7th Jan 2026. 9.01am

Regency View:

BUY Intertek (ITRK)

- Growth

- Income

Regency View:

BUY Intertek (ITRK)

Keeping a keen eye on quality at market highs

When equity markets are making headlines for all the right reasons, discipline matters more than excitement. The FTSE pushing to fresh all-time highs is a welcome sight, but it also changes the job of the investor. This is no longer about chasing what is working fastest. It is about being selective, focusing on businesses with durable earnings, strong returns and valuations that still make sense when optimism is already high.

That is where Intertek (ITRK) comes into the conversation. It has not been a market darling over the last year. In fact, the shares have lagged noticeably while the index has surged ahead. But that divergence is precisely why the stock is interesting today. The business has continued to deliver steady growth and strong returns, while the valuation has quietly reset. In a market where plenty of stocks are priced for perfection, Intertek offers a more measured proposition.

Quality matters most when markets are expensive

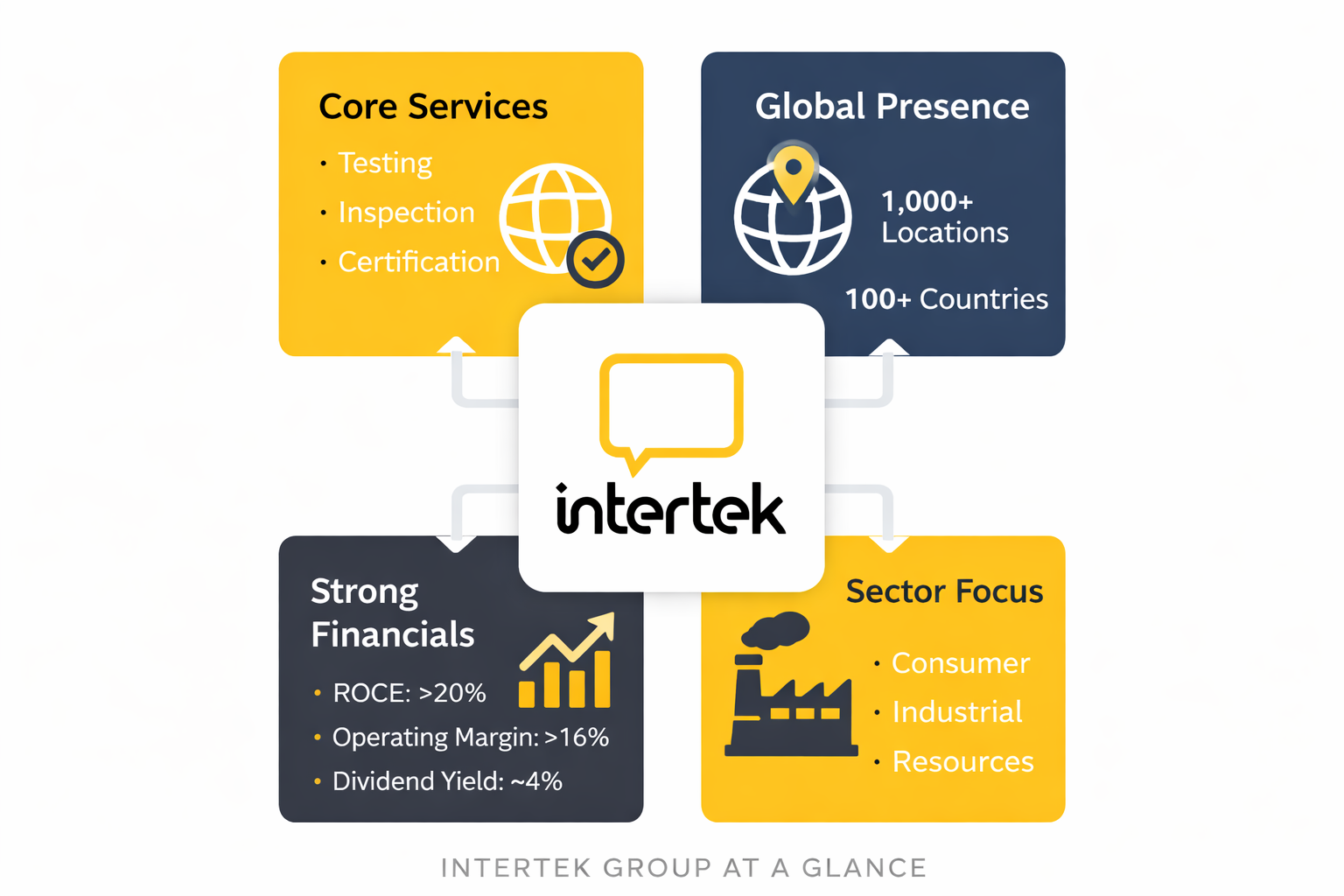

Intertek sits firmly in the “quality first” camp. It is a business built around testing, inspection and certification services that are woven into global supply chains. This is not discretionary spending that companies can easily switch off. Regulatory standards, safety requirements and quality assurance obligations tend to tighten over time, not loosen. That creates a reliable, recurring demand profile that supports earnings through different economic conditions.

The numbers reinforce that point. Intertek continues to operate with an operating margin of just over 16%, and returns on capital remain strong with ROCE above 20%. Return on equity is close to 30%, reflecting a business that converts revenue into profit efficiently. These are not peak-cycle metrics. They are the result of a capital-light model, pricing discipline and scale advantages that have been built up over many years.

Importantly, none of this has deteriorated during the period of share price underperformance. Revenues have edged higher to around £3.4bn, earnings have grown, and cash generation has remained robust. This is not a story of fundamentals weakening. It is a story of expectations cooling.

A valuation reset, not a broken story

Over the last year, Intertek’s share price has fallen around 17%, even as the FTSE has pushed higher. That is uncomfortable on the surface, but the reason matters. Rather than a single negative event, the share price drift reflects a slow reset in expectations. Organic growth has at times come in softer than the market hoped, prompting a valuation derating despite margins, returns and cash generation remaining intact.

Today, Intertek trades on a forward PE of around 17x. That is not cheap, but it is far more reasonable than the multiples investors were willing to pay previously. Free cash flow remains strong, with a price-to-free-cash-flow multiple in the mid-teens, and the balance sheet remains well supported with interest cover comfortably above 13x. Net debt has risen, but it remains manageable for a business with predictable cash flows and limited capital intensity.

This is the type of valuation reset long-term investors should welcome. It improves the margin of safety without compromising the quality of the underlying business.

Income with growth still on the table

Intertek is not pitched as a high-yield income stock, but it does offer a dependable return while investors wait. The forward dividend yield sits at around 3.8%, and the payout is well covered with dividend cover around 1.5x. Importantly, dividends have continued to grow over time, reflecting management confidence in cash generation rather than a desire to maximise short-term yield.

Looking ahead, earnings growth expectations remain sensible rather than heroic. Consensus forecasts point to high single-digit EPS growth, supported by organic growth, bolt-on acquisitions and ongoing operational leverage. In a market where many stocks require perfect conditions to justify their valuations, that kind of steady progress is valuable.

Reading the chart without rose-tinted glasses

Technically, this has not been an easy stock to own. The chart shows a broad, frustrating range over much of the past year, with several rallies failing to gain traction. Most recently, the shares dipped even as the FTSE broke to new highs, which naturally raises eyebrows.

However, the structure of the move matters. This has not been a disorderly sell-off. The 200-day moving average has flattened rather than rolled sharply lower, suggesting consolidation rather than a breakdown. Recent selling pressure eased quickly, and buyers stepped in around the mid-4400s, preventing a deeper slide. That behaviour is consistent with profit-taking and rotation, not institutional capitulation.

In other words, the chart reflects apathy more than alarm. That is often the environment where quality stocks quietly build a base.

A sensible choice at elevated levels

Intertek is not the most exciting stock in the market, and that is precisely the point. At times like this, excitement is often fully priced. Quality, discipline and patience are not.

This looks like a business that has done the hard work while the share price has stood still. With expectations reset and fundamentals intact, Intertek offers a sensible way to stay invested without stretching risk at a time when markets are already feeling confident.

For investors keeping a keen eye on quality as the FTSE makes new highs, Intertek stands out as a calm, considered choice.

Five key takeaways

1. Proven quality: Intertek delivers consistently high returns on capital, strong margins and dependable cash generation through the cycle.

2. Valuation reset: A year of share price underperformance has brought the forward PE down to more reasonable levels without any deterioration in fundamentals.

3. Defensive growth: Regulatory driven demand and recurring revenues support steady earnings growth even if the economic backdrop softens.

4. Income with resilience: A near 4% dividend yield, supported by solid cash flow and sensible cover, provides income while investors wait.

5. Opportunity at market highs: With the FTSE at record levels, Intertek offers exposure to a high quality business that has not already been fully rerated.

ITRK 3-Year Chart

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.