6th Nov 2025. 9.01am

Regency View:

BUY Staffline (STAF) Second Tranche

Regency View:

BUY Staffline (STAF) Second Tranche

Staffline: A recruitment revival worth reinforcing

When we first added Staffline (STAF) to our list of AIM Investor stocks back in May, it looked like a classic turnaround story gathering pace. After several difficult years of restructuring, the business had stabilised, profits were returning, and the chart hinted at a shift in sentiment. Since then, the shares have moved around 10% higher and recent interim results confirm that the recovery is far from over.

With momentum building both operationally and technically, we are taking the opportunity to increase our position with a second tranche buy.

Building a stronger, simpler business

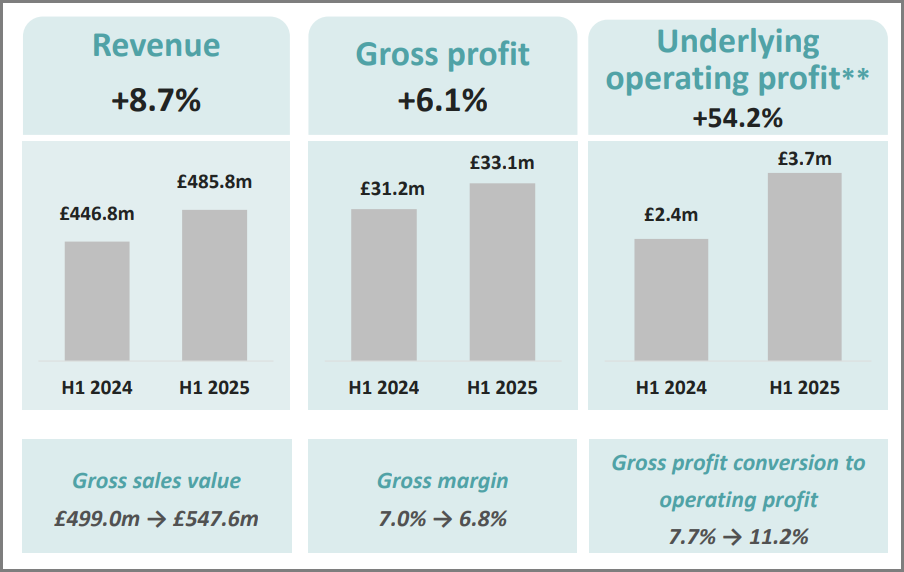

Staffline’s turnaround has been built on simplification. The disposal of its training arm, PeoplePlus, earlier this year was more than a tidy bit of portfolio housekeeping as it turned the company into a pure play recruitment specialist. That focus has already paid off. Revenue in the first half of 2025 rose 8.7% to £485.8 million while underlying operating profit jumped 54% to £3.7 million. Those numbers tell a clear story: a leaner, more efficient Staffline is delivering profitable growth even in a challenging market.

The business now operates through two divisions, Recruitment GB and Recruitment Ireland, supplying over 40,000 workers daily across industries such as food processing, logistics, and manufacturing. It is a market where scale, relationships, and reliability matter more than hype. With its nationwide reach and longstanding client base, Staffline has carved out a strong competitive advantage that few independent recruiters can match.

New contracts, new confidence

Momentum is not just financial, it is operational. The standout highlight from the interim period was a major strategic partnership with one of the UK’s leading food and drink logistics providers. This contract, which will see Staffline manage all agency labour for the client, adds around 3,000 workers across driving, warehousing, and security. It is a transformative deal that deepens Staffline’s exposure to a defensive, recurring area of the labour market.

Recruitment GB, the company’s core division, posted a 71% increase in underlying operating profit thanks to cost efficiencies and higher volumes. Temporary worker hours rose 4.4%, evidence that despite wider economic caution, essential sectors continue to rely heavily on flexible labour. Recruitment Ireland saw a dip in overall revenue due to softer public sector activity, but there was strong growth in permanent placements, particularly through the ongoing An Garda contract in the Republic of Ireland. That mix shift may temper short term numbers but positions the division well for a rebound in 2026.

A business built to withstand headwinds

Recruitment is a cyclical industry, but Staffline’s focus on blue collar sectors gives it a cushion against the slowdown in white collar hiring. Around 90% of group gross profit now comes from these defensive industries where demand is driven by logistics, food supply, and manufacturing, areas that remain active regardless of economic cycles.

The UK jobs market has cooled slightly, with vacancies dipping below pre pandemic levels, but Staffline continues to grow market share. Its ability to deliver agile workforce solutions has helped clients manage cost pressures and retain flexibility, while internally a £3 million cost reduction programme has improved margins and freed up cash. This operational discipline is the backbone of the turnaround.

Another point worth noting is the company’s balance sheet. Net debt has been reduced to £5.7 million from £9.2 million a year earlier, and management has used its improving cash position to launch a £7.5 million share buyback programme. By mid year, £4.8 million of stock had already been repurchased, signalling both confidence and a shareholder friendly capital policy. For a business that was once seen as stretched, this financial health is a refreshing change of pace.

STAF H1 2025

Valuation still on the low side

Despite the steady climb in the share price, Staffline still trades on modest valuation multiples for a company generating consistent growth. The forward price to earnings ratio sits at just 8.7, with a PEG of 0.3, suggesting the market is underestimating the pace of earnings recovery. The EV to EBITDA multiple of 2.6 further underlines the disconnect between price and fundamentals.

Free cash flow generation has improved and while the company is not paying a dividend yet, management’s buyback strategy is returning capital in a way that directly benefits shareholders. The recruitment sector often trades in boom and bust cycles, but with Staffline now more diversified, cost efficient, and debt light, it is entering the next phase from a position of strength.

Technical momentum points to more upside

On the price chart, the shares have recently been consolidating around the 50 day moving average, forming a series of lower swing highs and higher swing lows that together create a bullish flag or wedge formation. This type of compression pattern within the context of a long term uptrend signals accumulation and typically resolves higher. We view this pattern as a bullish technical catalyst for our second tranche.

Volume has eased since the initial rally, a typical consolidation phase after a strong uptrend, but the structure remains bullish. The recent buying activity from the company’s own share repurchases adds a further layer of support, showing confidence from within. Should the broader market tone stay constructive, Staffline looks well positioned for another leg higher as we move into year end.

Why we are buying more

Our first tranche back in May was about backing a turnaround that was gathering momentum. That call has worked so far, we are up around 10%, but what has changed since then is conviction. The latest results confirmed that Staffline’s transformation is not just cosmetic. It is delivering tangible growth, generating cash, and winning major contracts that provide visibility for the years ahead.

This second tranche is not about chasing a quick rebound, it is about reinforcing a position in a company that is still undervalued relative to its progress. Staffline now looks like a structurally stronger business than at any point in the past five years. With clear momentum in the numbers, supportive technicals, and disciplined management execution, it continues to tick the boxes we look for in a long term AIM recovery play.

In short, the turnaround is working, the valuation remains compelling, and the trend is still your friend. That is more than enough reason to double down.

Five Key Takeaways

1. Turnaround gaining traction – Revenue rose 8.7% and profits jumped 54% in H1 2025.

2. Operational momentum building – A new logistics contract adds 3,000 workers and expands market share.

3. Balance sheet strength returning – Net debt is down to £5.7 million with a £7.5 million buyback underway.

4. Valuation still appealing – Shares trade on a forward P/E of 8.7 and PEG of 0.3.

5. Technicals turning bullish – A flag pattern around the 50 day average points to further upside.

STAF 3-Year Chart

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.