25th Sep 2025. 8.58am

Regency View:

BUY Science Group (SAG) Second Tranche

Regency View:

BUY Science Group (SAG) Second Tranche

Science Group: Backing a proven performer

We first highlighted Science Group (SAG) back in 2021 and since then the shares have climbed nearly 40%. The company has quietly established itself as one of AIM’s most consistent performers, with a business model that blends high-value consultancy work with specialist engineering systems. Throw in a management team that knows how to put cash to work, and you have the recipe for a quality small cap.

Although we are presenting this as a second tranche buy, some of our newer clients may be seeing Science Group for the very first time. If that’s you, then these latest interim results provide the perfect introduction. They show a company delivering record profits, generating cash at a rapid pace, and sitting on one of the strongest balance sheets on the market.

A business built on brains and systems

Science Group is an international consultancy and systems engineering firm that applies science, technology and engineering expertise across a broad mix of industries. The Professional Services division supports clients in consumer, industrial, defence and medical sectors, helping with everything from regulatory guidance to product development. Alongside that sits two specialist systems businesses. Critical Maritime Systems & Support supplies submarine atmosphere management systems, while Frontier develops radio and audio semiconductor modules used in devices worldwide.

This combination of consultancy and systems is important. Consultancy provides recurring revenue and sticky client relationships, while the systems businesses operate in niches where demand is underpinned by long-term structural drivers. When one area softens, another often steps up. That was exactly the case in the first half of 2025. Professional Services saw some projects deferred or cancelled in the face of political and economic uncertainty, but both systems businesses delivered strong growth and rising profitability. It is this ability to balance the cycle that makes Science Group a resilient operator.

Interim results show strength beneath the surface

At the headline level, the interim results were exceptional. Profit before tax jumped to £32.2m, helped by a £24m gain on the opportunistic investment in Ricardo. That trade alone produced a return of 74% in just a few months and underlined management’s knack for spotting value.

Even without that one-off boost, underlying performance was strong. Adjusted operating profit edged up to £11.3m on revenues of £57.2m, while adjusted earnings per share rose to 19.3p from 18.1p. Operating cash flow more than doubled to £22.7m, lifting cash to £82m and net funds to £70.3m. For a company of this size, those numbers are impressive and speak to the quality of the operating model.

Smart capital allocation sets Science Group apart

What makes Science Group stand out is how carefully it uses shareholder capital. The Ricardo investment was not a lucky punt but the result of careful analysis and timing. Management had been watching Ricardo for years, spotted the mispricing after a profit warning, and moved decisively. The outcome was a rapid gain that materially strengthened the balance sheet.

Alongside these opportunistic moves, the board continues to invest in the core businesses and return capital to shareholders. Over 310,000 shares were bought back in the first half, and the programme has since been expanded. Dividends remain well covered, and the group’s £30m revolving credit facility is untouched. With so much cash on hand, the board has already hinted that further buy-backs or even a special return of capital may be on the cards if acquisition opportunities do not arise. Investors can be confident that excess funds will not sit idle.

Systems divisions firing on all cylinders

Critical Maritime Systems & Support is a market leader in submarine atmosphere management systems. Geopolitical tensions and the UK’s renewed defence commitments have reinforced the importance of this area, and CMS2 has benefited from growing demand. Revenues in the first half increased to £16.6m, with profitability boosted by new long-term support contracts. These contracts not only improve financial visibility but also strengthen relationships with clients who depend on CMS2’s technology.

Frontier, the audio and radio semiconductor specialist, has also turned a corner. Revenues climbed 20% to £7.1m, while adjusted operating profit improved to £0.9m from £0.1m a year earlier. Operational simplification in 2024 has paid off, delivering strong cash conversion and a more focused business. The upcoming Auria product line offers incremental growth potential from 2026, adding another lever for expansion. Frontier remains under strategic review, but it is clear that the division is now a valuable contributor in its own right.

Consultancy division ready for a rebound

The Professional Services business faced a trickier first half, with revenues falling to £33.2m from £36.5m as some clients cut back on projects. Despite this, margins were kept at a healthy 23.9%, showing the benefits of cost discipline and a sharper focus on high-value work. The outlook for the second half looks brighter, with customers adapting to the volatile environment and activity levels starting to recover. Over the medium term, the division’s blend of scientific expertise and regulatory knowledge should continue to provide steady growth opportunities.

Valuation and technicals add to the appeal

At 552p, the shares are only 5% below their 52-week highs. Analysts have a target of 714p, implying around 30% upside. On valuation grounds, the stock looks reasonable. A forward P/E of 14.7, an EV to EBITDA multiple of 8.3, and a price to free cash flow of 8 do not look demanding when set against a return on equity above 30%. Very few companies on AIM can boast that kind of profitability.

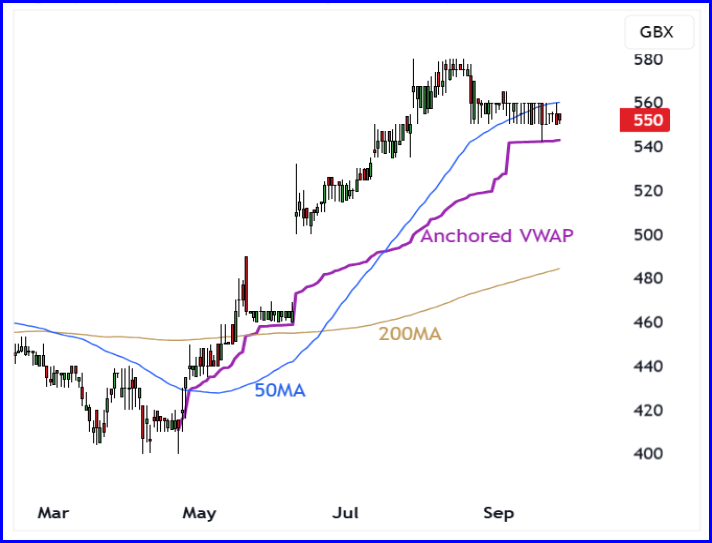

Technically, the chart is supportive. The shares are trading comfortably above their 200-day moving average, consolidating recent gains while setting up for another push higher.

The recent consolidation has seen the shares pullback to the volume-weighted average price (VWAP) anchored to the recent trend lows – this is a marker of institutional buying interest and we expect it to provide support.

Momentum is firmly behind the stock, and with Science Group qualifying for multiple quality, value and momentum screens, there is every chance the re-rating continues. For longer-term investors, we believe this is the type of AIM stock worth building a position in. Whether you joined us back in 2021 or are seeing Science Group for the first time today, Science Group is a small cap with exciting potential.

SAG 3-Year Chart

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.