16th Apr 2025. 8.59am

Regency View:

BUY BAE Systems (BA.)

- Growth

Regency View:

BUY BAE Systems (BA.)

BAE shows undeniable strength amid uncertainty

Systemic sell-offs have a silver lining – they make it easy to separate the strong from the weak. In the case of BAE Systems, that strength has been glaringly obvious.

While much of the market was still reeling from the fallout of Trump’s abrupt tariff escalation – what some traders have now dubbed “Liquidation Day” – BAE shares barely flinched. They dipped, sure, but the bounce was swift, clean, and confident. That kind of price action speaks volumes.

When fundamentals and charts both point in the same direction, it’s usually worth paying attention. And right now, BAE offers the rare combination of robust order visibility, structural growth tailwinds, and technical resilience. In an environment where many stocks are scrambling to regain their footing, BAE looks like it never lost it.

Europe’s defence awakening

If ever there was a time for Europe to take its security into its own hands, this is it. With the US clearly pivoting its strategic focus – and showing signs of fatigue when it comes to bankrolling the West’s defence posture – Europe is finally waking up to the need for greater self-reliance. Cue the ReArm Europe plan.

This isn’t just political theatre. We’re talking about a multi-year, €800 billion defence overhaul, designed to boost readiness, close capability gaps, and foster a self-sufficient industrial base. That means EU nations are being strongly encouraged – both by policy and financial incentives – to buy European. And BAE, with its scale, technology leadership, and deep ties across the continent, is arguably the best-placed contractor to benefit.

We’re not just talking about headline figures here – we’re talking about a fundamental reshaping of Europe’s defence architecture. Mobility, stockpiling, systems integration, AI, quantum technology – this isn’t a procurement spree, it’s an industrial revolution. And BAE is right at the heart of it.

Strong growth, stronger business

BAE’s 2024 results were a clear reminder of why the business commands such investor confidence. Sales were up 9% to £25.3bn, with underlying EBIT climbing 10% to £2.7bn. But beyond the headline growth, it’s the quality and breadth of that growth that really stands out.

Momentum was broad-based. Electronic Systems, Maritime, Air, Cyber – all divisions contributed meaningfully, supported by a strong cadence of new orders and programme milestones. The acquisition of Ball Aerospace (completed for $5.5bn) not only broadens BAE’s space and electronics footprint but also demonstrates a willingness to invest in future capabilities without compromising financial discipline.

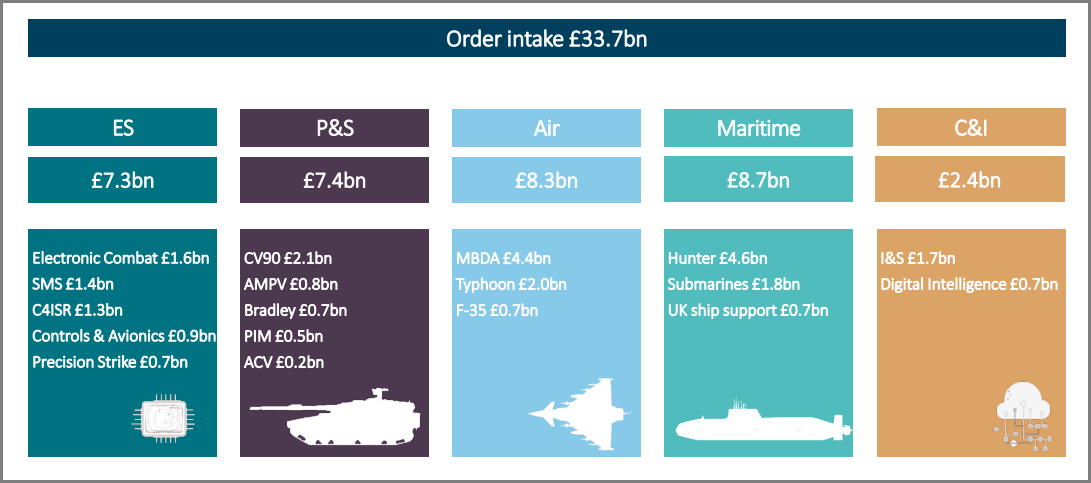

Free cash flow came in at £1.9bn, comfortably covering dividends and allowing for reinvestment. The order intake hit £33.7bn, lifting the backlog to a record £77.8bn. That’s not just future revenue locked in – that’s long-term visibility that most sectors can only dream of. When your business is this closely aligned with national security, budget volatility takes a back seat.

BAE Systems Order Intake

Not cheap – but worth it

Let’s address the obvious: BAE is no longer a value play. The stock trades on a forward P/E of around 20x, with a yield just above 2.5%. That’s not going to turn heads at first glance. But in this market – one where earnings durability and cash generation matter more than ever – the valuation starts to look a lot more reasonable.

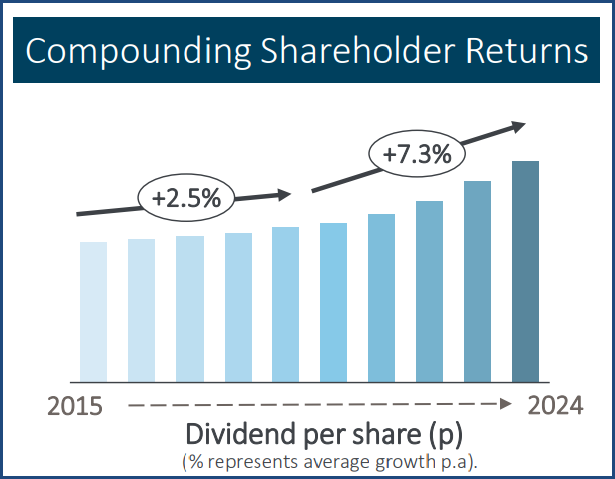

This is a high-quality, defensive compounder, with multi-year growth visibility, strong pricing power, and a shareholder-friendly capital return profile. You’re paying up for stability, recurring revenues, and structural tailwinds – and frankly, that’s a premium we’re happy to pay.

The shares go ex-dividend on Thursday, which usually brings a small markdown at the open. But if you’re taking a longer view, we’d argue it’s still worth buying ahead of the date to lock in the payout and position for further upside. Any post-dividend dip is likely to be short-lived – and possibly a final entry point before the next leg higher.

Charts that tell a story

It’s not often that a defence contractor chart makes you sit up straight – but BAE’s recent price action has been genuinely exciting (well, exciting for analysts anyway).

The shares gapped decisively higher in early March, surging through a major resistance level on the back of Europe’s defence spending push. That kind of breakout – with volume and a clear catalyst – is rarely a fluke. What followed was a textbook bullish consolidation: tight range, low volatility, and no give-back of gains.

Then came Trump’s tariff shock – and the market wobble that followed. BAE dipped with the rest of the pack, but crucially, it didn’t break trend. In fact, it bounced precisely from that former resistance level – now turned support. That kind of move suggests there’s real conviction behind the trend. Buyers were waiting.

The gap has been filled, support has held, and momentum is building again. With earnings catalysts, macro tailwinds, and institutional demand all lining up, we think the chart has plenty more to give.

BA. 3-Year Chart

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.