29th Apr 2026. 9.05am

Regency View:

BUY DCC (DCC) Second Tranche

- Value

- Income

Regency View:

BUY DCC (DCC) Second Tranche

DCC: Powering Higher on Energy Volatility

Following this morning’s publication, DCC has opened strongly, moving higher at the open. Moves like this can feel uncomfortable, but they often reflect the market starting to recognise the shift in expectations we outlined in the report.

We are not chasing strength, but positioning within a developing trend, where momentum and improving sentiment are starting to align.

DCC (DCC) has started to move. After a prolonged period of underperformance, the shares are beginning to reflect a shift in both sentiment and expectations, with recent price action suggesting the market is starting to look forward rather than back.

With momentum building and the underlying story becoming clearer, we are adding a second tranche to the position…

A Business in Transition

DCC is an international sales, marketing and support services group, with its core strength now firmly centred on its energy division. Historically, the group operated across multiple segments, including technology and healthcare, but management has been actively simplifying the business to focus on higher-return energy operations.

This shift is important. Energy distribution and marketing is not a high-margin business, but it is highly scalable and benefits from volume, pricing dynamics and operational efficiency. More importantly in the current environment, it can benefit from volatility in energy markets, as pricing dislocations and demand shifts create opportunities to expand margins.

The ongoing disposal of non-core divisions, including the remaining technology business, is helping to sharpen this focus. As the group transitions into a more streamlined energy-led business, the investment case becomes clearer, which is often a key ingredient in driving a re-rating.

From Weakness to Recovery

Looking backwards, the numbers have been underwhelming. Revenue has declined in recent periods, margins have compressed and returns have fallen, with operating margins currently sitting below 2% and return on capital trending lower. This is precisely why the shares have struggled over the past year.

However, the more recent trading update tells a different story. DCC reported strong operating profit growth in the third quarter, with its energy division delivering a solid performance, particularly within its Energy Products and Mobility segments. While there were some weaker areas, notably within UK Energy Services, the overall direction of travel is improving.

Crucially, full-year guidance has been maintained. In a market where investors are highly sensitive to downgrades, the absence of negative surprises is significant. It suggests that the worst of the operational weakness may already be behind the business, allowing investors to start focusing on the recovery potential.

Forecasts reinforce this view. Earnings are expected to rebound strongly, with consensus pointing to a sharp recovery in the next financial year followed by continued growth thereafter. This is where the valuation starts to look compelling. With a forward PE of just over 10x and a PEG ratio below 1, the shares are still priced for a business with limited growth, despite improving fundamentals.

A Re-Rating in Motion

The shift in sentiment is starting to show up more clearly. Earlier this month, the shares were upgraded by Exane BNP Paribas, with the broker arguing that the market had been overly pessimistic and was effectively pricing in declining profits indefinitely. Their view is that earnings expectations are too low, particularly as DCC benefits from improving unit margins and favourable energy market dynamics.

This kind of upgrade matters. It signals that institutional investors are beginning to revisit the story, which is often how re-ratings begin. Combined with the company’s ongoing strategic simplification and the potential catalyst from the disposal of the remaining technology business, the ingredients for a sustained re-rating are starting to fall into place.

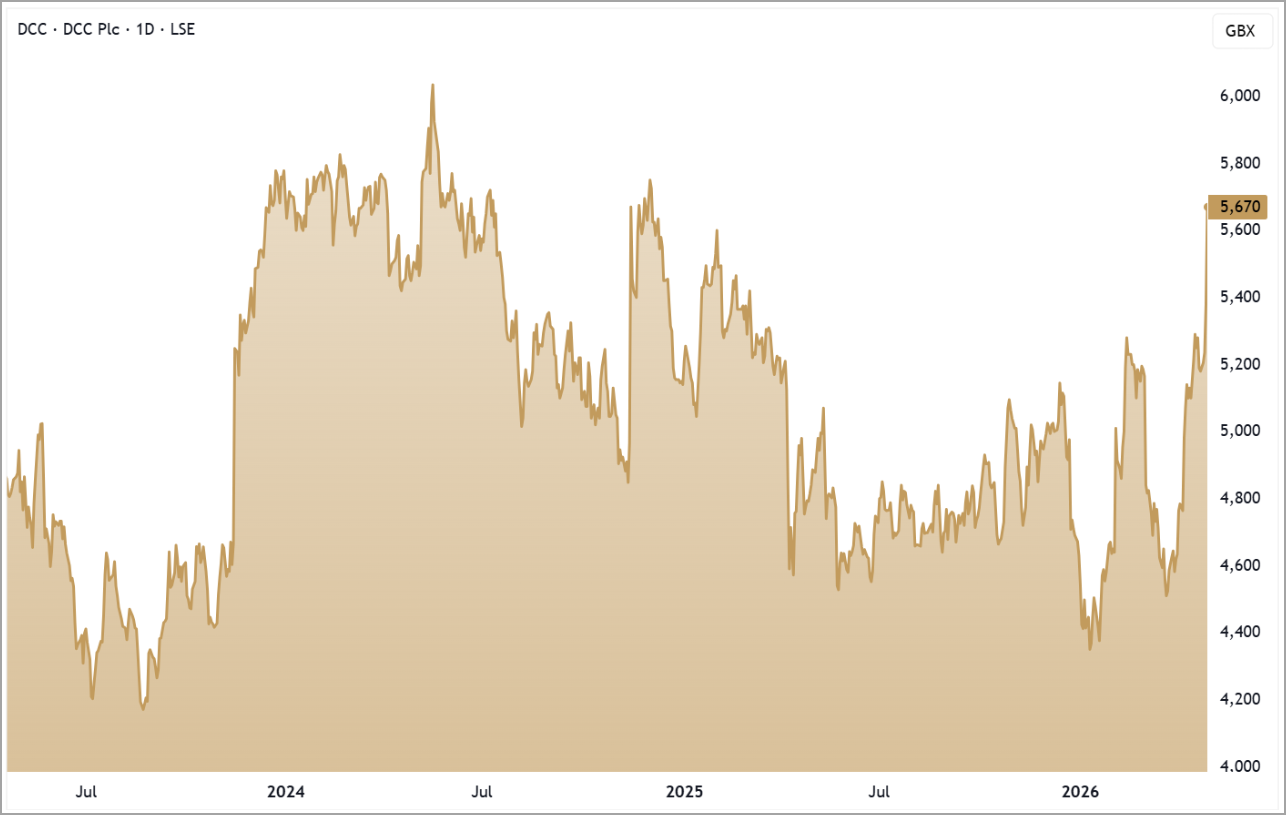

Technical Analysis: Momentum Confirms the Shift

The shares have started to reflect this improving narrative. After a period of consolidation, price has pushed higher and is now trading close to its 52-week highs. The move has been supported by strong relative strength over the past one and three months, indicating increasing buying interest.

Importantly, the shares are now holding above both the 50-day and 200-day moving averages, reinforcing the strength of the emerging trend. This is a notable change in behaviour compared to the previous year, where rallies struggled to sustain momentum.

The current setup suggests that the market is beginning to price in the recovery story. In this context, strength is not something to fade but something to respect. As expectations shift and positioning builds, trends like this can extend further than initially expected.

Why Add Now

We are not adding because the shares are cheap in isolation, nor because the recovery is fully proven. We are adding because the balance between risk and opportunity has shifted.

The business is showing early signs of operational improvement. The strategy is becoming clearer. External validation is starting to emerge. Most importantly, the market is beginning to respond.

By adding a second tranche here, we are increasing exposure to a position that is starting to work, rather than trying to pick a bottom in something that has yet to turn. In our view, this is the phase of the move where the probability of success improves, even if short-term volatility remains.

Five Key Takeaways

1, Recovery underway: recent trading suggests operational performance is improving.

2. Energy focus: simplification towards a pure energy business strengthens the story.

3. Valuation support: low multiple reflects past weakness, not future potential.

4. Re-rating potential: upgrades and catalysts are starting to shift sentiment.

5. Momentum building: price action confirms increasing investor interest.

DCC 3-Year Chart

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.