19th Feb 2025. 9.00am

Regency View:

BUY 4imprint (FOUR)

- Growth

- Income

Regency View:

BUY 4imprint (FOUR)

A promotional powerhouse: Why 4imprint is ready to thrive in 2025

In a market where cash is king, 4imprint (FOUR) stands out as a business that not only generates strong free cash flow but does so with remarkable efficiency. Its direct-marketing model, built for scalability, has allowed the company to grow revenues while keeping costs firmly under control—a combination that continues to attract long-term investors.

The company’s ability to acquire and retain customers at scale, coupled with its low working capital requirements, gives it a significant advantage. And with a strong start to 2025, backed by both fundamental resilience and bullish price momentum, 4imprint is ticking all the right boxes.

Efficient, scalable, and cash-generative

4imprint has built a highly efficient, direct-marketing business model that is designed to scale quickly while keeping costs low.

The company’s ability to deliver tens of thousands of custom promotional products to millions of customers worldwide is underpinned by its proprietary order processing platform, ensuring a seamless customer experience from start to finish. This scalable model has allowed the company to keep operational costs low while generating high levels of cash flow, a key reason why 4imprint remains so attractive to long-term investors.

4imprint has a proven track record of acquiring new customers through a combination of brand marketing, search engine optimisation, and its Blue Box sample mailings. With a high proportion of repeat business and a strong customer retention rate, 4imprint is not just adding new customers but cultivating long-term relationships that drives revenue growth year after year.

The company’s low working capital requirements, due to its drop-shipping business model and credit card-based payments, further enhances its cash-generative qualities. Low inventory levels and minimal capital expenditure mean the company can reinvest its cash flow into growth initiatives, making 4imprint a prime example of a business that generates profits while minimising its capital needs.

January trading update: A strong start to 2025 backed by price momentum

4imprint’s January trading update was well received. With unaudited revenue expected to hit $1.37 billion for 2024—a 3% increase on the previous year—the company has continued its steady growth trajectory despite a challenging market environment. Profit before tax is expected to reach no less than $153 million, surpassing analyst expectations and demonstrating the strength of its business model.

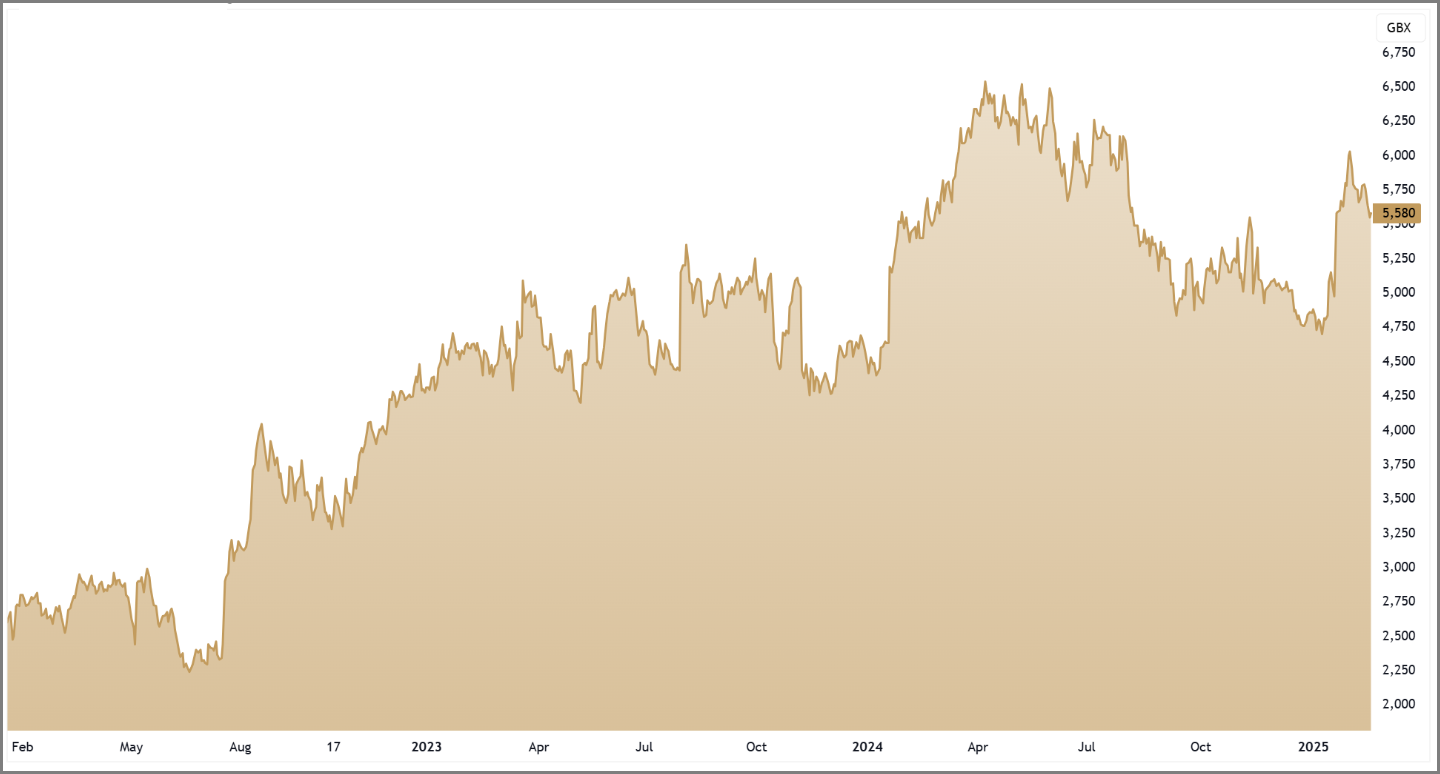

From a technical perspective, the stock is in a strong position. The share price has shown a clear breakout above its 50-day and 200-day moving averages—key technical indicators that signal the start of a new bullish phase. This move has been supported by rising average volume, which points to increased investor confidence and a growing belief in the company’s long-term prospects.

With the short-term momentum now aligning with the broader multi-year uptrend, the technical timing looks right to establish a first position in the stock.

Quality and income

When it comes to valuation, 4imprint’s financial health speaks for itself. The company’s low debt levels and significant cash position—ending 2024 with $148 million in the bank—provide the flexibility to continue investing in growth opportunities while maintaining a solid balance sheet. In a market where many companies are weighed down by debt, 4imprint’s clean financials are a major asset.

The company’s valuation is appealing, with a forward price-to-earnings ratio of 16.6 that remains reasonable given the company’s quality. Despite its strong growth track record, the stock remains well-positioned relative to its peers, and its price should continue to appreciate as the company capitalises on the strong demand for promotional products in its core markets.

Investors should also take note of the company’s attractive dividend policy. 4imprint has a clear capital allocation strategy, which prioritises shareholder returns through regular, progressive dividend payments. The current dividend yield is 3.88%, which is comfortably cover more than 1.7 x earnings. With a strong cash-generative business model, the company has the ability to continue rewarding shareholders with sustainable dividend increases while reinvesting in organic growth initiatives.

Why 4imprint is one to watch in 2025

For investors seeking a debt-free, cash-generative business with a proven track record of growth, 4imprint is an obvious choice. The company’s efficient business model, combined with its strong financial performance and technical momentum, makes it a standout choice.

As the company continues to expand its market share in the fragmented promotional products industry and reinvest in sustainable growth, we believe 4imprint is well-positioned to deliver long-term value for its shareholders.

FOUR 3-Year Chart