18th Feb 2026. 9.00am

Regency View:

BUY Diploma (DPLM)

- Growth

Regency View:

BUY Diploma (DPLM)

Diploma: Brilliantly boring

Markets love excitement, but they tend to reward consistency. The problem is that consistency rarely looks interesting. It does not come with dramatic turnarounds or bold promises. It usually shows up as steady growth, disciplined decisions, and a business that just keeps delivering. That kind of story does not grab headlines, but it has a habit of doing something far more useful over time, which is compounding shareholder returns.

Diploma (DPLM) is a textbook example of that. There is nothing flashy about its markets or its strategy, yet the results keep stacking up. Organic growth remains solid, margins are strong, cash generation is reliable, and the acquisition engine is still turning. The shares are not cheap, and they rarely are, but that is the price the market puts on consistency. In a year already full of noise and narratives, Diploma’s appeal is refreshingly simple. It keeps executing, and investors keep getting paid for it.

A decentralised machine that keeps delivering

Diploma’s model is built around value-add distribution in highly specialised niches, ranging from seals and controls to life sciences and aerospace fasteners. It is not a scale-at-any-cost operator. Instead, it focuses on businesses where technical expertise, availability, and reliability matter more than price alone. That shows up clearly in the numbers.

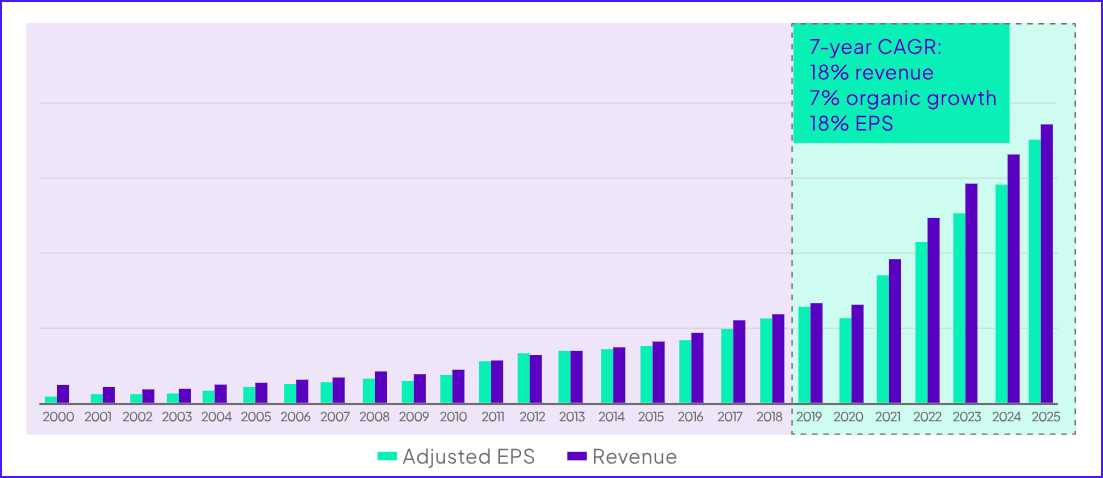

For the year ended September 2025, revenue reached £1.525bn, up from £1.363bn the year before. Operating profit increased to £276m, and net profit rose to £185m. Normalised earnings per share were 153p, compared with 127p the year before, a gain of just over 20%. Over the last five years, revenue has compounded at just over 23% per year, while normalised EPS has grown at roughly 26% per year. That is not cyclical noise. That is a business that has consistently found ways to grow both organically and through acquisitions.

Returns remain strong rather than spectacular, but importantly they are durable. Return on capital employed sits at 18.2%, return on equity at 19.7%, and operating margins have moved up to just over 18% in FY25. Management’s guidance points to an adjusted operating margin around 22.5% for FY26, which underlines that the direction of travel is still positive rather than peaking.

This is also a business that converts profit into cash reliably. Free cash flow per share in FY25 was 188p, up from 129p the year before, and operating cash flow per share was 199p. That cash generation is what funds the steady dividend progression and, more importantly, the acquisition engine.

The January update: execution, not excuses

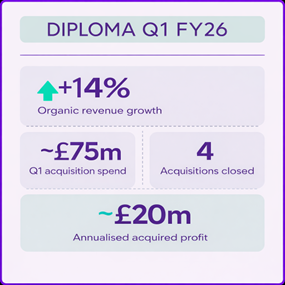

The January 2026 trading update covered the three months to the end of December 2025 and it was unambiguously strong. Organic revenue growth came in at 14% for the quarter. That is well ahead of the company’s full-year organic growth guidance of 6%, even allowing for the fact that management have said growth will be weighted to the first half.

Alongside that organic performance, Diploma completed four acquisitions in the quarter for around £75m, targeting aerospace fasteners, hydraulic seals, machining parts for OEM applications, and defence-related components. Taken together with the previous quarter, that makes eight acquisitions across two quarters for roughly £130m, with an expected annualised operating profit contribution of around £20m.

Crucially, management did not chase the numbers by hiking guidance aggressively. Organic growth guidance remains at 6% and margin guidance remains around 22.5%, while net acquisition growth has been nudged up to 3% from 2%. That is exactly the kind of conservative framing you would expect from a team that prefers to upgrade later rather than disappoint early.

The message here is not that Diploma has suddenly become a high-octane growth story. It is that the existing model is working as intended. Organic growth is healthy, the acquisition pipeline is active, and integration risk remains low because the deals are small, frequent, and in familiar territory.

Valuation: paying for quality

There is no getting away from the fact that Diploma is not cheap. On current numbers, the shares trade on a forward PE of about 26.9 times, with a PEG ratio around 1.8 and a forecast dividend yield of roughly 1.25%. On trailing figures, the price to free cash flow multiple is close to 28.5 times, and EV to EBITDA is just over 20 times.

That is the price you pay for consistency, predictability, and a long record of compounding. The market is not treating Diploma as a cyclical distributor. It is treating it as a structural compounder with a proven playbook.

The balance sheet remains supportive rather than stretched. Net debt at the last year end was £383m, against a business generating nearly £200m of operating cash flow per year and with interest cover above 11 times. This is not a leveraged roll-up. It is a business that uses debt as a tool, not a crutch.

Dividends continue to grow steadily rather than spectacularly. The FY25 dividend was 62.3p, up from 59.3p the year before, and forecasts point to mid-single-digit growth continuing. Yield will never be the attraction here. Reliability and reinvestment capacity are.

What the chart is saying

After a strong run over the past few years, the shares have spent recent months moving sideways rather than higher. They are around 7% below the 52-week high and broadly in a consolidation phase above the rising long-term moving average. Momentum over one, three, and six months has been mildly negative, but the longer-term trend remains intact.

This kind of price action is not unusual for high-quality compounders. Periods of digestion often follow strong advances, especially when valuation has become full. What matters more is that there is no sign of structural breakdown, and no fundamental evidence that the business is losing its edge.

In other words, the chart is not flashing a warning about the model. It is reflecting a market that is waiting for earnings to catch up with expectations again.

The real investment case

The reason Diploma still works in a portfolio like yours is not because it looks cheap, and not because it is about to surprise on a single quarter. It works because it combines three rare traits in one package.

First, it operates in niche markets where service, reliability, and technical know-how matter more than price. That supports margins and customer loyalty. Second, it has a repeatable acquisition engine that has been proven over many years, not just in one cycle. Third, it converts profits into cash and reinvests that cash with discipline rather than ambition for ambition’s sake.

The January update reinforces that nothing in this machine is slowing down. Organic growth is healthy, acquisitions are continuing at a sensible pace, and margins are being protected. The share price may be taking a breather, but the business itself is not.

This is not a stock for bargain hunters or for those looking for a quick rerating. It is a stock for investors who are willing to accept a premium valuation in exchange for a high probability of steady compounding.

Five Key Takeaways

1. High quality: Consistently strong margins, high returns on capital and reliable cash generation underline the strength of the model.

2. Dependable growth: Double digit organic growth in Q1 and a long track record of compounding earnings support a strong medium term outlook.

3. Disciplined acquisitions: A busy and well funded M&A pipeline continues to add incremental growth without stretching the balance sheet.

4. Premium, but justified: The shares trade on a higher multiple, but that reflects durability, visibility and a proven ability to compound value.

5. Trend intact: Despite recent consolidation, the longer term share price structure remains constructive, consistent with the underlying fundamentals.

DPLM 3-Year Chart

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.