30th Jan 2025. 9.05am

Regency View:

BUY Renold (RNO) Second Tranche

Regency View:

BUY Renold (RNO) Second Tranche

Renold: Strength in motion – A second tranche buy

When we first highlighted Renold (RNO) in September, the stock was quietly making strides, backed by strong cash flow, improving margins, and a well-managed order book.

Now, with the shares starting to break out of a long-term wedge consolidation pattern, operational improvements continuing to deliver results and the valuation still looking attractive, we’re adding a second tranche.

A business built on resilience

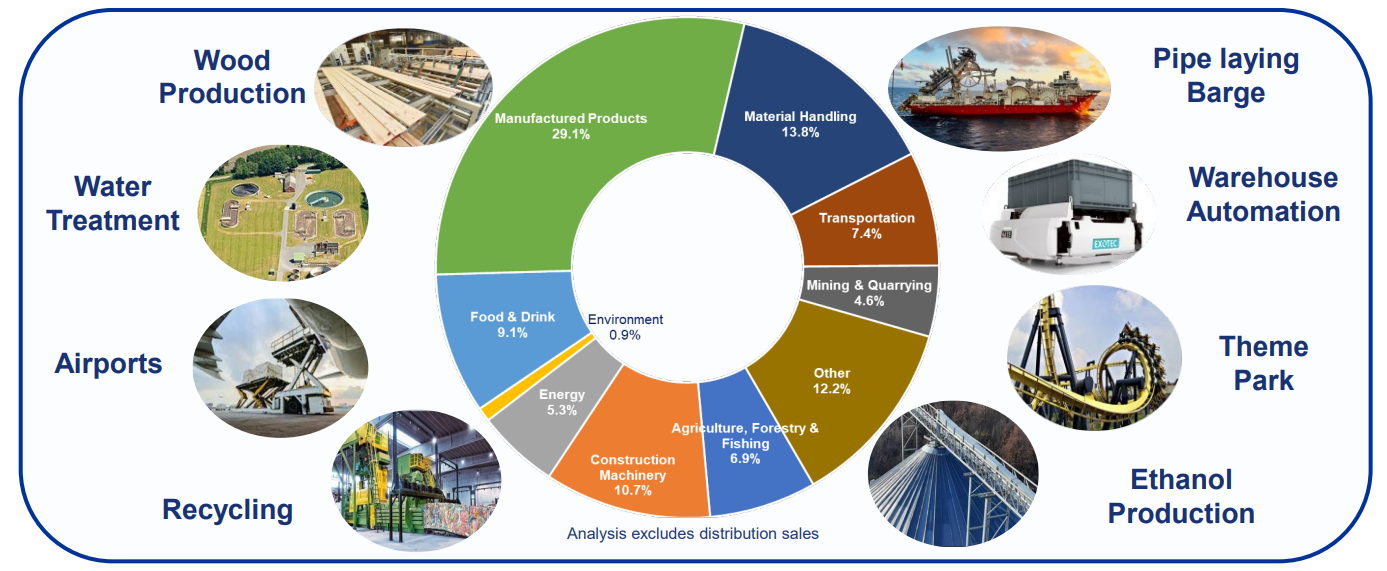

Renold isn’t a household name, but its products keep the world moving. The company is a global leader in industrial chains and power transmission systems, supplying essential components to industries ranging from mining and infrastructure to food production and material handling. These are businesses that demand reliability, and Renold has built a reputation as a trusted supplier, with operations spanning 20 countries and a customer base that includes some of the biggest names in manufacturing.

Its latest set of results showed why this consistency matters. For the six months ending September 2024, revenue came in at £123.4m, down slightly by 1.52% compared to the prior period. Despite this, Renold has maintained profitability, with net income of £14.5m over the trailing twelve months and an operating margin of 11.6%—up from 9.27% in 2023.

Crucially, Renold continues to generate strong free cash flow, with free cash flow per share at 10.6p in the last twelve months, up from 4.00p the year before. This has supported further balance sheet improvements, with net debt now at £62m, reflecting increased investment in the business. Despite the rise in debt, Renold’s net debt to EBITDA remains at 1.9x, which is still a comfortable level given the company’s earnings profile.

The company’s ability to defend margins in an inflationary environment speaks to the strength of its business model. With operating cash flow per share reaching 15.2p, Renold has the flexibility to continue investing in growth opportunities while maintaining financial discipline.

Renold Sector Diversification

Momentum building: A breakout on the horizon

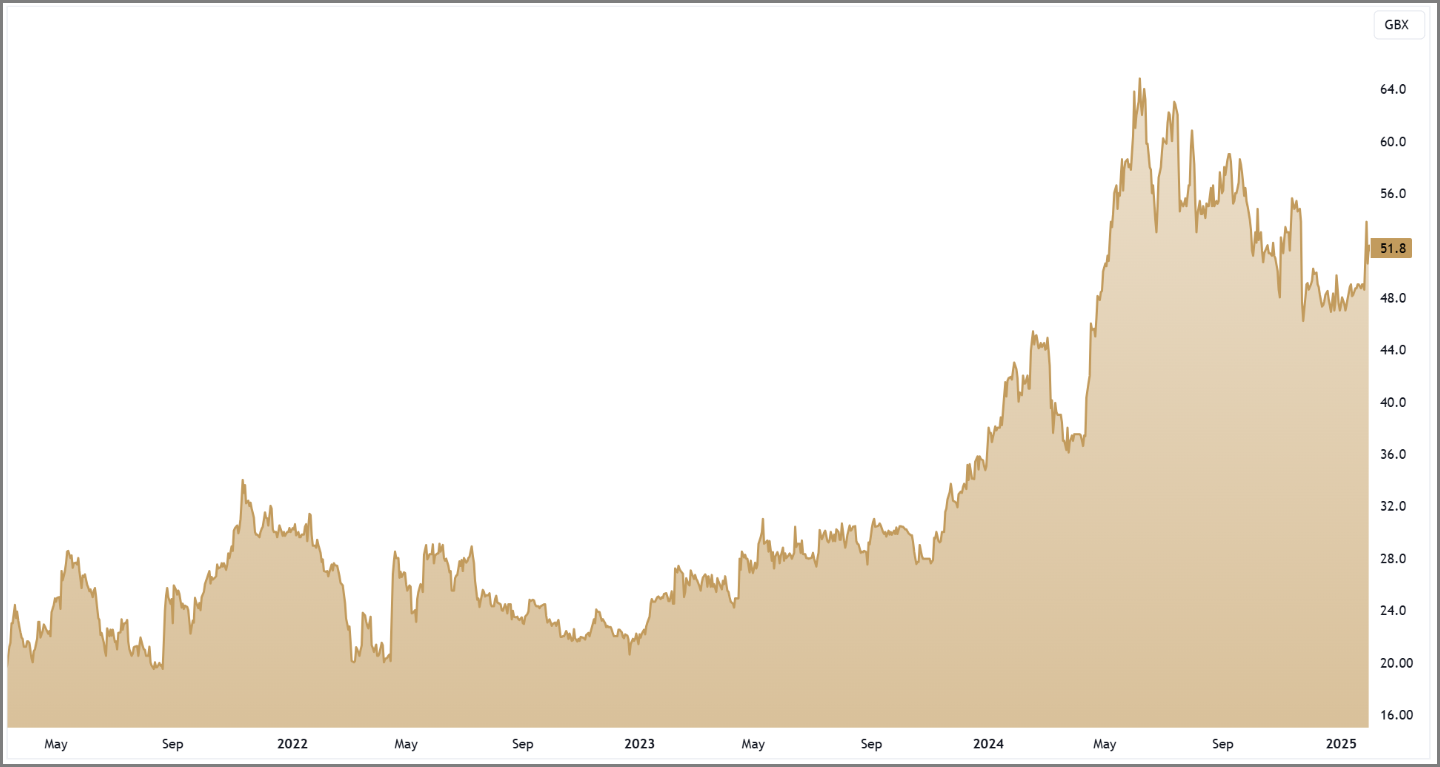

The technical picture has shifted in recent sessions. After spending months consolidating within a wedge formation, Renold’s share price has started to breakout higher on rising volume. This kind of price action often signals the start of a stronger uptrend, as buyers step in following a period of accumulation.

The shares are now trading above the 50-day moving average and prices are currently testing the 200-day moving average. This suggests that short-term momentum is aligning with the longer-term trend. In addition, the potential breakout has come on increased volume, reinforcing the idea that buying interest is picking up.

Historically, Renold shares have trended well once they get going. In 2023, the stock rallied more than 50% in six months after breaking out from a similar pattern. While past performance isn’t a guarantee of future results, the current setup looks constructive.

Valuation and upside

Renold’s valuation remains highly attractive, even after the recent rally. With a forward P/E of 6.2x, the stock is trading significantly below the sector average of around 12x for industrials. This low multiple presents a clear opportunity for re-rating, especially given Renold’s strong earnings growth trajectory and improving fundamentals.

The PEG ratio of 0.6 confirms that Renold is undervalued relative to its growth rate of 10.6% forecasted for the next year, significantly below the industry average. This suggests the market may be overlooking the company’s potential, providing us with an attractive entry point.

On an EV/EBITDA basis, Renold trades at 4.72x, a multiple well below the industry average of 7.5x. This indicates that Renold’s enterprise value is still not fully reflecting its operating performance and prospects. If the stock were to re-rate to a multiple closer to the sector median of 6x-7x, the stock could see a meaningful upside. A re-rating to 6x EV/EBITDA would imply a fair value closer to 65p, around 20% upside from current levels.

Renold’s Price to Free Cash Flow ratio of 5.5 is another compelling indicator of its undervaluation. The company has been delivering strong cash flow, with free cash flow per share at 10.6p for the last twelve months, up from 4.00p the year before. Given that Renold has been able to generate impressive cash flow while reducing debt, there is a strong case for a higher valuation multiple.

Why we’re adding

With operational momentum intact, improving margins, and a technical setup that favours further upside, we’re adding a second tranche to our position. The stock remains undervalued relative to its earnings potential, and the recent breakout suggests the next leg higher may now be underway.

Renold isn’t a high-flying tech stock or a speculative play—it’s a well-run industrial business with a clear growth path. And as history has shown, when these shares start moving, they can trend for extended periods. The trend is now in motion—so we’re staying on board.

RNO 3-Year Chart

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.