26th Nov 2025. 8.59am

Regency View:

BUY 4imprint FOUR Second Tranche

- Growth

- Income

Regency View:

BUY 4imprint FOUR Second Tranche

4imprint: A welcome return to form

Earnings season always gives us a chance to reassess stories and spot new catalysts that can shift a trend. 4imprint (FOUR) has just delivered exactly that. We first added the shares earlier in the year, and although the position has been under pressure, the latest trading statement is the clearest sign yet that the long-term investment case remains firmly intact. In fact, the update is strong enough to justify increasing exposure.

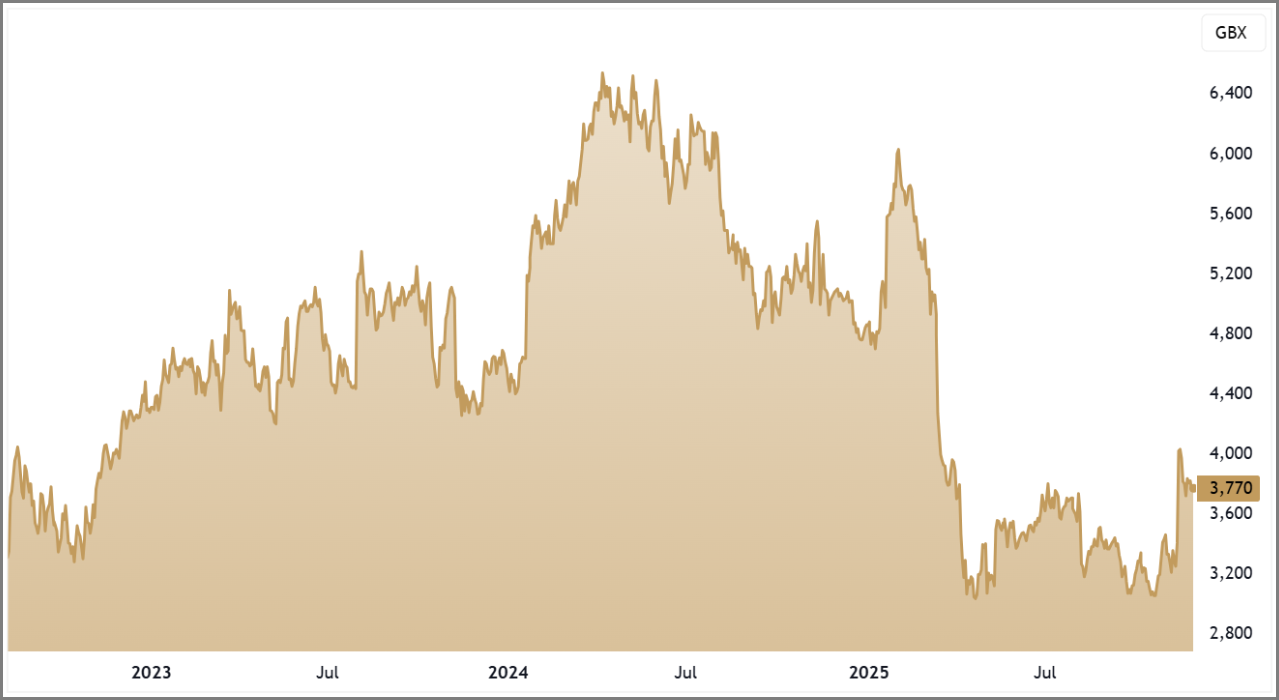

The shares gapped higher on the announcement and have been consolidating above the 200 day moving average ever since. That behaviour often marks the early stages of sentiment turning, and when you combine this with an upgrade to full year guidance, the conditions for a second tranche are now in place. FOUR has navigated a tricky year with a level of resilience that the market had not priced in, which gives us a timely opportunity to act.

A quiet compounder with real financial muscle

FOUR sits in a part of the market that rarely attracts headlines, yet its business model is exactly the kind of steady, cash-generative engine we like to back. It supplies branded promotional products to a huge base of North American businesses, operating a direct marketing model that prioritises retention, repeat orders, and reliable service. It is not glamorous, but it is exceptionally well run, and this is reflected in some of the most impressive profitability metrics of any UK-listed mid cap.

Returns on capital routinely exceed 100%. Operating margins sit in the low double digits. Free cash flow is consistently strong. And the balance sheet carries meaningful net cash. This combination of high returns and low capital intensity is rare, and it has allowed FOUR to compound earnings at a rate far above the wider sector over the past decade.

The revenue profile shows a story of long-term expansion with occasional slowdowns rather than structural weakness. Even with macro uncertainty and softer demand from new customers, the business has kept average order values stable and maintained retention rates that most consumer-facing companies would envy. When you can preserve the core engine during a tougher backdrop, the recovery in top line growth tends to follow.

A trading update that alters the narrative

The latest update was far better than expected. Management now guides full year revenue towards the top of the analyst range and profit before tax above the upper end of the range. That is a material shift for a business that had spent most of this year being priced for disappointment.

In the first 10 months of the year, revenue tracked only slightly behind the prior period, order values held steady, and existing customer activity remained firm. New customer orders have been weaker, but this is clearly cyclical rather than structural, and the company has continued to trade resiliently through its peak seasonal months. Crucially, gross margins remain healthy, helped by a smoother than expected timing of cost increases.

The balance sheet continues to strengthen. Cash balances remain high, free cash generation is positive, and the company has approved a measured investment into consolidating office space into its expanded distribution centre. This signals ongoing confidence without stretching the financials. When management reaffirm their belief in the business through disciplined capital allocation, markets usually follow.

Valuation and technicals align at the right moment

The valuation now looks very reasonable for a company with this level of quality. Forward earnings are priced at a modest multiple, free cash flow is still growing over the longer term, and the dividend yield is comfortably covered. None of this was being recognised by the market a few months ago, but the earnings beat has reset expectations.

Technically, the gap higher on the trading statement was important. Weak stocks do not jump through the 200 day moving average and then hold the level. Price action has now consolidated above it, forming a tight base that suggests accumulation rather than distribution. This is often the market’s way of saying that the worst of the derating has passed.

We have seen this pattern before in FTSE names that quietly compound in the background. A period of softer sentiment leads to an exaggerated sell off, earnings hold up better than feared, the business upgrades guidance, and the share price stabilises and begins to rebuild. FOUR is ticking each stage of that pattern.

Second tranche buy

We are increasing our position in FOUR. The core business remains strong, the latest trading statement exceeded expectations, and the technical backdrop has turned constructive at the exact moment fundamentals have improved. This is the kind of asymmetry we aim to capture in FTSE Investor: a high-quality company regaining momentum while still trading at a valuation that underestimates its long-term earning power.

FOUR continues to demonstrate the resilience and discipline that long-term compounding stories are built on. This second tranche strengthens our exposure at a moment when the evidence is turning back in our favour.

Five Key Takeaways:

1. Earnings upgrade: Full year revenue and profit now guided above analyst expectations.

2. Margin resilience: Gross margin remains strong and operating margins stay in double digits.

3. Cash strength: High cash balance and ongoing free cash generation support long-term growth.

4. Technical shift: Shares gapped above the 200 day moving average and are consolidating firmly.

5. Second tranche case: Valuation, fundamentals and sentiment now aligned in our favour.

FOUR 3-Year Chart