1st Oct 2025. 9.00am

Regency View:

BUY Investec (INVP)

- Value

- Income

Regency View:

BUY Investec (INVP)

Investec: Value, income and a buyback boost

This week we are turning our focus to a good old fashioned value and income play. Investec (INVP) might not grab the attention of growth hunters or the AI crowd, but for long-term investors who like a combination of deep value, strong cash generation and a generous dividend, the shares are starting to look very appealing.

The group’s latest trading update shows a business quietly ticking along, delivering resilient earnings, and returning capital to shareholders, all while trading on valuation metrics that look distinctly undemanding. For investors willing to look past the glitz of the mega-caps and focus on steady, compounding returns, Investec is worth a closer look.

Specialist banking meets wealth management

At its core, Investec is a hybrid: part specialist bank, part wealth and investment manager, operating with a dual-listed structure in London and Johannesburg. The DLC framework allows it to run seamlessly across its key markets while maintaining local legal and regulatory structures.

In practice, the business serves two main client groups. The first is corporates and high-net-worth individuals, where Investec provides lending, treasury and advisory services across both the UK and South Africa. The second is wealth and investment management, built around discretionary and annuity funds, a broader asset management platform, and its strategic tie-up with Rathbones in the UK. This adds meaningful scale and strengthens its presence in one of the most competitive wealth markets globally.

Undervalued and yielding over 7%

The most obvious hook with Investec right now is valuation. At around 557p, the stock trades on a forward P/E of just 6.7, well below the sector average, and at a discount to book value with a price-to-book ratio of 0.93. In simple terms, you can buy £1 of Investec equity for less than 95p. That is not something you see often in a large cap financial services group with a strong track record of profitability.

On top of that, the shares carry a forecast dividend yield of just over 7%, covered nearly two times by expected earnings. For income investors, this is about as close as you get to a sweet spot: a high yield, backed by strong cover, and supported by operating margins comfortably above 35%. It screens well on classic value and income filters and stands out in a market where reliable income is hard to find.

Profitability holding its ground

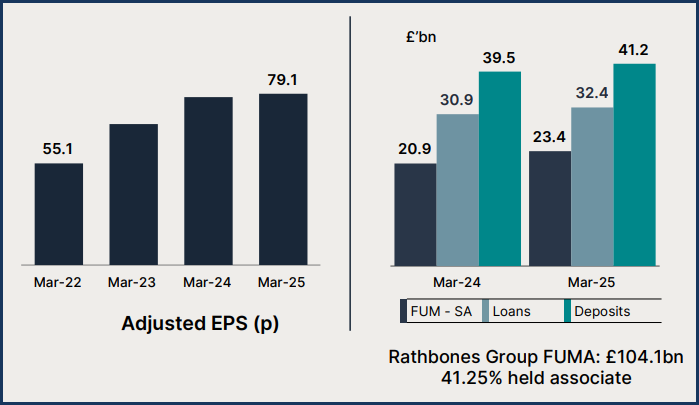

Earnings have shown volatility in the past, but the normalised EPS trajectory tells a more encouraging story, with an average growth rate of nearly 20% over five years. The most recent pre-close update suggests adjusted EPS will come in broadly flat year on year, a solid result given the softer macro environment.

Group return on equity sits at 13 to 14%, right in the middle of management’s target range of 13 to 17%, while operating margins remain close to 38%. These are levels that many banks would struggle to match. Costs are edging higher as the group invests in people and technology, but that is the price of building scale and improving client service, and margins remain resilient enough to absorb it.

Growth in the right places

Investec is not chasing aggressive expansion, but the areas where it is growing look sensible. Core loans rose at an annualised 5.5% in neutral currency over the latest five months, supported by both corporate lending and private client lending across its two main geographies. That steady expansion adds to the revenue base and underpins net interest income.

Wealth management continues to be a bright spot. In South Africa, funds under management climbed nearly 8% with healthy discretionary inflows, while in the UK the partnership with Rathbones adds exposure to more than £100bn of client assets. Together, these businesses give Investec a meaningful position in long-term wealth creation, an area with structural growth tailwinds as demographics shift and more clients seek professional advice.

Capital strength and buybacks

Balance sheet resilience is another reason to feel comfortable here. CET1 ratios stand at 12.2% in the UK and 15.3% in South Africa, both comfortably above regulatory requirements. Net gearing is low, liquidity is strong, and the group has room to absorb shocks while still funding growth initiatives.

Perhaps more telling is what Investec is doing with that capital. Earlier this year, management launched a £100m share buyback programme and has already executed nearly half of it. Combined with a dividend stream that has grown strongly over the past five years, this shows a clear focus on rewarding shareholders. For long-term investors, that mix of dividends and buybacks can compound quietly in the background, steadily lifting returns.

Technical timing looks supportive

From a charting perspective, the set-up is looking constructive. After a tough spell earlier this year, Investec’s share price has recovered well from its April lows, carving out a series of higher swing lows. The shares are tracking above both the 50 day and 200 day moving averages, with the shorter average recently crossing above the longer term line, a bullish signal known as a golden cross.

Even more interesting is what happens when we anchor a volume weighted average price to those April lows. This gives us a true sense of the average institutional buying price. Right now, Investec’s shares are trading above that anchored VWAP and have used it as support in recent sessions. With the price back near this level, the technical timing looks supportive for investors considering an entry point.

In a market where plenty of financial names are still working through legacy issues or fighting margin pressure, Investec offers something different: stability with upside. The shares remain cheap, the dividend is generous, and the technicals suggest timing is on the side of new buyers. For long-term FTSE investors seeking value, income and capital discipline, we believe Investec deserves a buy rating.

INVP 3-Year Chart