29th Jan 2026. 9.08am

Regency View:

Netcall (NET) Second Tranche

Regency View:

Netcall (NET) Second Tranche

Netcall: Adding exposure as the evidence builds

One of the advantages of following AIM closely over long periods is that you begin to recognise the businesses that simply keep turning up and doing the work. They don’t shout, they don’t promise the earth, and they rarely dominate the headlines. But quarter after quarter, year after year, the progress is there if you’re paying attention.

Netcall (NET) is one of those businesses. We first highlighted the shares back in 2023 and that initial tranche is now up around 30%. For newer clients, this is not a recent discovery or a turnaround play. It’s a company we’ve watched mature steadily, and recent developments give us enough confidence to increase our exposure rather than just admire the progress from the sidelines.

Software that sits at the centre of the organisation

At its core, Netcall builds enterprise software designed to make large organisations run more smoothly. Its Liberty platform helps automate workflows, manage cases and improve how businesses interact with customers and citizens. Think financial services firms handling complex cases, councils managing high volumes of requests, or healthcare providers trying to reduce administrative friction.

Once Liberty is embedded, it becomes part of the plumbing. These systems are not easily swapped out, and customers tend to expand usage over time rather than churn away. That stickiness is what separates a decent software business from a genuinely durable one.

Revenue is generated largely through recurring cloud subscriptions, supported by implementation and services. Over recent years, management has been deliberately shifting the mix toward cloud, improving both visibility and margins. It’s not flashy, but it’s exactly how you build a high-quality software model.

The cloud engine is doing the heavy lifting

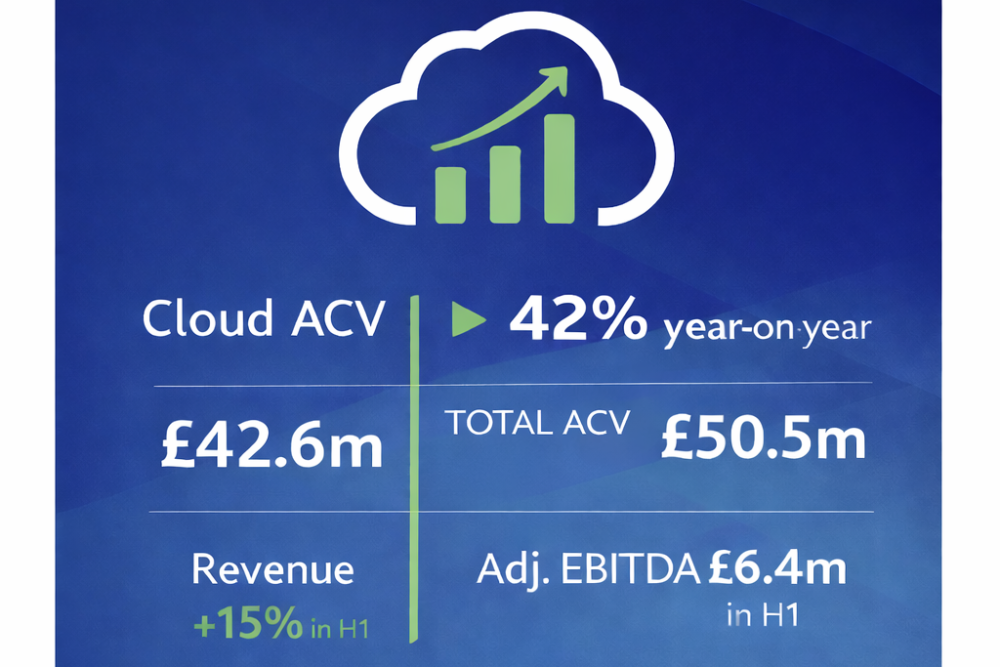

The latest trading update confirmed that this strategy is paying off. Cloud demand continues to drive growth, with customers not only signing up but increasing the scope of what they use. Annual Contract Value from cloud services rose sharply again, pushing total ACV beyond the £50m mark.

That’s an important milestone. ACV tells us what has already been sold and contracted, not what management hopes to win next. It brings a level of predictability that AIM investors don’t always get.

The pattern is consistent. New customers are coming on board, average deal sizes are rising, and existing clients are adding additional modules, including Liberty’s AI capabilities. This is the kind of compounding you want to see. Growth layered on top of growth, rather than growth constantly having to start from scratch.

Execution that shows up where it matters

Alongside the operational momentum, the financial delivery remains reassuringly solid. For the first half of the year, revenue is expected to be up 15%, with EBITDA growing at a double-digit rate as well. That’s notable given the heavy cloud investment programme completed previously. The benefits are now flowing through, rather than costs continuing to rise.

Netcall also remains debt-free, even after completing the acquisition of Jadu in December. Cash levels dipped as expected due to acquisition payments, but the balance sheet remains in good shape and gives management flexibility rather than constraints.

The recent £3m multi-year Liberty Cloud contract with a global financial services group adds another layer of comfort. It deepens an existing relationship, increases annual subscription value and reinforces the land-and-expand strategy. These are the kinds of wins that quietly improve the quality of future revenues.

Price action still telling the right story

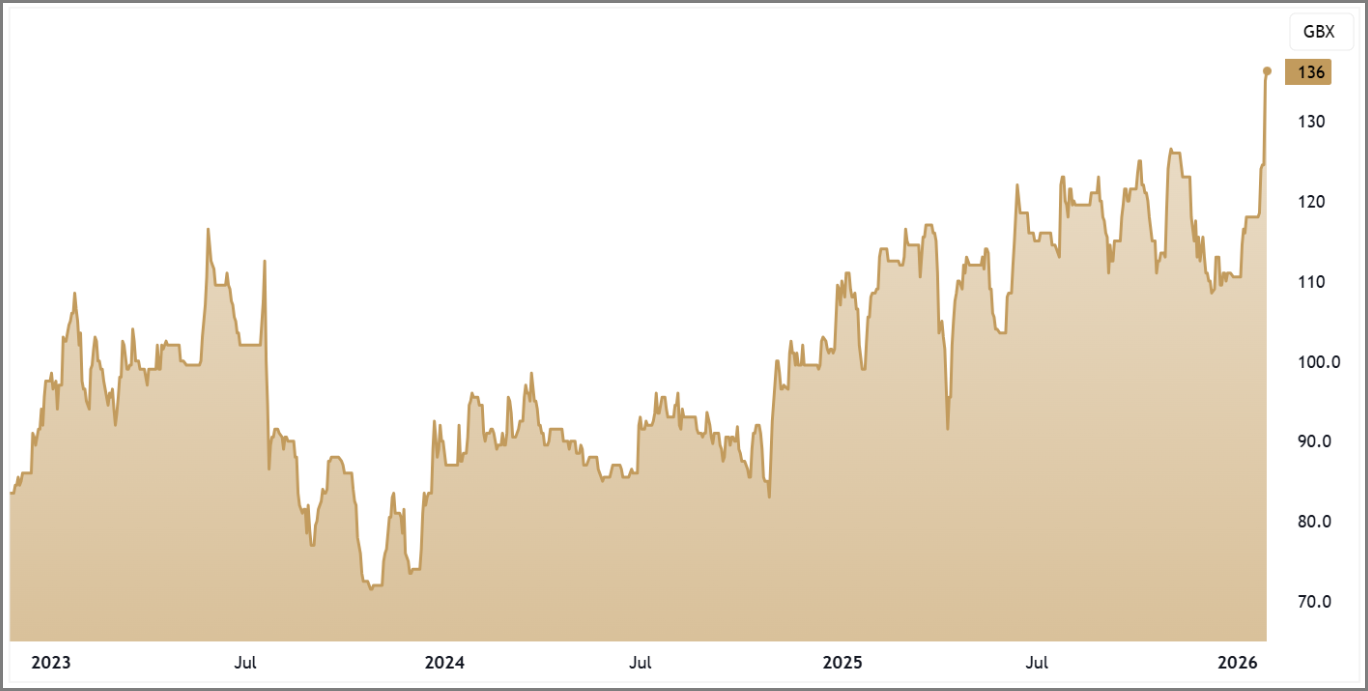

Technically, the shares continue to do what strong trends tend to do. Over the past year, price has formed a clear uptrend, repeatedly finding support along the rising 200-day moving average. Pullbacks have been absorbed rather than accelerated.

Since last week’s trading update, buying interest has increased, supported by healthier volumes. That suggests conviction rather than speculation. We’re not trying to fine-tune short-term moves, but the broader structure remains constructive and supportive of adding exposure.

NET Daily Candle Chart

Why we’re comfortable adding here

Netcall is no longer a hidden micro-cap, but it also doesn’t feel fully priced for what it’s becoming. Forecast growth remains attractive, supported by recurring revenues and improving operating leverage. The valuation reflects a business that is scaling sensibly, not one that has already peaked.

Crucially, on the price chart there’s been progress, but not excess. That matters. We’d much rather add to a position where the market is steadily recognising improvement than chase something that has already run far ahead of the fundamentals.

This is not about chasing momentum or reacting to a single announcement. It’s about recognising that a good business is continuing to get better, and adjusting our exposure accordingly.

Five Key Takeaways

1. Proven compounder: Netcall has delivered steady growth over multiple years, building value well beyond short-term market noise.

2. Cloud-led momentum: The shift to Cloud subscriptions and AI is accelerating recurring revenues and improving visibility.

3. Land and expand: Blue-chip customers are deepening usage over time, lifting contract values and stickiness.

4. Balance sheet strength: A debt-free position provides flexibility to invest, acquire and compound without strain.

5. Trend intact: The shares remain in a clear long-term uptrend, with recent news reinforcing positive momentum.

NET 3-Year Chart

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.