17th Sep 2025. 9.00am

Regency View:

BUY BT (BT.A)

- Value

- Income

Regency View:

BUY BT (BT.A)

Why boring BT belongs in your portfolio

Telecoms rarely sit at the top of a watchlist, yet the UK sector has quietly outperformed over the past year while delivering the kind of steady cash flows that portfolios love. BT (BT.A) is beginning to convert that steady profile into a more compelling story…

July’s trading update and boardroom news triggered a sharp re-rating on the day, then the market cooled and the share price drifted back in an orderly way. That sequence leaves us with something investors do not get very often in large caps. Momentum, a credible transformation plan, and a better entry point after a pullback.

For our current list of FTSE Investor stocks, BT fills a useful gap. We already carry plenty of financials and industrials, plus exposure to more cyclical names. A domestic telecom with a clear plan, solid cash generation, and a dependable income stream provides balance. It also gives us participation in the ongoing fibre and 5G buildout of the UK without taking commodity or export risk. In short, this is a quality of earnings call at a sensible price, with catalysts that are understandable and close at hand.

What you are really buying

BT is best thought of as three engines that work together Consumer, Business, and Openreach. Consumer houses the EE mobile brand and fixed broadband. Business serves corporates and the public sector in the UK and overseas. Openreach is the wholesale network that underpins the country’s digital plumbing. The strategic direction is to let Openreach keep building and filling the fibre network, while simplifying the customer facing businesses and focusing on service and retention. Management has already flagged that Business will be reported as two units from the second quarter of the next financial year, one focused on the UK and one on international operations. That separation should tighten accountability and improve visibility on progress.

This structure matters because it explains why BT can grow value even if headline revenue is not racing ahead. Openreach monetises a growing fibre footprint through higher take up and better speed mix. Consumer and Business pivot customers onto that footprint and sell converged services. When the network improves, churn falls and pricing power improves at the margin. That is the flywheel we are paying for.

Fibre first and simpler by design

Operational momentum is clear in the latest numbers. Full fibre now passes more than 19 million premises, with an average build rate of 81,000 per week. Management is on track to pass up to five million premises this fiscal year. Connected premises reached seven million, helped by record quarterly net additions that were 46% higher year on year. Take up across the footprint has risen to 37%, and rivals are increasingly signing onto Openreach, with Hyperoptic the latest to extend its wholesale access.

Mobile is moving in the right direction as well. The 5G network now covers more than 87%t of the UK population and the 5G base stands at 13.5 million. In Consumer, the broadband base grew during the quarter and the postpaid mobile base expanded too. Broadband average revenue per user rose in Openreach on a higher fibre mix and price changes, while Consumer average revenue per user was softer in the quarter but expected to follow the usual seasonal pattern over the year.

Cost transformation is doing the heavy lifting in earnings. The group has reduced total labour resource by 5%, network energy usage is down 5%, and Openreach repair volumes are down 14%. Those savings have fully offset higher employer costs tied to the National Living Wage and National Insurance.

Leadership succession adds another pillar. Simon Lowth, the group CFO, will retire after a managed handover, with Patricia Cobian of Virgin Media O2 appointed to succeed him next year. She brings deep UK telco experience and a track record through a major merger. That appointment signals continued discipline on capital allocation and supports execution of the plan already in motion.

Value where it counts

The financial print for the first quarter reads like a steadying ship. Group revenue of £4.88bn was down 3% year on year, with softer handset sales and international trading offsetting fibre progress. Adjusted UK service revenue fell 1%. Adjusted earnings came in at £2.05bn, down 1%, as cost actions cushioned the revenue headwind. Reported profit before tax was £468m, 10% lower, reflecting higher finance costs and guidance for the medium term was reconfirmed.

Valuation is the part that makes the case. The shares trade at about 11x forward earnings, with an enterprise value to EBITDA multiple a touch above 5.6x. The forward dividend yield is a shade above 4% and is covered more than 2x on normalised earnings. Net debt sits a little above £20bn, which is not light, but it is supported by regulated and recurring cash flows and a long lived asset base. Interest cover is tighter than we would like, yet manageable, and the balance of cash generation and capital investment is trending in the right direction as fibre capital intensity peaks and then fades. This is not a story about rapid top line expansion. It is about improving mix, stable margins, and disciplined capital deployment at a valuation that leaves room for a re rating if execution continues.

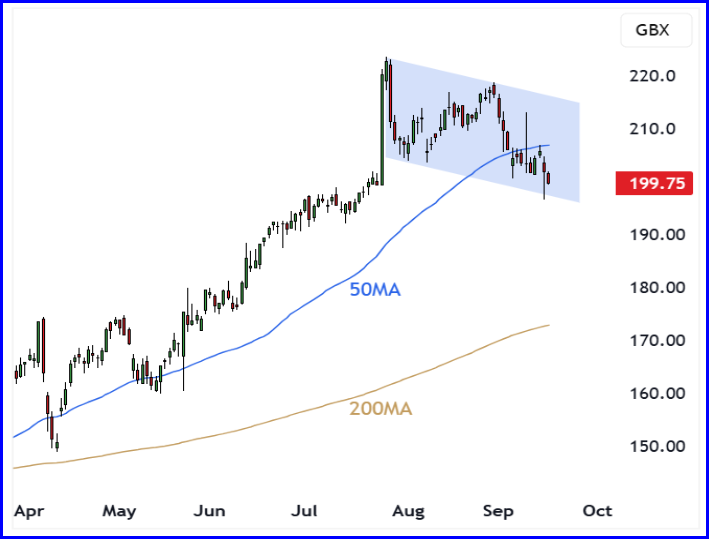

News pop now pullback

The market reaction to July’s news was unambiguous. A single session jump of around 10% is rare for BT and speaks to renewed confidence in the plan and in leadership depth. Since that burst, price has eased back in a steady fashion and remains well above the 200 day moving average. One year performance is strong, six month performance is strong, and the recent consolidation helps reset momentum without breaking the underlying uptrend.

For investors, that creates a straightforward action plan. Use the pullback to build a position rather than chasing a spike. The fundamental picture is improving, the valuation remains supportive, and the income stream pays you while the transformation compounds. If sector sentiment stays firm and operational milestones continue to land, the next leg higher can follow without needing heroic assumptions.

BT will not be the most exciting name in the book, and that is precisely why it belongs there. It brings resilience, a visible path to value creation, and a sensible price. In a portfolio that already leans into financials, industrials, and cyclicals, a fibre first telecom with improving service metrics and a covered yield is exactly the kind of ballast that lets you stay invested through the noise.

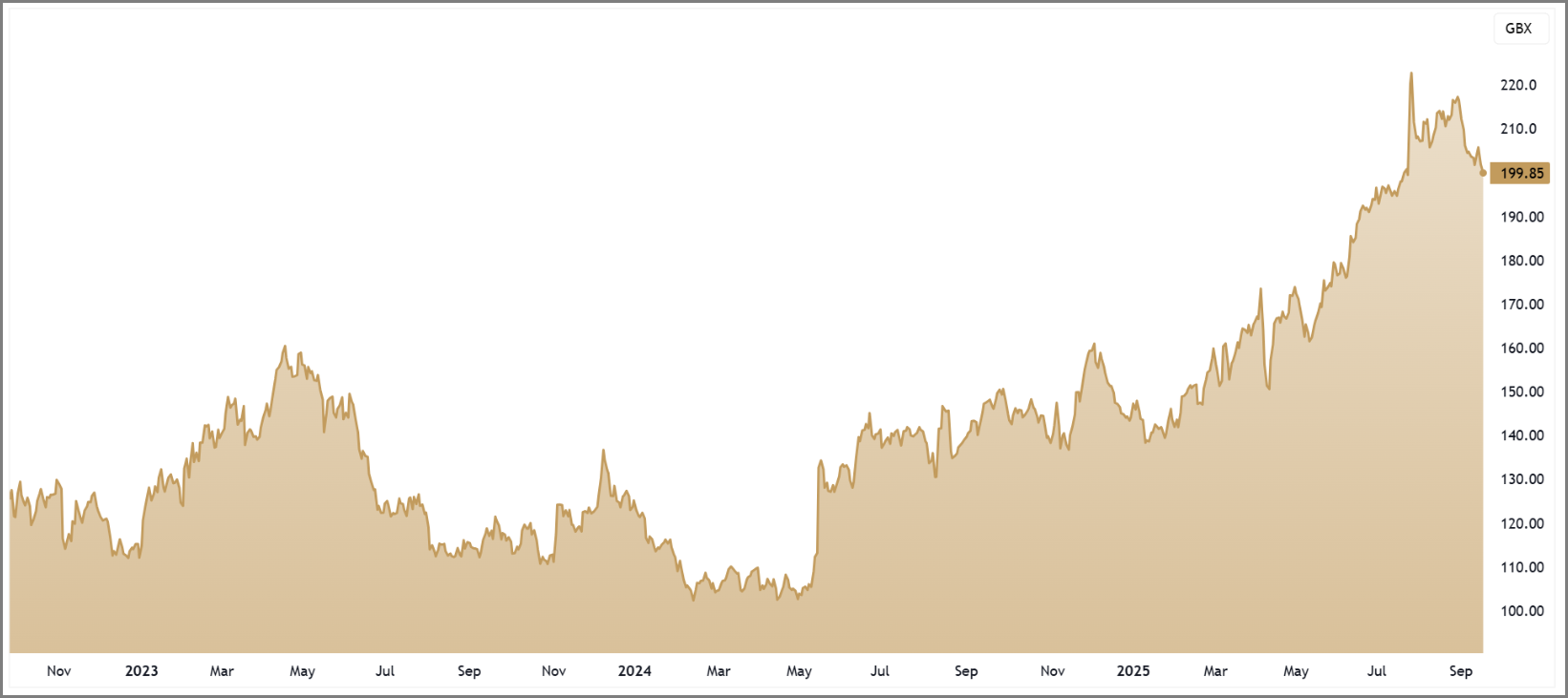

BT.A 3-Year Chart

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.