19th Mar 2025. 9.04am

Regency View:

BUY Diageo (DGE)

- Value

- Income

Regency View:

BUY Diageo (DGE)

Diageo offers deep value for the resilient investor

Value investing is not for the faint-hearted. The best opportunities often appear when sentiment is at its worst, and buying into a company that has fallen out of favour takes patience and conviction. More often than not, it’s darkest before dawn—great businesses can see their share prices slump as the market fixates on short-term concerns. The key is distinguishing between companies in structural decline and those experiencing a rough patch.

Diageo (DGE) is a prime example of this dynamic. Its share price has been cut in half since 2021, and the stock is deeply out of favour with investors. Yet, while the challenges are real, the long-term investment case remains intact. With the shares retesting a major technical level, there is a growing argument that this could be a rare opportunity to acquire a world-class business at a discount.

A challenging backdrop

Diageo’s latest results underscore the difficulties it has faced. While organic net sales edged up by 1% to $10.9 billion, reported operating profit slipped by 5%, reflecting cost pressures and shifting consumer trends. The North American market—a key revenue driver—showed some resilience, with strong demand for premium brands like Don Julio and Crown Royal. However, growth was more muted elsewhere, particularly in Latin America and Asia.

The company’s decision to abandon its medium-term growth targets highlights the uncertainty in the spirits industry. Changing consumer habits, potential US tariffs on Scotch whisky, and macroeconomic headwinds all pose challenges. Inflation and rising interest rates have also squeezed disposable incomes, leading some consumers to trade down from higher-end brands.

Yet despite these issues, Diageo remains a highly cash-generative business. It produced £1.7 billion in free cash flow over the period, allowing it to maintain its dividend. The payout remains well-covered, offering investors a degree of stability in turbulent markets.

Unrivalled brand portfolio

One of Diageo’s greatest strengths is its dominant position in the global drinks market. The company owns an extensive portfolio of world-renowned brands, including Johnnie Walker, Guinness, Smirnoff, Tanqueray, and Baileys. These brands have deep consumer loyalty, giving Diageo pricing power and a degree of insulation from economic cycles.

The spirits industry has historically been a reliable store of value, with premiumisation trends driving long-term growth. Consumers may adjust their spending habits in downturns, but demand for high-quality alcoholic beverages tends to be resilient. Diageo’s ability to maintain strong operating margins, currently at 28.6%, reflects this advantage.

The company also benefits from a global distribution network that few can match. Its presence in over 180 markets gives it scale and flexibility, allowing it to navigate regional economic challenges. While short-term pressures exist, the long-term fundamentals of the business remain intact.

Valuation: Attractive relative to history

Diageo’s valuation has come down considerably, but it still trades at a forward P/E of 15.7 and a price-to-free-cash-flow ratio of 22.3. While not outright cheap, these levels are well below the company’s historical averages, suggesting the market has priced in much of the recent negativity. The 3.88% dividend yield is now at the higher end of its range, providing a compelling source of income.

Returns on capital employed (15.8%) and equity (35.8%) remain robust, reflecting Diageo’s strong underlying profitability. The stock’s price-to-sales ratio of 2.98 and EV/EBITDA multiple of 12.52 indicate that while Diageo is not in deep value territory, it is trading at a discount relative to its long-term growth potential.

Technicals: A key support level in play

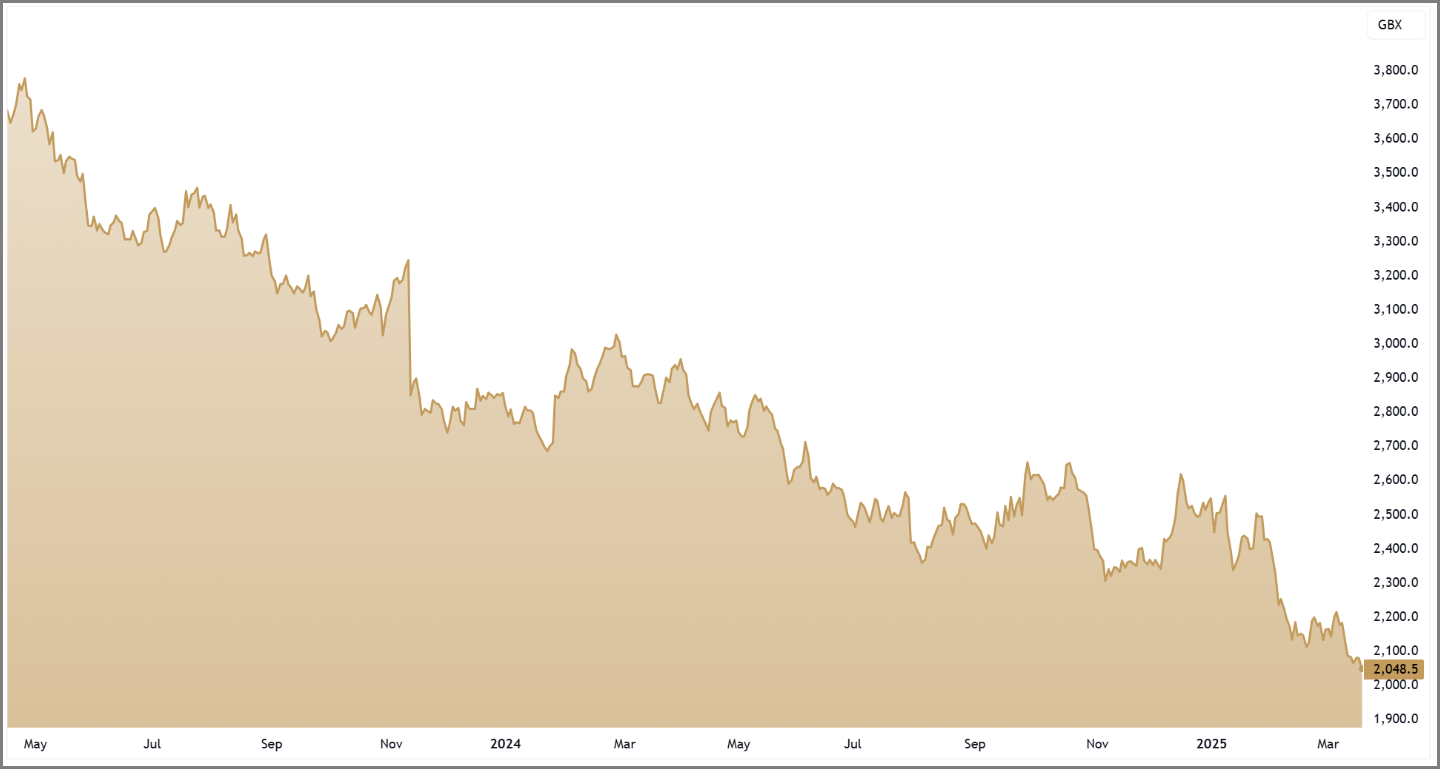

Diageo’s price action has been nothing short of brutal, with the stock down 35.6% over the past year. However, it has now reached a major technical level, retesting the March 2020 pandemic lows. Early signs of buying interest emerged this week, with bullish divergence appearing on the Relative Strength Index (RSI). This suggests that while the broader trend remains bearish, downside momentum may be beginning to fade.

DGE retests long-term support

The bottom line

Diageo is facing a challenging environment, but the market may have overreacted. The company retains its status as a global drinks powerhouse, with a portfolio of leading brands, strong cash flow, and a well-covered dividend. While risks remain, the combination of an attractive valuation and momentum divergence suggests that now could be a compelling time for long-term investors to take a closer look.

DGE 3-Year Chart

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.