aluminium producer Norsk Hydro said last week that it will sell a 30% stake in Brazilian alumina refinery Alunorte and a 5% stake in bauxite producer Mineracao Rio do Norte to Glencore (GLEN).

Glencore expects to pay about $700m for the equity stakes on completion of the deal in the second half of 2023, it said in a separate statement.

The transaction value is based on a total net enterprise value of $1.11bn, which will be adjusted for net debt of about $335m.

“The growing decarbonisation trend is driving demand not only for the mass production of batteries that require the raw materials which Glencore produces, but also for primary aluminium as a strong, lightweight manufacturing metal” said Robin Scheiner, Glencore’s head of alumina and aluminium.

This deal comes on the back of Glencore’s bid for Teck resources and further highlights Glencore’s plans to build its ‘decarbonisation metals’ portfolio and spin out its coal assets.

GLEN Daily Candle Chart

HSBC jump on $2bn share buyback as higher interest rates boost earnings

HSBC (HSBA) announced plans to buy back up to $2bn of its stock in a bid to shore up investor support amid rising pressure from Ping An, its largest shareholder.

Q1 pre-tax profits jumped to $12.9bn, more than three times the figure from a year earlier and beating analysts’ expectations for $8.6bn.

The surge in profits was partly due to a provisional gain of $1.5bn from its £1 rescue of the UK arm of collapsed lender Silicon Valley Bank (SVB) in March.

HSBC also reversed $2.1bn of impairments linked to the planned sale of its French retail banking network to the private equity firm Cerberus.

Alongside the share buyback, HSBC also said it would return to making its dividend payouts every quarter, meeting a key demand of its Hong Kong retail investor base.

HSBC set the payout at 10 cents a share and said it planned to pay a special dividend once the $10bn sale of its Canadian business closes next year.

“Our strong first quarter performance provides further evidence that our strategy is working” said CEO Noel Quinn.

“Our profits were spread across our major geographies, and all three global businesses performed well as we continued to meet our customers’ needs through our internationally connected franchises” he added.

HSBA Daily Candle Chart

Indivior lifts revenue guidance, cuts profit outlook after Opiant deal

Opioid addiction treatment maker Indivior (INDV) lifted its full-year revenue guidance but trimmed its outlook for operating profit due to costs related to the acquisition of Opiant Pharmaceuticals.

Indivior saw net revenue rise up 22% to $253m in the first quarter, while adjusted operating profit jumped 31% at $71m.

The company lifted its full-year net revenue guidance to between $970m and $1.04bn, from previous guidance of $950m to $1.02bn.

However, its outlook for adjusted operating profit was reduced to “slightly below” FY 2022’s adjusted operating income of $212m, as a result of the additional operating expenses associated with the Opiant acquisition.

Indivior CEO, Mark Crossley said:

“SUBLOCADE injection continues to power our growth as we drive greater depth of prescribing across Organized Health Systems (OHS) in the treatment of moderate-to-severe opioid use disorder (OUD)”.

Indivior’s strong numbers are still clouded by the uncertainty surrounding US legal action in relation to its control of the US market.

INDV Daily Candle Chart

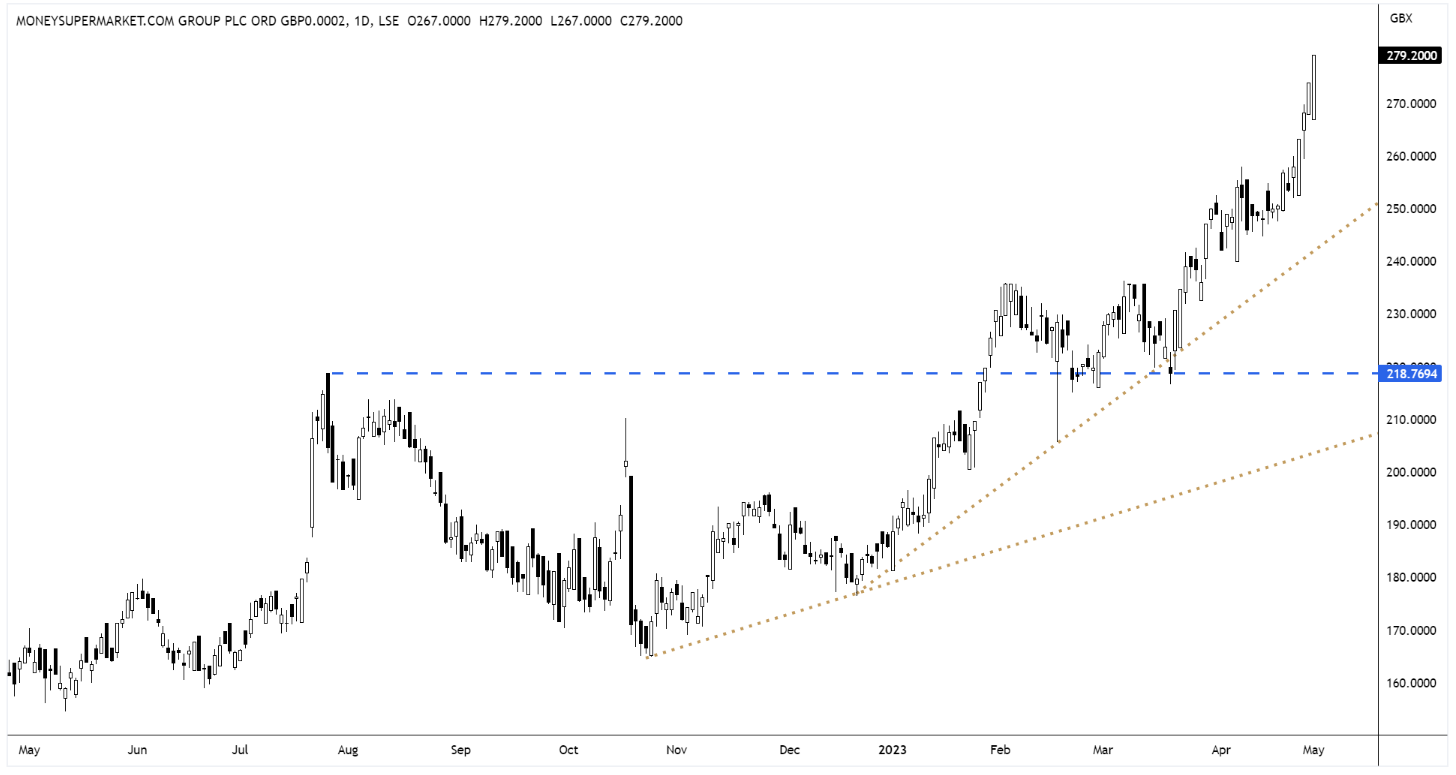

Moneysupermarket gets travel boost in first quarter

Moneysupermarket.com (MONY) revealed robust revenue growth for the first quarter following a strong recovery in travel and insurance.

The price comparison site said it was “confident” of meeting market forecasts for this year as total revenue jumped 15% to £106.3m in the first quarter.

Insurance revenue grew by 23% to £50.6m, with car insurance showing a strong recovery after new FCA pricing regulations for general insurance impacted the market last year.

Revenue from the group’s Travel business surged by 63% to £5.4m in the period, with travel insurance around 50% higher than pre-pandemic 2019 levels.

While revenue in its Money division came in at £26.9m, showing growth of 9%, driven by promotional offers in banking.

“This is a strong performance led by recovery in Insurance and Travel,” said chief exec, Peter Duffy.

“Our strategy of making it easier for people to save on more of their bills is going well and means we’re helping consumers cope with cost of living pressures” he added.

MONY Daily Candle Chart

Morgan Advanced Materials hikes dividend despite damaging cyber attack

Morgan Advanced Materials (MGAM) raised its dividend by 31.9% to 12.0p per share on the back of a 24.3% jump in adjusted earnings per share.

The payout hike was declared despite a damaging cyber attack in January.

Morgan’s CEO, Pete Raby said:

“As previously announced, the cyber event we experienced in January has impacted sales and profitability in the short term, but our recovery is on track. We are also taking the opportunity to accelerate the modernisation of our IT infrastructure”.

On the group’s full-year outlook he added:

“As a consequence of the cyber incident, we expect revenue in our first half to be in line with prior year, whilst experiencing temporary cost inefficiency as previously highlighted. In the second half, we expect to return to growth, with growth and margins in line with our financial framework. Outlook for full year adjusted operating profit is unchanged from our guidance of 7 February 2023.”

After a sharp drop in January, Morgan’s share price has started to fight back and prices are within touching distance of its pre-cyber attack highs.

MGAM Daily Candle Chart

Rentokil rally on Q1 trading update

Rentokil’s (RTO) share price was given another boost last month following the release of an impressive set of Q1 numbers.

The global pest control behemoth said the year had “started well”, with reported revenue up 64.5%, reflecting the benefit of its Terminix acquisition along with “strong” organic revenue growth of 6.7%.

All regions and divisions saw solid levels of organic revenue growth with North America Pest Control up 4.9%, driven by strong demand from commercial, residential, and termite customers.

Commenting on the trading update, CEO Andy Ransom reiterated full year guidance:

“I am delighted with the performance our colleagues delivered in Q1, which demonstrates the resilience of our compounding growth model and continued strategy execution. This performance, combined with further progress in our value-creating M&A programme led by the integration of Terminix, means we are well positioned for the remainder of the year. We reiterate our 2023 full year expectations.”

RTO Daily Candle Chart

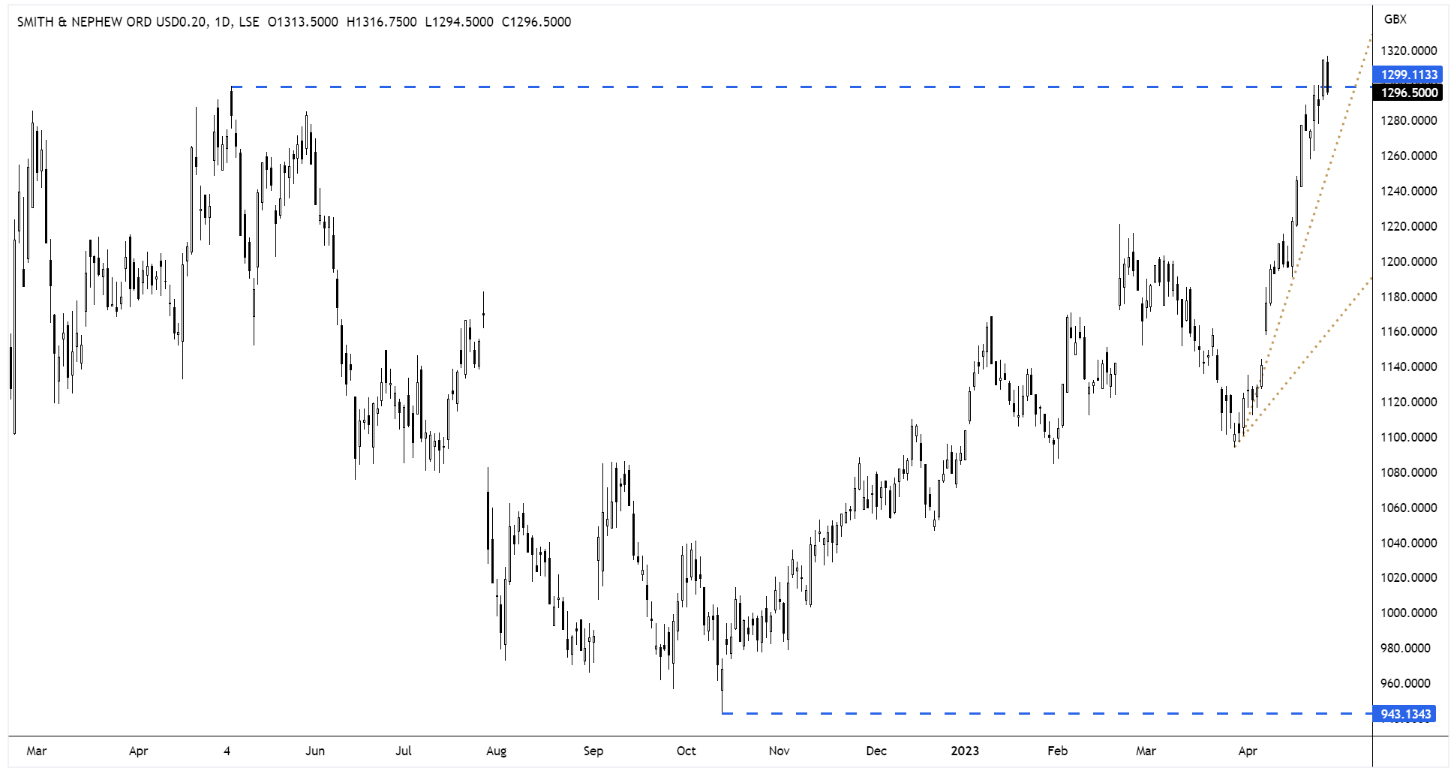

Smith & Nephew delivers in-line trading statement

Smith & Nephew’s (SN.) share price has continued its strong recent run after releasing a solid set of quarterly numbers.

The medical equipment manufacturing company said strong growth in its Sports Medicine and Advanced Wound Management businesses had underpinned a 3.8% improvement in first-quarter revenue.

Smith & Nephew said underlying revenue in Sports Medicine & ENT rose 10.0%, in Advanced Wound Management by 7.9% and in Orthopaedics by 3.9%.

Chief Exec Deepak Nath said he was pleased with the group’s revenue performance in the first quarter and the “accelerated adoption of robotics” added further differentiation to Smith & Nephew’s platform.

“We are still in the early phases of the two-year life-cycle of our 12-Point Plan and are focused on driving transformation” he added.

Smith & Nephew left its financial year 2023 guidance unchanged – management are targeting 5% to 6% underlying revenue growth and a trading profit margin of at least 17.5%.

SN. Daily Candle Chart

Unilever sees strong start to the year

Unilever (ULVR) has had a “good start to the year, delivering another quarter of strong topline growth” said CEO, Alan Jope.

Underlying sales growth accelerated to 10.5%, driven by price growth in response to continued high input cost inflation and an improved volume performance.

“Growth was broad-based across the five Business Groups, underpinned by strong performances from our €1 billion brands” Jope added.

Unilever’s sales volumes recovered more strongly than expected from a 3.6% drop in the previous quarter and were flat year on year. Sales held up better in the Americas — where they ticked up 0.6% — than in Europe, where they fell 3%.

Management expect underlying sales growth for the full year 2023 to be “at least at the upper end of our multi-year range of 3 – 5%”. And underlying price growth is expected to remain high in the first half and soften through the year.

Unilever’s share price reflects the business’ strong start to the year and the shares are back within touching distance of their October 2020 swing highs.

ULVR Daily Candle Chart

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.