11th Jun 2025. 9.07am

Regency View:

BUY Sabre Insurance (SBRE)

- Income

Regency View:

BUY Sabre Insurance (SBRE)

Sabre Insurance: Where caution pays dividends

There is an old saying in insurance: you make money when you price risk well, and you lose it when you chase volume. Sabre Insurance knows exactly which side of that equation it wants to be on, and that is what makes now such an interesting time to take a position.

This is not a high-octane growth story driven by hype. Sabre plays the long game. It is a steady operator in the tough and competitive world of UK motor insurance. While premium volumes have dipped in the latest update, the story here is not about shrinking. It is about patience, discipline, and preparing for the next phase of profitable growth.

What Sabre does and how it stays competitive

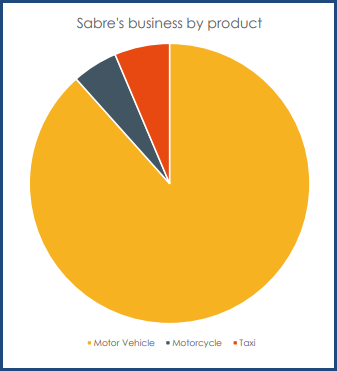

Sabre is one of the UK’s leading motor insurance underwriters with a particular focus on maintaining profitability rather than simply chasing growth. The company writes insurance policies for motor vehicles, motorcycles, and taxis, balancing a diversified portfolio that helps smooth out the inevitable ups and downs in the insurance market.

Sabre’s competitive edge lies in its disciplined, actuarially driven pricing strategy. Using a proprietary and agile pricing model refined over more than 15 years, Sabre leverages a deep dataset to price risk with precision. This allows it to avoid the pitfalls many insurers face when they underprice in soft market conditions. The company’s ability to stay disciplined on pricing means it protects margins and sustains profitability when others may be tempted to chase volume at any cost.

On top of that, Sabre has a robust claims management system and strong anti-fraud capabilities. This means losses are controlled, underwriting profit is preserved, and the business avoids surprises that can hit insurers hard. The company’s diversified distribution strategy includes multiple channels, from long-established broker relationships to three direct-to-consumer brands. This breadth helps reach a wide range of customers efficiently without blowing out costs.

Risk management is another strength. Sabre uses excess of loss reinsurance to shield itself from very large claims and maintains a low-risk investment portfolio to protect capital. Operations are run from a single site with some specialist functions outsourced, keeping the cost base lean and manageable.

Latest trading update shows discipline over volume

The trading update for the first four months of 2025 revealed Sabre is sticking to its guns, prioritising profit over volume in a challenging market. Gross written premiums were down compared with the same period last year. Total premiums came in at £66.1 million compared to £85.7 million for the first four months of 2024.

That drop looks significant at first glance but the previous year was an exceptional one for growth, partly fuelled by unusually favourable market conditions that are not repeating this year. When we compare against the prior five-year average, Sabre’s premiums are actually up by over 8%. This detail matters because it shows that while the company has pulled back from chasing volume aggressively, it is still growing steadily when measured over a longer horizon.

CEO Geoff Carter put it well. The company has managed the insurance cycle according to its long-term plan, deliberately reducing the volume of business written during a period of weak pricing to protect margins and profitability. This pricing discipline means Sabre is confident it can deliver strong profit and dividends in 2025 despite the softer market environment.

The loss ratio – the proportion of claims paid out compared to premiums earned – remains in line with the company’s target, confirming that underwriting remains robust. The solvency capital ratio has improved too, sitting comfortably above the 171 percent reported at the end of 2024. This reflects solid profitability year to date and a strong capital position that supports both growth and dividend payments.

Growth plans and market positioning

Sabre’s recent launch of the Sabre Direct Motorcycle product is a clear signal the company is diversifying and expanding its footprint in key niches. While still in a test and learn phase, this product strengthens Sabre’s presence in the motorcycle insurance market, which can offer attractive margins when managed properly.

On the technology front, Sabre is progressing with an upgrade to its pricing infrastructure expected to be trialled in the second half of 2025. This is a key part of the company’s Ambition 2030 plan. Improved pricing accuracy and responsiveness could drive both premium growth and better underwriting profitability in the years ahead.

The wider UK motor insurance market has seen price reductions of around 15% over the last year, but recent data suggests this downward trend has flattened out. Claims inflation and other cost pressures are likely to push premiums higher later in 2025. Sabre’s disciplined approach means it is well placed to benefit when the market turns, as it will be ready to write business at healthier prices.

The company expects a slight reduction in total premium volume year on year for the rest of 2025. This cautious stance reflects the ongoing soft pricing environment but supports maintaining margins, profitability, and a strong balance sheet.

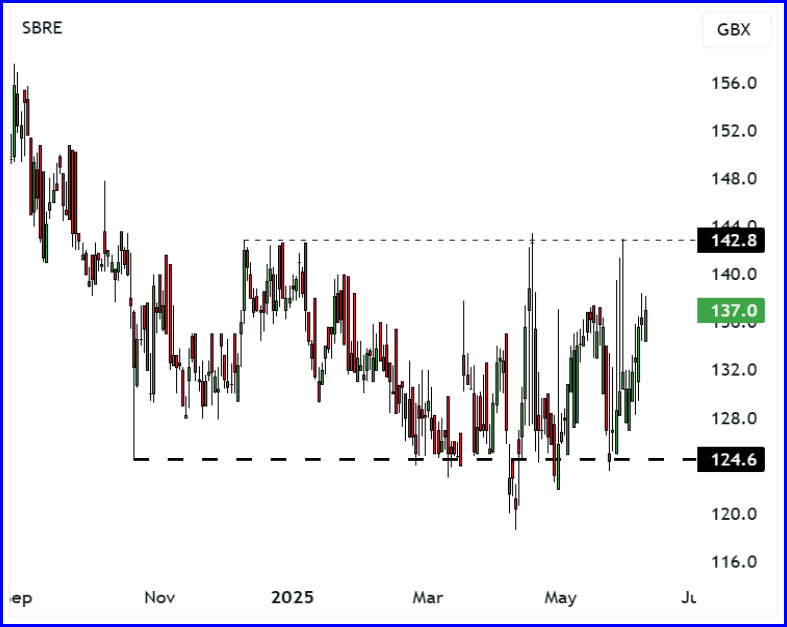

Technical analysis: Stability over momentum

Sabre’s share price chart is not the most exciting from a momentum or trend perspective. The price action shows consolidation and sideways movement rather than a clear upward trend. But for a company valued for steady dividends and reliable cash flow, stability is the key.

The share price has found solid support near the October 2024 lows around 124 pence. Although the price has dipped briefly below this level on occasion, the market has defended this support multiple times, suggesting buyers are keen to step in at this level.

More encouragingly, an inverted head and shoulders reversal pattern appears to be forming. This classic technical formation often signals a potential long-term trend change if confirmed. The confirmation would come with a breakout above the recent swing highs that have acted as resistance since the start of the year. Should this happen, it would support a more sustained recovery in the share price, aligning with the company’s improving fundamentals.

Dividend and valuation: A yield worth watching

One of the biggest draws to Sabre is its dividend yield. The forecast dividend yield is just under 10%, which is highly appealing in the current low-interest-rate environment where reliable income streams are rare. The company has historically maintained dividend cover above one times earnings, with a forecast cover around 1.17 for 2025 and 2026. This means the dividend payments are comfortably supported by the company’s earnings and cash flow.

Dividend growth has been uneven in recent years, reflecting the cyclical nature of the insurance market and the company’s cautious stance during tougher times. However, with premiums stabilising and underwriting profitability improving, the outlook for sustainable dividend payments looks solid.

Valuation metrics reflect cautious optimism. Sabre trades on a forecast price to earnings ratio of 8.6 times, below many peers in the insurance sector. This low multiple signals the market’s wariness over the insurance cycle but also suggests upside potential if the company continues to deliver disciplined profit growth.

The price to book value ratio is about 1.3 times, suggesting the stock is reasonably valued relative to its net assets. The enterprise value to EBITDA ratio sits near 6.3 times, which is quite reasonable for a company with Sabre’s financial stability.

Free cash flow generation is steady, though the price to free cash flow ratio at 15.4 times indicates investors pay a moderate premium for the security of cash flow and a strong dividend yield.

Sabre’s quality scores further reinforce its appeal. Return on equity sits at 14.4% and operating margins at nearly 21%. These figures show the company generates profit efficiently and underline the strength of its dividend model.

For investors seeking a dividend-focused exposure to UK motor insurance, Sabre offers a reassuring combination of stability, income, and the potential for recovery. Ultimately, Sabre is a story of patience, prudence, and pricing discipline. It is not about quick wins but about making steady progress in a cyclical industry where getting the risk pricing right makes all the difference.

SBRE 3-Year Chart

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.