15th Jan 2026. 9.00am

Regency View:

BUY MTI Wireless Edge (MWE)

Regency View:

MTI Wireless Edge (MWE)

MTI Wireless Edge: Strong signal, steady execution

Over the last seven years of monitoring the AIM market, MTI Wireless Edge (MWE) has consistently appeared on our quality screens. That alone places it in a relatively small group. AIM offers no shortage of exciting narratives, but far fewer businesses demonstrate the ability to execute steadily across multiple market cycles. MTI has done exactly that, quietly building a track record that speaks for itself.

It is also a company we have highlighted on multiple occasions over the years, including periods where strong share price performance allowed profits to be taken. That history matters. Longevity, repeatability and resilience are often the most underappreciated quality signals in small caps, yet they tend to be the foundations of long term compounding. MTI feels like one of those businesses that keeps showing up, year after year, doing the work.

Three engines, one cohesive strategy

MTI operates across three divisions that at first glance appear diverse, but in practice fit together well. Antennas, water management solutions and defence focused design services all sit under the same umbrella of radio frequency expertise and mission critical infrastructure.

The antenna division remains the backbone of the group and has increasingly benefited from rising global defence spending. Military and secure communication systems are becoming more complex, more electronic and more specialised. MTI’s products sit directly in that value chain, supplying components that are essential rather than discretionary.

Alongside this, the Mottech water management business continues to benefit from structural demand. Water scarcity, infrastructure efficiency and regulatory pressure are driving adoption across both government and commercial markets. Orders from Israel, the Gulf States, Italy and the US highlight the international reach of this division and reduce reliance on any single geography.

MTI Summit, the group’s defence focused design subsidiary, has also returned to form. After a period of underperformance, the division delivered a profitable third quarter and now carries a healthy pipeline of new opportunities. Importantly, these are not one off wins but design led projects that often lead to repeat business and long term relationships.

Execution showing up in the numbers

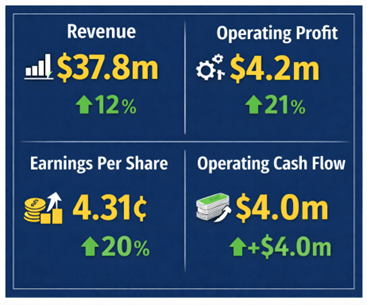

The November update confirmed that operational momentum is translating into tangible financial progress. For the nine months to September 2025, revenue rose 12% to $37.8m, while operating profit increased 21% to $4.2m. Earnings per share climbed 20% to 4.31 US cents, reflecting both revenue growth and disciplined cost control.

What stands out is the quality of that growth. It has been driven by demand across all three divisions rather than a single standout contract. Defence now accounts for around 48% of group revenue, but this is balanced by exposure to infrastructure and water management, reducing cyclicality.

Cash generation was particularly encouraging. Net cash from operating activities reached $4.0m for the period, comfortably ahead of the full year figure delivered in 2024. As a result, net cash increased to $6.4m by the end of September, reinforcing the strength of the balance sheet.

Balance sheet strength and capital discipline

MTI’s conservative financial approach continues to set it apart within the AIM universe. The group operates with net cash, modest capital expenditure requirements and a clear focus on cash conversion. That combination provides resilience during softer periods and optionality when opportunities arise.

Management has also remained disciplined on capital allocation. Rather than chasing aggressive expansion, the focus has been on incremental growth, operational efficiency and returning capital to shareholders when appropriate. The expectation of a progressive final dividend alongside the full year results reflects confidence that current cash flows are sustainable rather than temporary.

In a market where dividends are often the first casualty of uncertainty, MTI’s consistency in this area deserves recognition.

Order backlog and visibility

Another encouraging feature of the recent update was commentary around the order backlog. The group enters the final quarter of FY2025 with a robust pipeline, supported by ongoing tenders across defence, communications and infrastructure.

While timing of contract awards can always vary, the breadth of opportunities suggests that momentum is not reliant on a single outcome. This provides a level of visibility that is relatively rare among smaller AIM listed companies and helps smooth earnings through the year.

Looking further ahead, management expects demand to remain supported by three long term drivers: defence modernisation, continued rollout of 5G infrastructure and growing investment in water efficiency. These are not short lived themes.

Technical view: Subtle but encouraging signals

From a technical perspective, the share price has not been chasing momentum headlines over the past year, but recent price action has started to improve. The response to November’s trading update was bullish, with the shares moving decisively above both the 50 day and 200 day simple moving averages.

Since then, prices have pulled back into that moving average cluster before pushing higher again, forming a higher swing low. This type of structure often reflects improving sentiment rather than speculative excess. For a small cap with solid fundamentals, that is usually how more sustainable trends begin.

It is important not to overanalyse short term price action in smaller stocks, but taken in context, the technical picture aligns well with the underlying operational progress.

Why MTI continues to stand out

MTI Wireless Edge is not a business built on bold promises or transformational one off events. Instead, it has steadily compounded through operational delivery, conservative financial management and exposure to long term structural demand.

In an AIM market that can often reward noise over consistency, MTI remains a reminder that doing the basics well, year after year, still matters. For investors looking for quality, resilience and steady execution we believe this is a stock that continues to earn its place in your small cap portfolio.

Five key takeaways

1. Proven operator: MTI has appeared on quality screens for years, reflecting a business that delivers across cycles.

2. Multiple growth drivers: Defence, 5G infrastructure and water management provide diversified and durable demand.

3. Cash-led model: Strong cash generation and a net cash balance underpin balance sheet resilience.

4. Disciplined execution: Revenue growth is translating into higher profits without stretching the business.

5. Early technical improvement: Recent price structure suggests momentum is beginning to rebuild.

MWE 3-Year Chart

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.