19th Jun 2025. 9.01am

Regency View:

BUY Tristel (TSTL)

Regency View:

BUY Tristel (TSTL)

Tristel: A clean opportunity for growth and income

In a market often obsessed with flashy tech and overleveraged turnarounds, there’s something refreshingly straightforward about Tristel (TSTL).

It makes products that kill bugs quickly, safely, and effectively. That simple formula turned Tristel into one of the market’s pandemic darlings. Its hospital-grade disinfectants were essential in preventing the spread of COVID-19, and the shares more than doubled between 2020 and 2021.

But with the pandemic in the rear-view mirror and investor attention elsewhere, the dust has long since settled. Tristel is no longer a ‘hot stock’ and that’s exactly what makes it interesting. The shares are now trading 46% below their pandemic peak, having hammered out a long-term support base around 280p. The hype may have faded, but the fundamentals have only improved.

Between strong cash generation, expanding US traction, and a dividend policy that keeps shareholders smiling, Tristel is quietly building a case as one of the UK market’s most compelling income-and-growth plays. With the shares still down 19% over the past year, now looks like an opportune time to take a fresh look.

Infection control is non-discretionary

Tristel’s entire business rests on a simple but defensible idea: infection prevention is essential. Whether you’re scanning for early-stage cancer or performing a routine ultrasound, the one thing hospitals can’t afford is cross-contamination. Tristel’s chlorine dioxide chemistry, delivered in wipes, foams, and portable kits, has become a go-to alternative to legacy disinfection methods like soaking or expensive, slow-to-operate machines.

Its appeal? Speed, portability, and effectiveness. While traditional solutions require 10–20 minutes and dedicated equipment, Tristel’s products disinfect at the point of care within two minutes and without infrastructure. That’s not just a convenience; it’s a clinical and economic advantage. And it’s why Tristel has built partnerships with hospitals across Europe, Asia, and now North America.

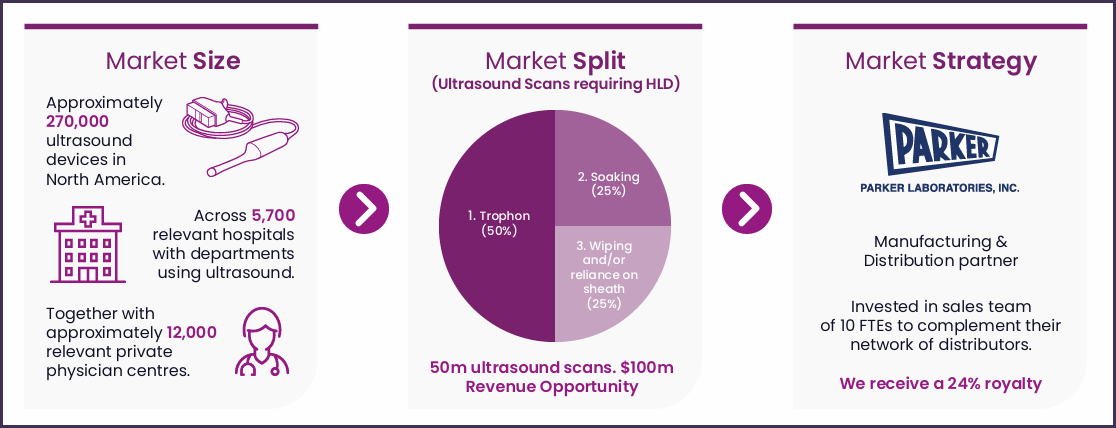

The growth engine: US expansion begins

Cracking the US healthcare market is the kind of “if they can pull it off” story that normally comes with risk and dilution. But Tristel has already secured FDA clearance for two key products, ULT and OPH, and they’re being rolled out with the help of a distribution partner and a dedicated sales team.

The US ultrasound disinfection market alone represents a $100m revenue opportunity, with a clear need to replace outdated soaking methods and expensive capital-intensive systems like Trophon. With its wipe-based system now used in over 200,000 procedures and customer feedback glowing (“a lifesaver,” “game-changer”), Tristel is firmly on the front foot.

Ophthalmology, another overlooked but high-volume market, adds a further $32m revenue opportunity. These aren’t speculative future gains, they’re addressable markets with demand already in motion.

USA Ultrasound Opportunity

The numbers back it up

For all its niche appeal, Tristel’s financials show the hallmarks of a company with real staying power. Revenue rose 8% in H1 2025 to £22.6m, while adjusted profit before tax jumped 19% to £4.9m. Importantly, margins are expanding: EBITDA margin hit 28%, up from 26% a year earlier. The company is debt-free, sitting on £11.7m of cash, and continues to generate strong free cash flow with an 18% increase in adjusted EBITDA in just one year.

Tristel’s 10-year compound annual growth rate sits at 11%, and consensus expects a further 19.8% EPS growth in 2025. That level of consistent, profitable growth is a rarity in UK small caps especially when paired with a healthy dividend.

A dividend you can actually rely on

Income investors, take note: Tristel isn’t just throwing off dividends it’s growing them. The interim payout rose 117% this year to 5.68p, and full-year dividends are forecast to reach 14.7p for a yield of 4.2%. That’s comfortably covered by earnings, with dividend cover expected to rise to 1.11x in 2025 and improving again in 2026.

This isn’t a one-off uplift, either. Over the past five years, Tristel has delivered a 27% compound annual growth rate in dividends. In other words: consistent, compounding income fuelled by real cash flows, not financial engineering.

Valuation: Not a bargain, but not expensive either

With a forward P/E of 20.7 and EV/EBITDA of 17.5x, Tristel isn’t priced like a deep-value stock but nor should it be. This is a company with double-digit earnings growth, high returns on capital (ROCE of 19.6%), and a global rollout just getting started.

The PEG ratio of 1.07 underlines the growth-adjusted valuation still looks reasonable. And with shares up 13% in the past three months but still lagging their long-term trend, there’s momentum building without FOMO-level froth.

Why now?

Tristel’s story isn’t new but the inflection point in the US is. After years of groundwork, regulatory wins and initial traction in a $100m+ market, investors are now seeing the first wave of revenue and customer proof points. Add to that a growing dividend, margin expansion, and a defensive healthcare niche with genuine pricing power and you’ve got the ingredients for a rerating.

With the shares still trading below their long-term average valuation multiples and well under their 52-week high, the risk/reward looks attractive.

For long-term investors looking for something resilient but with income and capital growth potential, we believe Tristel now deserves a spot in their portfolio.

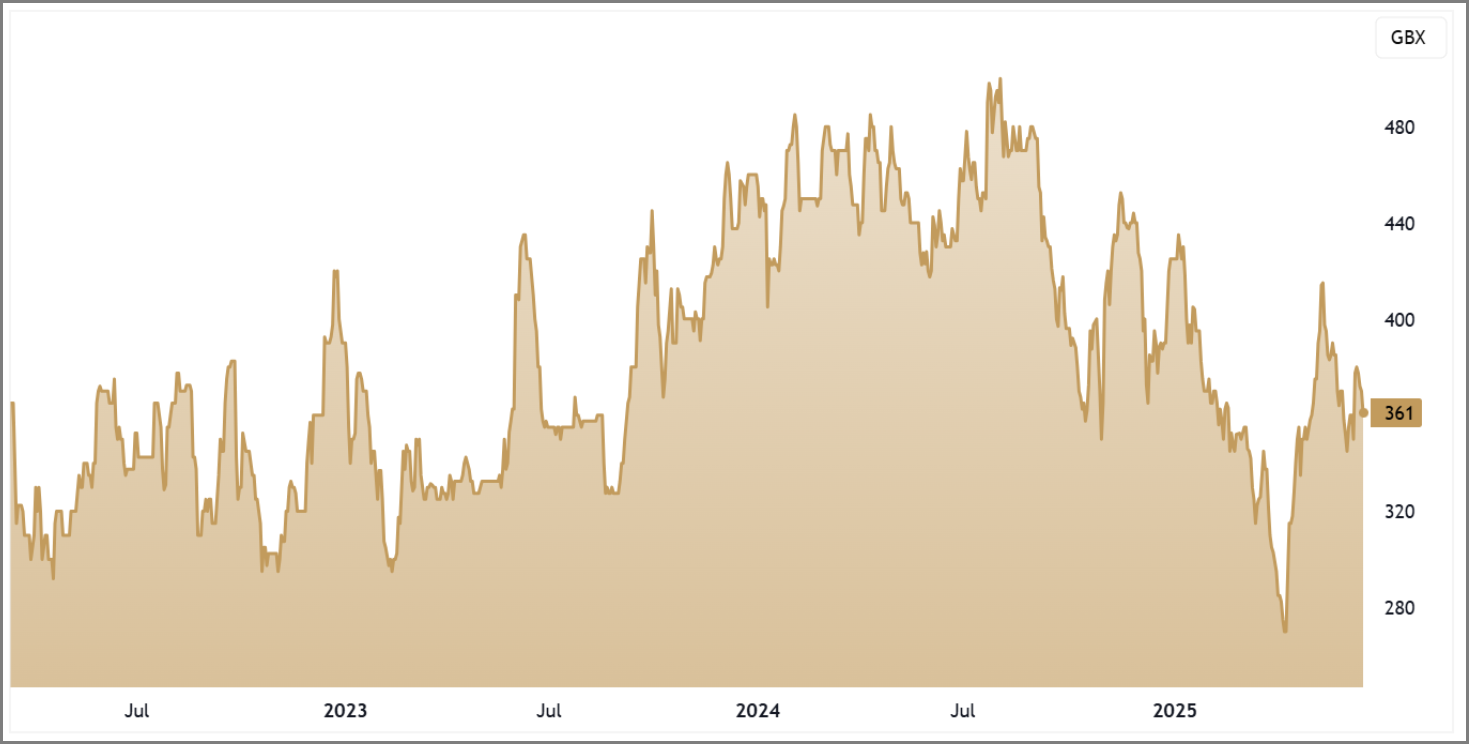

TSTL 3-Year Chart

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.