4th Mar 2026. 9.00am

Regency View:

BUY BP (BP.) Second Tranche

- Value

- Income

Regency View:

BUY BP (BP.) Second Tranche

More than a Middle East oil trade

The art and science of long-term investing are often stress tested after weekends like the one just gone. Geopolitical shocks cause spikes in risk appetite, take correlations to zero and leave even seasoned investors watching the blow-by-blow newsflow as markets reopen.

Adding another tranche of BP (BP.) when energy stocks are among the few parts of the market moving higher may appear obvious at first glance. But the decision is not about chasing a short-term spike in oil prices. It reflects the reality that disruptions to global energy distribution can take time to resolve, and companies with strong cash generation and established infrastructure tend to benefit when supply becomes uncertain.

Khamenei’s death changes the risk profile of the Middle East

The escalation in the Middle East is not simply another flare-up in a region used to tension. The death of Iran’s Supreme Leader Ali Khamenei has triggered a strategic shift that makes the security outlook far less predictable.

For years Iran has developed what it calls the “Decentralised Mosaic Defence” doctrine. Rather than relying on a single central chain of command, military authority is distributed across regional units that can operate independently if national leadership is disrupted.

With Khamenei now gone, that doctrine has effectively moved from theory into practice. Provincial commanders and Revolutionary Guard units can launch drone and missile attacks without waiting for direction from Tehran, creating what analysts describe as a fragmented battlefield with multiple autonomous actors.

For energy markets the implication is clear. When retaliation is decentralised, stabilising the situation becomes far harder. Even if diplomatic channels reopen or a new leadership structure emerges, there may be no single authority capable of immediately halting attacks on shipping routes and infrastructure across the Gulf.

A cash generating giant

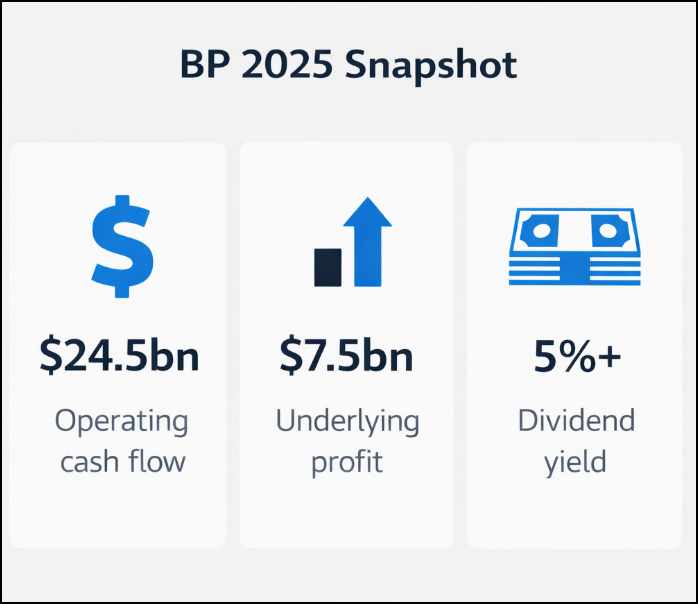

This is where BP comes back into focus. The company’s most recent full year results, released in February, show a business that remains capable of producing substantial cash even in a relatively moderate pricing environment.

For 2025 BP reported underlying replacement cost profit of $7.5bn alongside operating cash flow of $24.5bn. These numbers matter because they demonstrate the resilience of the company’s upstream portfolio and the continued strength of its integrated energy model.

Operational performance also remained solid. Upstream reliability reached record levels above 96%, while production remained broadly stable compared with the previous year. Downstream operations also delivered steady earnings, with refining and customer segments continuing to generate consistent contributions.

In other words, BP did not need a geopolitical shock to produce healthy cash flow. The business was already delivering meaningful earnings and operational progress before the latest developments in the Middle East.

Strengthening the balance sheet

One of the more important strategic decisions announced alongside the results was BP’s decision to prioritise balance sheet strength over aggressive shareholder distributions.

Net debt ended the year at $22.2bn, down from $26bn in the previous quarter, supported by asset sales and disciplined capital allocation. Management has also chosen to suspend share buybacks for now, allocating excess cash toward further debt reduction.

That decision may disappoint investors looking for short-term capital returns, but strategically it positions the company well for a more volatile energy environment. A stronger balance sheet provides flexibility to invest in upstream opportunities while maintaining dividend resilience.

The dividend itself remains a core pillar of the investment case. BP continues to target at least 4% annual dividend growth, reinforcing its role as a major income generator within the FTSE 100.

A breakout with room to run

The technical picture has also started to turn more constructive. After spending several months consolidating beneath resistance, BP’s shares have now broken above the upper boundary of that range, suggesting the market is beginning to reprice the stock.

Importantly, this move is not occurring in isolation. The shares are trading comfortably above both the 50 day and 200 day moving averages, with the longer term trend gradually turning higher. That type of structure often signals that momentum is beginning to shift back in favour of buyers after a prolonged period of sideways price action.

The breakout also comes after a lengthy consolidation phase that allowed the previous rally to reset. Rather than a sharp vertical spike, the chart reflects a market that has absorbed supply and built a stronger base before attempting to move higher.

With momentum indicators such as RSI moving into bullish territory but not yet stretched, the technical picture suggests there is still room for the trend to develop.

For long term investors, that combination of improving fundamentals, supportive sector dynamics and a constructive chart pattern strengthens the case for adding a second tranche.

Five Key Takeaways

1. Energy security back in focus: Escalating tensions in the Middle East highlight how vulnerable global oil distribution can be.

2. Strong cash generation: BP generated $24.5bn of operating cash flow in 2025 despite a softer oil price environment.

3. Balance sheet improving: Net debt has fallen to $22.2bn, with a target of $14bn to $18bn by 2027.

4. Attractive income profile: Shares offer a dividend yield above 5% with management targeting at least 4% annual dividend growth.

5. Second tranche opportunity: With solid fundamentals and a supportive energy backdrop, adding to the position offers both income and potential upside.

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.