Regency View:

Update

Alpha trading ‘significantly ahead’ expectations

Alpha Financial Markets Consulting (AFM) delivered a very strong trading update last week in which it said it now expects to report full year FY23 results “significantly ahead of current market expectations”.

Alpha expect to deliver strong double-digit organic net fee income growth compared to the prior year. This has been driven by “positive trading conditions in the second half of the year and ongoing client demand”.

Alpha’s bullish update highlighted the “particularly good progress” made in North America with Lionpoint trading strongly.

Euan Fraser, Alpha’s CEO commented:

“We end FY23 significantly ahead of expectations and with a strong balance sheet. We remain mindful of the inflationary backdrop and geopolitical uncertainties and remain positive that the underlying industry trends and our market leading reputation will continue to drive demand globally for our services”.

The market’s reaction to the numbers has been bullish but tempered by the wider sell-off in financial stocks following the collapse of Silicon Valley Bank (SVB).

AFM Daily Candle Chart

Craneware says US healthcare market continues to face challenges

Craneware’s (CRW) share price continued its recent slide after the publication of a cautious set of Interim Results…

The US-focused financial software provider to the healthcare market expects first-half revenues to increase by roughly 6% to $84.7m, and underlying profits to grow by 8% to $25.5m.

Craneware CEO, Keith Nelson said the numbers were “robust” but that its client base, US healthcare providers, continue to face many “post-pandemic challenges” and are struggling to cope with inflationary pressures.

The business continues to have strong financials with annual recurring revenue topping $166m and cash reserves of $38.6m.

For this reason, we can afford to be patient and wait for the US market to recover with Craneware stating they have the “building blocks in place for growth acceleration as the current pressures within the US healthcare market abate”.

CRW Daily Candle Chart

Enwell wins VAS field legal battle

Ukrainian oil and gas producer, Enwell Energy (ENW) announced earlier this month that its legal challenge to a suspension of its VAS field has been successful.

In 2019, the State Service of Geology and Subsoil of Ukraine published an order for suspension dated in respect of Enwell’s production licence for the VAS field.

Enwell took the legal battel all the way to the Supreme Court of Ukraine which determined that the order was not justified and should be cancelled.

“The Supreme Court is the final appellate court in the legal proceedings and therefore this decision is final” said Enwell.

The news has boosted Enwell’s share price which has been steadily climbing since the turn of the year.

Our position remains under active review and we will keep our clients informed of any changes.

ENW Daily Candle Chart

Keywords Studios hikes dividend by 10%

Gaming services provider, Keywords Studios (KWS) hiked its dividend by 10% and said trading in 2023 has started well.

In a solid set of Final Results, released this week, Keywords said the business was well-positioned to increase market share and navigate volatility.

Keywords reported revenue for the calendar year of €690.7m, up 35% on the previous year, and adjusted profit before tax jumped 30% to €112m.

A final dividend per share of 1.60p was declared, up from 1.45p last time, bringing the total dividend for 2022 to 2.37p compared to 2.15p.

Bertrand Bodson, Keywords CEO commented:

“We expect to continue to see robust demand for content generation as our clients seek to capture the imagination of the three billion gamers globally”.

“We continue to have a healthy pipeline of acquisition opportunities to broaden our capabilities, geographic footprint and service offerings. This, together with our organic growth, will enable us to continue to grow market share, and build upon our position as the partner of choice for the global video games industry, and beyond” he added.

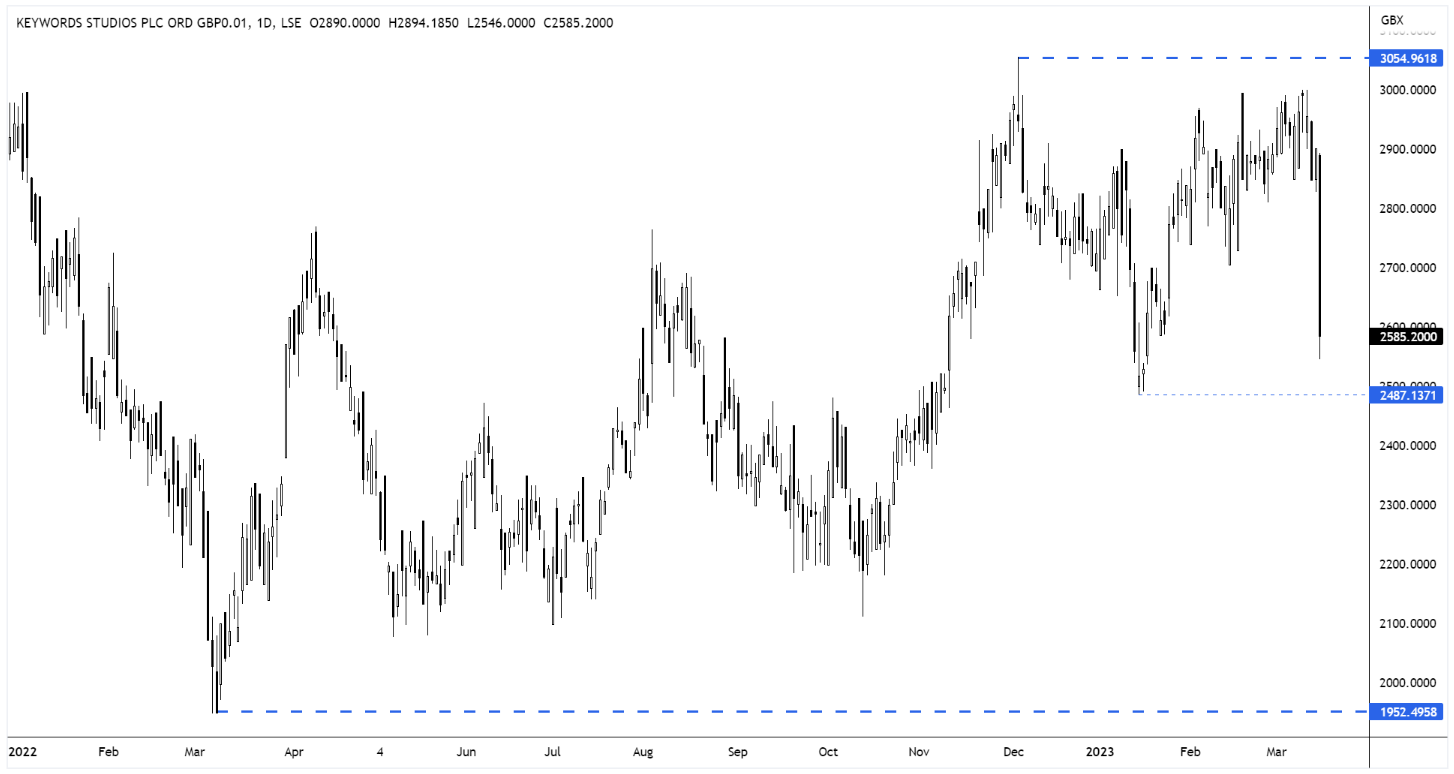

KWS Daily Candle Chart

Midwich tops £1bn revenue on 40% sales growth

Midwich (MIDW) delivered record full-year sales of £1.2bn with sales growth of 40.7%.

“We’ve had an exceptional year and one of our best organic growth years that I can remember” said Midwich CEO Stephen Fenby.

“You can’t grow at 40% forever but we’ve got ambitious plans for the future. We’d like to keep growing at a good rate, so long as it’s the right sort of growth, the right sort of products and markets, and we can be profitable at it and offer a good service” he added.

The international audio-visual (AV) distributor has seen strong growth in the US, expanding by 60% in constant currency terms, compared with 14% to 18% in other territories.

“The Starin business in the US is a good-sized business for us. It accounted for about 10% of our turnover last year” said Fenby.

Adjusted profit before tax grew 42% to £45.2m and net debt to adjusted earnings reduced to 1.6 time – back within its target range.

A final dividend of 10.5p has been proposed – bringing the full year dividend to 15p, up from 11.1p last year.

On the price chart, the shares have ebbed lower after a strong rally at the turn of the year. However, we expect 431p to be supportive and a retest of this level may represent another buying opportunity.

MIDW Daily Candle Chart

Netcall sees ‘accelerating momentum’

Netcall (NET) delivered a strong set of Half Year results last week, with double-digit revenue and profitability growth.

The AI-driven customer engagement software provider saw revenue jump 19% to £14.7m for the six months to end December 2022.

Total annual contract value leapt 34% to £19.8m while adjusted earnings increased 29% to £4.4m with profit before tax doubling to £2.4m.

Growth has been driven by advanced cloud services, with revenue surging 58% to £17.1m.

Netcall CEO, Henrik Bang said:

“We enter the second half in a good position with a healthy pipeline and a profitable and cash generative business, which combined with our strong balance sheet, enables us to continue investing in our growth strategy. The Board remains confident in the Group’s continued success.”

It’s early days for our Netcall position and with these strong Half-Year results behind them, we expect the stock to perform well for us this year.

NET Daily Candle Chart

Tremor deny the sale rumours

Smart TV advertising group, Tremor International (TRMR) denied that it was currently in talks to sell the business.

Addressing recent speculation, Tremor confirmed it is in discussions with Goldman Sachs as an ongoing financial adviser but “is not currently in a sale process.”

“From time to time, the company receives inquiries, and the board evaluates such inquiries, as applicable, together with its financial advisor,” Tremor said in a statement.

But the company added that it “continues to believe in the stand-alone prospects of the business, and also recognizes its fiduciary duties to its shareholders.”

The statement follows a disappointing trading update earlier in the month which saw annual profit and revenue fall, despite an increase in revenue in the last quarter of 2022.

Tremors annual revenue also fell to $335.3m from $341.9m, while operating costs increased to $229.8m from $195.8m in 2021.

The stock has mirrored the wider underperformance of the US advertising industry and prices are trading back at levels not seen since 2020.

TRMR Daily Candle Chart

Yu Group falls despite ‘record breaking’ financial performance

Managing the market’s expectations is more art than science, and Yu Group (YU) CEO Bobby Kalar is learning this the hard way.

He has been very quick to hype up Yu Group’s stellar performance this year, but this has caused expectations to run ahead of themselves…

Revenue increased 79% to £278.6m and adjusted earnings more than tripled to £7.9m. Cash generation was very strong and Yu reinstated its final dividend with a 3p per share payout.

Chief Executive Officer Bobby Kalar said:

“Our record-breaking financial performance and significant strategic progress is a testament to the strength of the group”.

“We have got off to a fantastic start in 2023 with our exceptional performance continuing. Whilst we remain vigilant, we look forward to delivering continued shareholder value in 2023 and beyond.”

Despite the excellent numbers, Yu’s share price has dropped sharply this week – indicating that the market was expecting more.

Mr Kalar will need to do a better job at managing expectations if he is to avoid the share price volatility that we’ve seen this week.

YU. Daily Candle Chart

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.