9th Oct 2025. 9.07am

Regency View:

BUY SigmaRoc (SRC)

Regency View:

BUY SigmaRoc (SRC)

SigmaRoc: Building strength through the cycle

The materials sector has been the UK market’s standout performer over the past three months, powered by renewed investor appetite for cyclical value plays. Construction materials and industrial minerals stocks have outperformed as markets anticipate a rebound in infrastructure and manufacturing activity across Europe.

Within this momentum, SigmaRoc (SRC) stands out as a business that combines scale with discipline. The European lime and minerals group has delivered another robust set of results, growing earnings and cash flow while reducing debt in a challenging market. It remains one of the best-positioned mid-caps in the sector for investors seeking steady, long-term growth exposure to the European industrial recovery.

Building value from the ground up

SigmaRoc supply essential materials to industries ranging from construction and steel to agriculture, energy and environmental management. Lime and limestone are increasingly vital in the green transition, with growing applications in battery recycling, air pollution control and CO₂ capture.

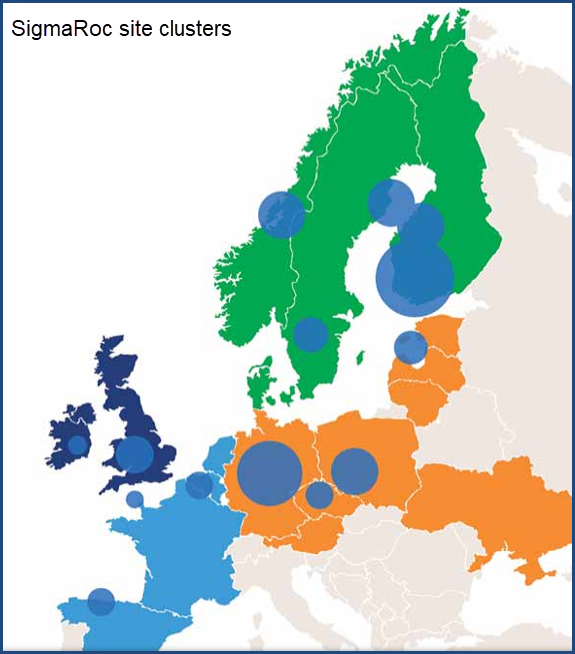

The company’s model is simple but effective. It acquires and integrates businesses in fragmented markets, extracts efficiencies through active management, and generates returns from asset-backed investments. With 2.7 billion tonnes of high-quality resources spread across Europe, SigmaRoc has the scale and stability to thrive through economic cycles. Its operations span the UK, Ireland, Western and Central Europe and the Nordics, providing both diversification and operational leverage as regional markets recover.

Operational grit and smart growth

The first half of 2025 underlined SigmaRoc’s ability to perform through softer demand. Revenue rose 13% year-on-year to £510 million, while underlying EBITDA jumped 21% to £117.8 million, pushing margins to 23.1%. This reflects strict cost control and the continued success of its synergy programme, which delivered £13 million in savings during the first half and is now forecast to exceed £21 million for the full year.

Across the group’s portfolio, regional performance has remained resilient. In the UK and Ireland, the Buxton lime acquisition drove volume and profit growth despite subdued residential construction. Central Europe offset weakness in steel and automotive demand through efficiency gains, while the Nordics maintained strong profitability even as pulp and paper volumes softened. Western Europe also saw higher margins thanks to tighter cost control and better pricing. Meanwhile, SigmaRoc’s decision to divest its French ready-mix business shows management’s commitment to focusing on higher-return assets.

Strong cash flow, lower debt and improving returns

Financially, SigmaRoc is moving from strength to strength. Free cash flow climbed 38% to £61.9 million, while covenant leverage fell to 2.0x. Cash conversion improved to 52.5%, and return on invested capital rose by 100 basis points to 5.9%. These metrics suggest SigmaRoc is converting operational performance into tangible financial strength.

The balance sheet continues to improve, with net debt now at £498 million and around £100 million of undrawn facilities. The group’s interest cover remains healthy, and the new five-year credit structure led by European banks provides flexibility for future acquisitions. At around 11x forward earnings and with forecast EPS growth of 15% per year, valuation remains modest relative to peers. While the company does not yet pay a dividend, management intends to begin distributions once leverage falls below 1.5x which is a sensible goal given its cash generation trajectory.

Innovation and long-term drivers

SigmaRoc is also investing in innovation to secure its long-term relevance. Through its SkreenHouse Ventures arm, the company is backing technologies that align with Europe’s shift towards sustainable construction. Investments in Adaptavate’s carbon-reducing wallboard and Koncrete’s digital logistics platform demonstrate its commitment to decarbonising materials supply chains while improving operational efficiency.

Structural catalysts are also taking shape. Germany’s infrastructure stimulus, expected to lift spending by around 20% from 2026, and rising European defence budgets should support demand for aggregates, lime and building materials. The eventual reconstruction of Ukraine could add another significant growth leg. SigmaRoc’s geographic positioning across northern and central Europe leaves it well placed to capture these opportunities when they materialise.

Timing the trend

SigmaRoc’s shares have carved out a strong uptrend this year, gaining nearly 50% over the past twelve months. The 50-day moving average is trending above the 200-day, confirming bullish momentum, and price has recently pulled back towards the 50-day line and key swing support. We believe the short-term timing now aligns with the long-term trend, suggesting the current consolidation could offer a favourable entry point for investors looking to position ahead of further upside.

Momentum remains supported by sector strength and solid fundamentals. As free cash flow improves and leverage declines, the backdrop for continued appreciation looks encouraging. Broker targets of around 142p imply roughly 20% upside from current levels, with potential for a sustained re-rating as the company continues to deliver operationally and as European industrial activity normalises.

SigmaRoc is achieving what most cyclical materials groups struggle to do – improving margins, expanding cash flow and reducing debt in a subdued market. With strong operational leadership, a solid asset base and clear exposure to Europe’s infrastructure and industrial recovery, the group looks set for continued progress. It is the kind of company that rewards patient investors who understand the value of consistent execution over time.

SRC 3-Year Chart

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.