Regency View:

BUY AstraZeneca (AZN)

The cancer-fighting pharma with untapped potential

The last eighteen months has seen AstraZeneca (AZN) cement its position as the world leader in revolutionary cancer care…

A string of positive trial readouts for key products in breast cancer and prostate cancer has given the company an incredible oncology pipeline.

In this report, we’re going to outline why, despite being one of the FTSE 100’s top performers, AstraZeneca still look cheap.

Breast cancer drug has potential for $3bn additional sales

Anyone who has had to witness a loved one undergo chemotherapy will know that it’s a very blunt tool.

AstratZeneca is at the forefront of an exciting revolution in cancer treatments which involves engineering antibodies to fight cancer in a much more targeted and less damaging way. Its breast cancer drug, Enhertu is a shining example of this…

Enhertu, which is being jointly developed and commercialised with Japanese Company, Daiichi Sankyo has been shown to reduce the risk of disease progression by half and reduce the risk of death by a third versus chemotherapy.

The treatment is already approved as a third line of therapy for patients with later stages of the metastatic breast cancer and for a second line therapy for metastatic gastric cancer.

And there is significant hope that Enhertu’s use can be widened to treat a number of other cancers…

Enhertu targets the HER2 (human epidermal growth factor receptor 2) cancer protein. And there are many HER2 cancers, including bladder, pancreatic, ovarian and stomach cancers.

For this reason, Enhertu was granted Breakthrough Therapy Designation (BTD) in the US.

And whilst its already generating sales of $426 million (FY21), the approval for a broader range of cancer patients could be worth up to $3 billion in additional sales according to analysts at Credit Suisse.

Alexion acquisition opens new markets

In July last year, AstraZeneca completed its largest acquisition ever – the purchase of US biotech Alexion for $41bn, funded by a combination of shares and $8bn in new long-term debt.

Alexion is specialist in rare diseases and it current has a lead medicine soliris along with four other approved medicines and a pipeline of 11 molecules.

Over 7,000 rare diseases are known today, and only appox. 5% have treatments approved by the FDA. Demand in medicines for rare diseases is forecasted to grow by 11%-15% per annum over the next ten years.

AstraZeneca have used the acquisition to create a dedicated rare disease unit in Boston and management expect the deal to deliver double-digit average annual revenue growth by 2025.

Growth at a reasonable price

When it comes to analysing the merits of AstraZeneca’s valuation it has something for everyone…

The stock offers growth and momentum in the form of forecast earnings per share (ESP) growth north of 50%, a sector-leading sales CAGR of 19.2% over three years, and a share price that’s shown high levels of relative strength.

Of course, with growth and momentum comes a punchy price to earnings (PE) ratio of 16.65 (forward), but this looks reasonable given AstraZeneca’s dominant position and forecast EPS growth of 52.2%. This gives AstraZeneca a Price to Earnings Growth (PEG) ratio of 0.5 (where anything below 1 is attractive) – indicating that the shares offer growth at a reasonable price.

And for those of you after income, well AstraZeneca offer investors a forward dividend yield of 2.5% – by no means the biggest yield on the market, but a payout that is forecast to increase over the next three years.

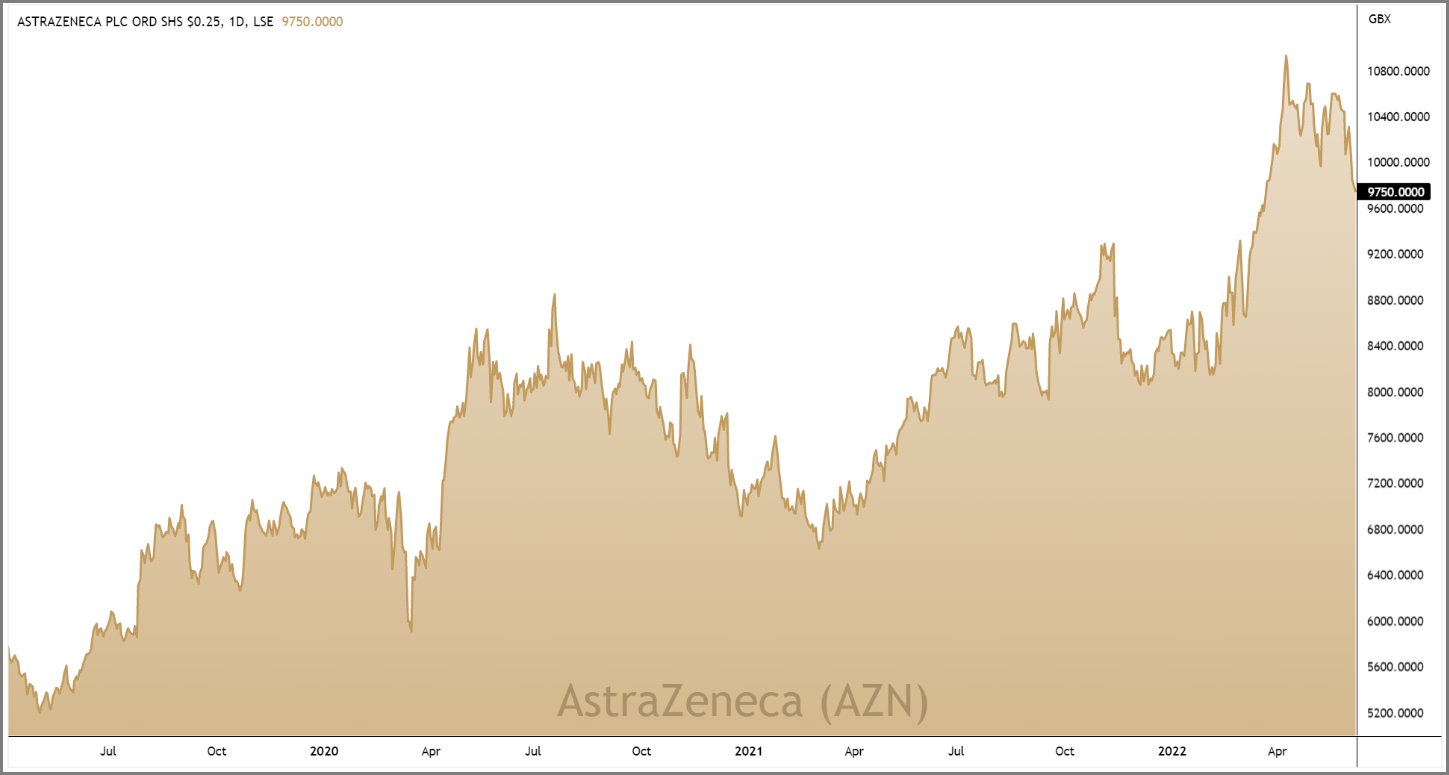

Prices pull back into broken resistance

Having been one of the FTSE 100’s standout performers in Q1, AstraZeneca’s share price has spent much of Q2 in consolidation mode…

This period of choppy mean reversion has taken the form of a small descending channel or ‘bull flag’ pattern (see chart right).

Recent price action has seen the shares move back to the bottom of the bull flag – an area that’s not too far from the November 2021 highs at 9,371p.

A characteristic for strong uptrends is for resistance to become support, and we anticipate this happening with AstraZeneca…

In fact, yesterday’s price action has formed a large bullish ‘pin-bar’ candle signalling that buyers are starting to step in and creating a short-term technical catalyst to time our entry.

AZN 3-Year Chart