18th Mar 2026. 9.01am

Regency View:

BUY Babcock (BAB) International

- Growth

- Value

Regency View:

BUY Babcock (BAB) International

Back for a second sortie

There is always a danger in revisiting a stock too soon after taking profits. Sometimes the story has already played out, sentiment is too hot, and what looks like renewed strength is really just the final stretch of an old move. That is why Babcock (BAB) is worth approaching with a clear head rather than a nostalgic one.

We know this stock well. We locked in a gain of around 110% last April, which was exactly the right call at the time. The shares had rerated sharply, momentum was strong, and the easy money had been made. What makes Babcock interesting again today is not simply that defence remains in favour. It is that the business has continued to execute, earnings have kept moving higher, and the latest consolidation phase has left the shares looking more like a second chance than a victory lap.

From recovery story to real operator

A few years ago, Babcock was a very different proposition. The business was wrestling with restructuring, patchy execution, and a market that had lost confidence in management’s ability to turn the ship around. That version of Babcock is no longer the one in front of us.

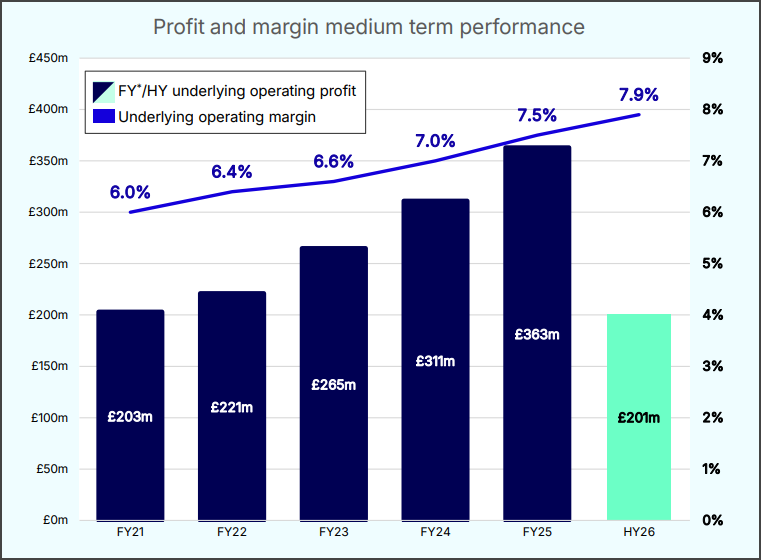

Today the numbers tell a much cleaner story. Revenue for the trailing twelve months has climbed to £4.96bn, while operating profit has improved to £414m. Normalised earnings per share have risen to 51.1p, with forecasts pointing to 56.1p for FY26 and 62.2p for FY27. Operating margins have continued to move in the right direction, reaching 8.35% on a trailing basis, while return on capital employed has improved to 25.4%.

That matters because it shows Babcock is no longer being held together by hope and government contracts alone. It is becoming a more focused, more productive business with stronger returns, better margin discipline and a clearer sense of where it can win.

Critical assets, long contracts, better visibility

What gives Babcock its appeal is not glamour. It is strategic relevance. This is a company embedded in areas that are difficult to replicate and increasingly important in a less certain world.

The group’s exposure to naval support, nuclear infrastructure, aviation and defence engineering puts it in the middle of several long-duration spending themes. That was evident again in January’s trading update. Management said strong first half momentum had continued into the third quarter, with Nuclear growing well on the back of new build clean energy projects and submarine support work. Aviation also remained strong, supported by the ongoing ramp up of the French Mentor 2 contract, while Marine benefited from higher LGE volumes and growth in the Skynet programme.

That mix matters. Investors often lump defence names together, but Babcock is not simply an arms exporter or a pure weapons platform company. It sits in the maintenance, support, training and strategic infrastructure parts of the chain, which can often offer better visibility and lower earnings volatility than the more headline-driven parts of the sector.

January’s update quietly strengthened the case

The most encouraging part of the January update was not a flashy contract win, though there were plenty of those. It was the confidence behind the language.

Management said the group remained on track to meet board expectations for FY26, including hitting the 8% margin target, with upside possible if the Indonesian Arrowhead licences are delivered in year. That is exactly the sort of sentence long-term investors like to hear. It suggests momentum is intact, guidance is grounded, and optionality still exists.

There was also no shortage of strategic progress. The Indonesian Maritime Partnership Programme is potentially significant, with Babcock selected as prime industrial partner on a £4bn programme and signing a Letter of Intent covering the aims of the wider initiative. The Arrowhead programme also continues to move forward, with milestones reached on Type 31 and further international naval discussions ongoing. Elsewhere, the company expanded its strategic partnership with HII to support the US Virginia Class submarine programme in Rosyth, which reinforces Babcock’s position within the broader AUKUS ecosystem.

Taken together, this is not a company waiting for the defence cycle to improve. It is already participating in it.

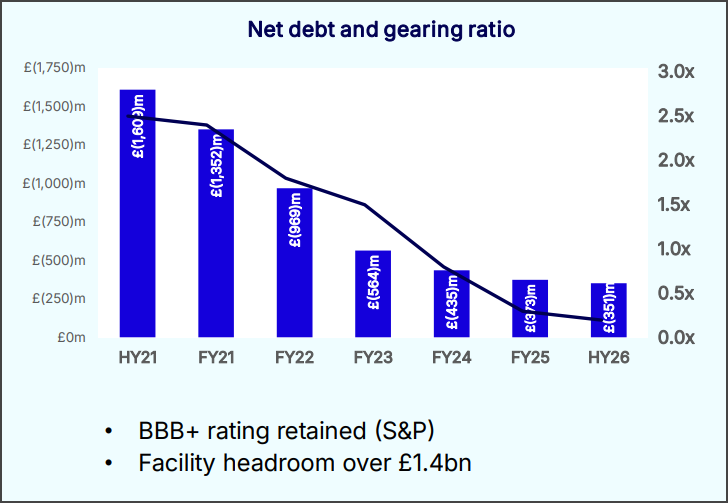

Capital allocation has improved too

One of the more attractive shifts in the Babcock story has been the improvement in capital discipline.

Net debt has fallen to £364m, down substantially from the levels seen in prior years, while free cash flow per share has improved to 41.1p. The business is also returning capital, with the £200m share buyback announced in Q2 already £90m complete by the January update, and still expected to finish around the March year end. The chart (right) is taken from the November half year results and differs to the Jan update but it clearly illustrates the bigger picture trend.

That is not the behaviour of a business still stuck in survival mode. It is the behaviour of a management team that believes the heavy lifting has largely been done and shareholder returns can now play a bigger role in the investment case.

The dividend is still modest at a forward yield of around 0.9%, so this is not an income story. But it does reinforce the idea that Babcock has moved from repair mode to controlled growth mode.

The chart says pause, not peak

The technical picture also looks more constructive than it did a few weeks ago. After a powerful move into January, the shares pulled back and have spent the past several weeks consolidating rather than collapsing. That is an important distinction.

The stock remains comfortably above its 200-day moving average, which continues to slope higher, while the recent consolidation has helped cool the excess without doing any real structural damage. Price is sitting just below the 50-day moving average, which suggests short-term momentum has softened, but the broader trend remains intact.

Put simply, this does not look like a chart that has topped out. It looks like a chart that has paused after a strong run and is trying to decide whether the next leg higher can begin. For a stock with improving fundamentals, that is a far healthier setup than a vertical breakout into fresh highs.

Why revisit it now

The obvious bear case is valuation. At around 22x forward earnings, Babcock is no longer a cheap turnaround. The market has recognised the progress, and some of the rerating has already happened.

That is true. But valuation needs to be weighed against direction of travel. Earnings are still forecast to grow, margins are still improving, debt is still falling, and the company continues to win strategically important work in exactly the areas where Western governments are likely to keep spending. For a business that has moved from restructuring to delivery, a premium to the wider market is not hard to justify.

The bigger point is that this is no longer the old Babcock story. We already made strong money from the initial recovery. What is on offer now is something different: a higher-quality, more operationally stable business with improving visibility and a chart that suggests the market may be preparing to reward it again.

Five Key Takeaways

1. Turnaround delivered: Babcock has moved beyond recovery mode, with stronger margins, better returns and much improved earnings power.

2. Defence relevance: Exposure to naval support, nuclear infrastructure and defence training gives the group strategic importance in a tougher global backdrop.

3. Strong trading update: January’s update confirmed continued momentum into Q3 and confidence in meeting the FY26 8% margin target.

4. Balance sheet progress: Net debt has fallen to £364m, while buybacks underline growing confidence in cash generation.

5. Second chance setup: After banking a 110% profit last April, the current consolidation suggests Babcock may be offering investors a credible way back in.

BAB 3-Year Chart

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.