Regency View:

Update

Teck rejects Glencore’s sweetened bid

Earlier this month we bought you news that Glencore (GLEN) had made an “opportunistic” bid to buy Canada’s Teck Resources.

Teck rejected Glencore’s initial proposal to buy the company in a $22.5 billion all-share deal and then spinoff their combined thermal and steelmaking coal businesses.

Following the initial rejection, on April 11 Glencore rejigged its bid to include a cash component for those who may not want exposure to thermal coal.

However, Teck believe the revised proposal is materially unchanged and have rejected it while they look to restructure the business.

“Now, pre-separation, is not the time to explore a transaction of this nature” Teck Chairman Emeritus Norman Keevil said in a statement.

While Glencore’s CEO, Gary Nagle told Bloomberg news that he’ll meet the Teck CEO “anywhere” to talk about the bid.

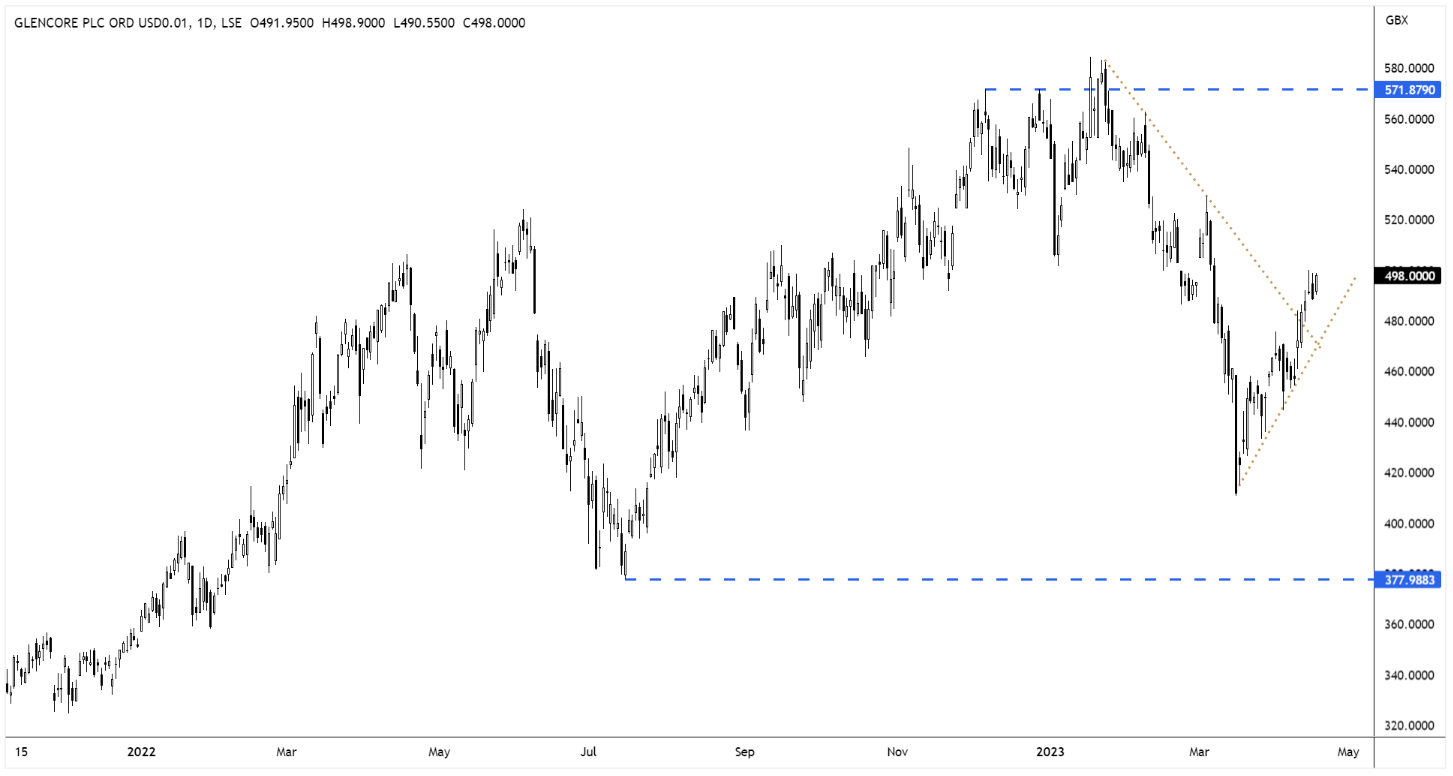

Glencore’s share price rallied on the revised bid and our open position has moved into a healthy initial profit.

GLEN Daily Candle Chart

Ping An to demand HSBC boost dividend

The FT is reporting that Chinese insurer Ping An will demand HSBC (HSBA) boost dividends to pre-Covid levels and commit to regularly reviewing its structure at its annual meeting next month.

“HSBC’s largest shareholder is planning to support resolutions proposed by a group of retail investors on dividends and structural reform, which includes spinning off operations in Asia to boost returns” said the FT.

Ping An pressure is having a positive effect on shareholder returns. HSBC set its dividend at 32 cents per share for 2022, up from 25 cents in 2021 and the highest level since 2018. It is also planning a 21 cent special dividend, worth $4bn, next year using proceeds from the sale of its Canadian business.

HSBC’s share price has rallied from a key area of broken resistance-turned support which we highlighted in previous updates. This is encouraging and we are now looking for the shares to close the gap which formed in early-March.

HSBA Daily Candle Chart

Qinetiq lifts full-year outlook

Qinetiq (QQ.) upgraded its full-year guidance this week, causing the shares to surge higher.

The pioneering defence company said it expect results for FY23 “to be ahead of previous guidance and in the upper range of market consensus expectations”.

“Following an impressive fourth quarter, full year order intake is up by 40% at a record-high of more than £1.7bn, demonstrating the continued high demand for our distinctive offerings” read the bullish trading statement.

Qinetiq expect to deliver “high-teens percentage total revenue growth” at stable margins, with underlying operating profit of at least £175m, including the benefit of the Avantus and Air Affairs acquisitions.

In addition to the robust orders, revenue and profit performance, cash flow management continues to remain “consistently strong” and Qinetiq have successfully reduced leverage to below 1x, ahead of its original guidance by 12 months.

The shares have rallied strongly from support and are now on course to retest last year’s highs.

QQ. Daily Candle Chart

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.